Risk managers adapt strategies to address shifting market dynamics

Persistent price hikes across major insurance lines prompt reevaluations Reprints

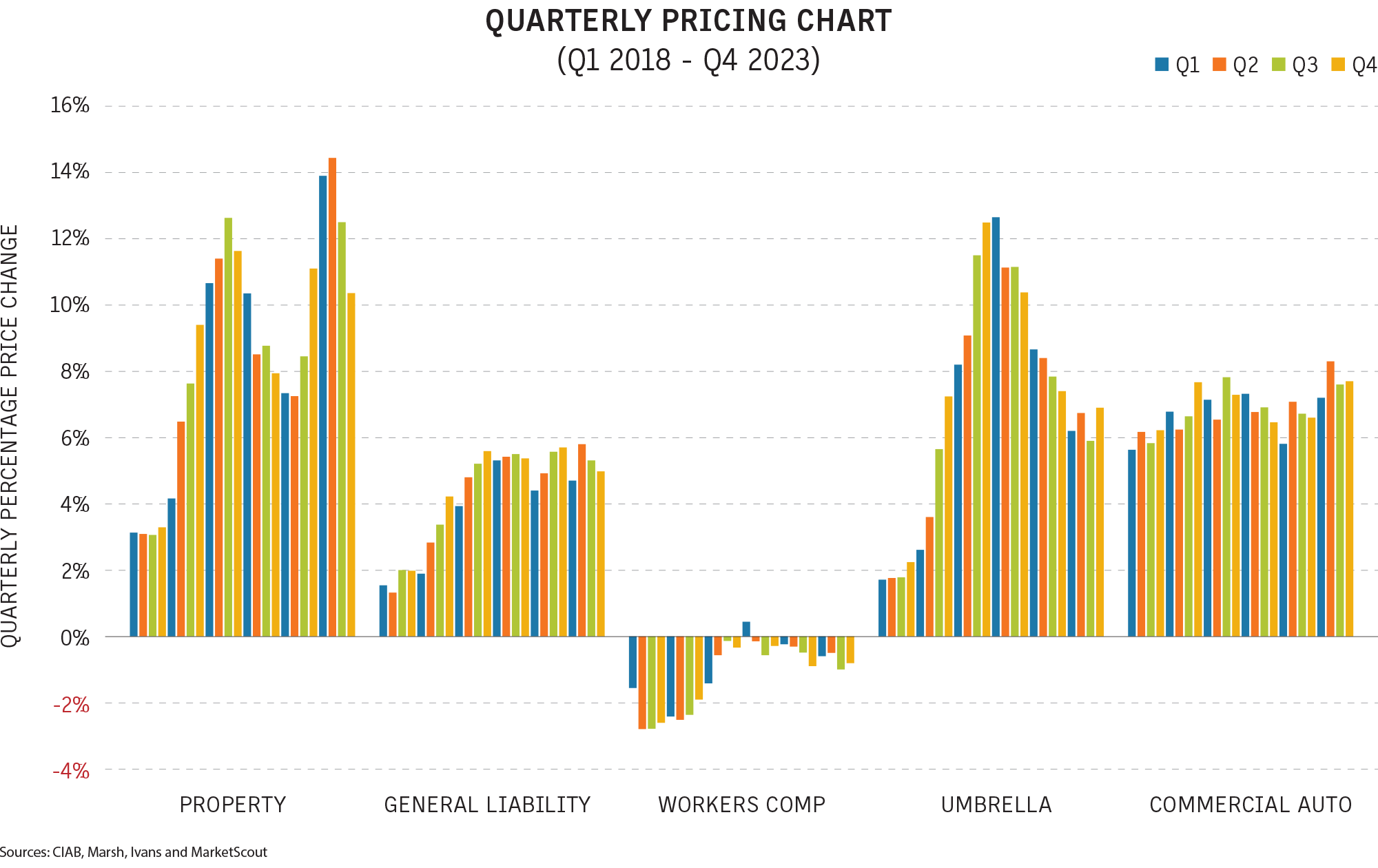

Commercial insurance buyers have endured price hikes in most major coverage lines for six years, and there seems little to suggest that rates will soften anytime soon.

According to Business Insurance’s quarterly pricing chart, which aggregates major industry quarterly pricing reports, prices have risen most for property insurance coverage, with rate hikes peaking at 14.4% in the second quarter of 2023. Umbrella rates saw the second largest average increase, peaking at 12.7% in the first quarter of 2021; followed by commercial auto, peaking at 8.3% in the second quarter of 2023; and general liability, which peaked at 5.8% in the same quarter. The interactive pricing chart is available at businessinsurance.com.

Some specialty lines, such as public company directors and officers liability insurance, have recently seen decreases, but overall the trend has been toward higher rates.

The only major line to show consistent decreases over the past six years was workers compensation, but the fall in rates was modest — the biggest decline was 2.8% in the 2018 second quarter — and employers still faced challenges with issues such as loss control and return-to-work strategies.

As buyers have adapted to the prolonged hard market, they have adopted new strategies and techniques to help their organizations remain comprehensively protected while minimizing cost increases. Business Insurance spoke with experienced risk managers and other insurance experts to learn more about the changes they have made to their programs and the successes they achieved.

Gavin Souter

Remarketing program produced cost savings, broadened cover options

Creating choices and opportunities has helped Vicinity Energy navigate the extended hard commercial insurance market, said Rachel Thuerk, the company’s Boston-based director of risk management.

Creating choices and opportunities has helped Vicinity Energy navigate the extended hard commercial insurance market, said Rachel Thuerk, the company’s Boston-based director of risk management.

The first thing Ms. Thuerk did when she joined Vicinity four years ago was to market the program, which brought in more insurers and choices for Vicinity, resulting in lower premiums.

“That took the price down almost immediately within one renewal cycle,” Ms. Thuerk said. “We went from being considered ahead of the market to being consistently at or below the market for renewal rates.”

The process was “tremendously time-consuming,” according to Ms. Thuerk, but it paid off. “Between changing brokers and marketing the program, we wound up saving about 20% in between the 2020 program and the 2021 program,” she said.

Energy can be “a particularly challenging” sector for insurance, and the hard market cycle began in 2017, running a “very long” seven years, Ms. Thuerk said.

The program’s property retentions have remained unchanged, and its liability retentions have seen “modest to moderate” increases depending on specific line of coverage, she said.

Ms. Thuerk also looked to risk control engineering and plant surveys, taking an eyes-on approach by attending five to seven engineering audits each year at Vicinity’s power generation plants.

“I go to every one, and I climb on every boiler, and that gives me so much insight into what’s going on with the plants, what really needs to be highlighted,” said Ms. Thuerk, who has a degree in mechanical engineering.

“Positioning ourselves aggressively as caring about constant improvement on risk reduction has been tremendous in terms of getting more markets engaged and limiting the premium spikes that some others are seeing,” Ms. Thuerk said.

The company, meanwhile, is taking strategic steps to change its exposure profile by reducing its use of fossil fuels.

“Vicinity is transitioning away from fossil fuels, which makes us a more attractive risk because the energy underwriters are under a lot of pressure to reduce their exposure, particularly to coal,” Ms. Thuerk said.

Matthew Lerner

Data-based approach made underwriters comfortable with risks

Early preparation and taking a data-driven approach enabled Kilroy Realty Corp. to successfully manage the hard market at its March 1 property renewal.

Early preparation and taking a data-driven approach enabled Kilroy Realty Corp. to successfully manage the hard market at its March 1 property renewal.

“It takes some intense strategizing to put yourself in the best position to come out with a renewal that you can say you’re happy with,” said Scott Ritto, senior vice president of risk management at Kilroy in Los Angeles.

As a predominantly West Coast-focused real estate investment trust, Kilroy is heavily exposed to earthquake risk, said Mr. Ritto, who is also president of the Los Angeles chapter of the Risk & Insurance Management Society Inc.

Kilroy worked with Marsh LLC to analyze its assets and improve its data quality ahead of its property renewal, checking to make sure secondary building characteristics, such as construction type, were correct, he said.

When the updated data was run through models, it showed a 42% decrease on the average annual losses for those properties, demonstrating on a scientific basis that its buildings would fare better in a large earthquake, Mr. Ritto said.

One of the benefits of data analytics is that insurers can feel more comfortable with the capacity or the pricing they offer, “because we should not have as many losses that would impact them,” he said.

The data also indicated Kilroy could reevaluate how much earthquake coverage it needed and buy less limit, he said.

“If you’re able to look at that (data) and say, ‘OK, maybe we don’t need as much limit as we bought before,’ that has a big impact,” Mr. Ritto said. Another benefit is that “it could bring other carriers into the mix,” generating more competition, he said.

Alternatives such as captives and parametric programs have gained popularity in the hard market, and risk professionals should consider them, but parametrics, which are based on triggers such as quake intensity rather than actual losses, can be problematic for a REIT, Mr. Ritto said.

“If we get a windfall, or capital, and we don’t have damages that income becomes an issue for us to manage and could potentially challenge a REIT status,” he said.

Claire Wilkinson

Price increases put risk mitigation efforts under the spotlight

Strong risk management practices and collaboration skills are helping risk professionals successfully navigate the hard market, said Patrick Sterling, vice president of legendary people at Texas Roadhouse in Louisville, Kentucky.

Strong risk management practices and collaboration skills are helping risk professionals successfully navigate the hard market, said Patrick Sterling, vice president of legendary people at Texas Roadhouse in Louisville, Kentucky.

“We always think about what we can do in advance so we don’t need to tap into our insurance,” said Mr. Sterling, who served as 2022 president of the Risk & Insurance Management Society Inc.

Restaurant businesses are susceptible to supply chain disruptions, inflation, increased litigation, cyber threats, safety issues and staff retention challenges.

“The hard market really emphasizes the impact of all these risks and our ability to recover financially,” he said.

Scenario planning, where companies run tabletop exercises to test their business continuity in response to a particular threat such as a ransomware attack, is playing a growing role in mitigating risk, Mr. Sterling said.

It’s critical that risk professionals take a “hard look” at their portfolio risk and ensure they have the correct asset values, he said.

Taking the time to understand their insurance policies is also important, Mr. Sterling said.

“A lot of times terms may have changed. There may be new verbiage in there. You’ve got to make sure you work closely with your broker partners and that you’re paying attention to all those details,” he said.

Restaurant risk managers are using insurance more creatively, Mr. Sterling said. Some are opting to self-insure rather than purchase coverage at a higher cost, depending on the organization’s risk profile and tolerance.

“At that point, having a conservative balance sheet is really important so you have enough money in the bank when the crisis strikes,” Mr. Sterling said.

Alternative risk financing, such as single parent or group captives and risk pools, increasingly are being considered. “Everybody wants to get information on how to get a captive started and how they can add value,” he said.

But some companies may still choose to purchase insurance even if it costs more, based on their risk appetite, Mr. Sterling said. “That’s always an option, but that’s where your long-term carrier relationships are really important,” he said.

The best way to navigate the hard market is to build strong risk management practices and partner with business leaders across the organization, Mr. Sterling said.

“Risk managers that are effective, realize that this is a team sport,” he said.

Claire Wilkinson

Alternative vehicles tapped to ease burden of higher retentions

The challenging insurance market for buyers has created change, said Chris Lang, New York-based global placement leader, U.S. and Canada, for Marsh LLC.

The challenging insurance market for buyers has created change, said Chris Lang, New York-based global placement leader, U.S. and Canada, for Marsh LLC.

More risk retention by clients is a direct consequence of the extended firm market, and it takes many forms. At a basic level, policyholders are taking higher deductibles and higher retentions, but they are also using captives or alternative structures, such as multiyear structured insurance programs or integrated programs that blend different coverages to achieve savings, Mr. Lang said.

Parametric coverage, which is insurance triggered by a specific data point, such as wind speed or rainfall amount, is another tool gaining traction in the hard market.

“We’re having a parametric conversation in every renewal strategy meeting. We’ll have that conversation with just about every significant client,” Mr. Lang said.

The use of parametric coverage, although still limited compared with traditional indemnity insurance, has increased “exponentially” among clients in the hard market, he said. One typical use is to fill in wind and other types of deductibles that have risen.

Submissions have also changed, with brokers and policyholders ensuring they are ready to answer increasingly granular questions from insurers about particular risks, Mr. Lang said. “Underwriters are asking specific questions to address certain exposures, so your submissions are more robust,” he said.

There are more data and technology tools available to help answer those questions and provide information, although they add time to the process, he said.

“It takes longer to get to that well-informed decision before you bind coverage,” Mr. Lang said.

“On the larger, more sophisticated end, the biggest accounts, it’s almost time to begin the renewal process right after you renew to get the longest running start. You almost never put the file down,” he said.

While submissions have been refined to carry more information and answer more potential questions, insurers “have gotten better at communicating the need for rate, the need for rate adequacy and for a capital return,” Mr. Lang said, helping to smooth negotiations in a challenging market.

Matthew Lerner

Early reporting helps curb university’s workers comp claims

While workers compensation hasn’t seen volatile conditions that other insurance lines have experienced over the past six years, risk managers remain concerned about trends such as an aging workforce, rising treatment costs and overall employee health.

While workers compensation hasn’t seen volatile conditions that other insurance lines have experienced over the past six years, risk managers remain concerned about trends such as an aging workforce, rising treatment costs and overall employee health.

Courtney Davis Curtis, Chicago-based assistant vice president, risk management and resilience, planning for the University of Chicago, likens the school’s campus to a small city, employing about 25,000 workers in such areas as administration, health care, public safety, faculty, research, printing press operations, student work-study and maintenance.

Workers comp claims come from common sources such as slips, trips and falls and strains that come with heavy lifting but also from less common sources such as accidental needle pricks among workers in the university’s research hospital. The school also has to address the risk of infectious disease, which is more pronounced since the COVID-19 pandemic.

An effective way to control costs overall has been the university’s early reporting model, a strategy that grew out of studying claims activity and outcomes, Ms. Davis Curtis said.

“It’s the information that we’ve gleaned from many, many years of historical data to manage and monitor the different (injury and treatment) trends that we see,” she said.

“As soon as an employee is injured, we like to be notified of that immediately, get the necessary paperwork completed and put our insurer on notice. That’s helpful from a couple of regards. It’s ensuring that your employee gets the treatment and the care that they need, and if an investigation is needed we’ll be able to get on top of that.”

Return to work strategies can be a challenge, Ms. Davis Curtis said, as narrow job classifications and department budget constraints make offering light duty difficult.

Such programs “can be pretty challenging to implement at any of the higher education environments,” she said. “Many institutions are relatively decentralized … from a budget or financial perspective.”

To prevent claims, the risk management department regularly meets with other departments, such as human resources, to implement safety and employee wellness strategies, she said.

“We’re pretty holistic in our approach and as comprehensive as necessary to come together as partners to find and identify solutions,” she said.

Louise Esola

Cybersecurity vital as hackers target gaming sector

Doubling down on cybersecurity, evaluating multiyear programs and selling their risk to insurers are some of the strategies that can help casino risk professionals manage rising insurance costs.

Doubling down on cybersecurity, evaluating multiyear programs and selling their risk to insurers are some of the strategies that can help casino risk professionals manage rising insurance costs.

Cyberattacks are a top concern for the entertainment sector and organizations are focused on eliminating or reducing cyber risks, said Mark Habersack, executive director of risk management at Resorts World Las Vegas.

Ransomware attacks at MGM Resorts International and Caesars Entertainment Inc. last year highlighted the threat to the casino industry which collects substantial data through its player programs, vendors, contractors, employees and guests, he said.

“Security is the No. 1 priority because of what a cyberattack costs companies and the reputational risks that go along with it,” Mr. Habersack said.

Opened in 2021, Resorts World’s modern technology, employee training, multifactor authentication and multifaceted software systems have helped its cyber insurance program, he said.

Affecting various lines of coverage, Nevada Assembly Bill 398, signed into law last year, requires insurers to offer coverage for defense costs outside the limits of liability policies. Resorts World used multiyear policies to manage the change, Mr. Habersack said.

“We went back on certain lines of coverage, we canceled coverages, and we wrote coverages for a two-year program, starting Oct. 1, hoping that our legislature when it comes back in two years, will come to their senses,” he said.

Resorts World also renewed its property program for a two-year term. “That actually saved us a little bit more money,” Mr. Habersack said. “Obviously, the flip side is if the market goes completely the other way, becomes a very soft market, you could end up paying more.”

Higher deductibles are another option, but “it’s important to determine what your risk comfort level is,” Mr. Habersack said. Resorts World has a $250,000 deductible on its liability insurance program and $500,000 on property and considered increasing them many times in the past three years, he said.

“The problem when you go up, it’s extremely difficult to go back down, so you’ve got to be careful if you’re going to raise it, and then when you raise it, how much savings does that really equate to?” he said.

The best way to control costs is to “sell yourself,” Mr. Habersack said. “We bring the carriers out, do tours, get them to understand why we’re a much better risk than any other property on the Strip,” he said.

Claire Wilkinson

Captives strengthen ties with insurers, differentiate risks

The hard market has prompted risk managers to explore alternative risk transfer solutions, such as using captive insurers and data analysis to deaden the blow of skyrocketing premiums, said Kevin Bates, group head of risk and insurance for Australian construction company Lendlease Corp. in Sydney, and a Risk & Insurance Management Society Inc. board director.

The hard market has prompted risk managers to explore alternative risk transfer solutions, such as using captive insurers and data analysis to deaden the blow of skyrocketing premiums, said Kevin Bates, group head of risk and insurance for Australian construction company Lendlease Corp. in Sydney, and a Risk & Insurance Management Society Inc. board director.

“We get better at enhancing our risk management practices when the market is hard,” he said.

Deploying captives demonstrates a company’s knowledge of its own risks and shows insurers a willingness to “put some skin in the game,” Mr. Bates said.

“You want to differentiate your risk and want to show that you know your risk, so you actually get better at knowing and understanding your data set and what it means,” he said.

Using a captive as a primary layer of coverage can forge a stronger relationship with an insurer and can also be useful for providing certain levels of excess coverage, he said.

“I deploy my captive generously throughout my program in risks that I’m prepared to demonstrate and evidence to the insurance market that they can trust because I trust them, and it’s my own money,” Mr. Bates said.

In addition, captives can be used strategically throughout a coverage tower, he said.

“If you’ve got a particular layer that is so expensive compared to what’s below it, and what’s above it, you can deploy your captive there. So, it’s ventilated capacity that you can do a more affordable rate,” he said.

Seeking guidance from and maintaining good rapport with an insurance broker are also crucial during a hard market, Mr. Bates said.

“Relationships with brokers and insurers are very important. Don’t underestimate the broker’s role, as they are really key to differentiating the risk and they have a lot of relationships with the insurers, so they can take a big portfolio and focus on loss prevention and loss control,” he said.

Obtaining multiyear policies is also a viable option if the rate is good, Mr. Bates said.

Shane Dilworth

Accurate valuations create more stability over the long term

Risk managers should “keep their foot on the gas” when it comes to valuing their risk, continue to gather data on their facilities, and find long-term solutions to deal with premium rates that have skyrocketed, say brokers at USI Insurance Services LLC.

Risk managers should “keep their foot on the gas” when it comes to valuing their risk, continue to gather data on their facilities, and find long-term solutions to deal with premium rates that have skyrocketed, say brokers at USI Insurance Services LLC.

Insurers and brokers have emphasized for the past several years that property values should be updated to take into account replacement cost inflation.

“We’re a lot closer than we ever have been to adequate valuations,” said Jeff Buyze, Orlando, Florida-based national property practice leader at USI. “Although it’s still topical, I don’t see that as being the large gap that it was when we started the hard market.”

Supply chain pressures and inflation have eased, Mr. Buyze said.

If policyholders continue to update valuations regularly and gather location data, they will improve their risk profiles, he said.

“If you’re consistent with how you value your assets and your personal property while continuing to gather key underwriting data points, the hard market will become less of an issue going forward,” Mr. Buyze said.

Policyholders should also retain more risks, be flexible about the use of instruments such as indemnity agreements, obtain fronted reinsurance capacity and deploy the surplus in their captives to continue adapting to the hard market, he said.

While captives may not be a suitable option for every business, “they’re a very viable long-term solution to reduce the volatility in the market,” Mr. Buyze said.

Group captives can secure long-term rate stability for commercial policyholders and some provide excess capacity with fixed rates, said Douglas O’Brien, New York-based national practice division manager, casualty and alternative risk, at USI.

Group captives can secure long-term rate stability for commercial policyholders and some provide excess capacity with fixed rates, said Douglas O’Brien, New York-based national practice division manager, casualty and alternative risk, at USI.

Mr. O’Brien said the rating methodology hasn’t changed really more than half a point since 2018. So, we’ve put a lot of clients into a group captive solution, because of that inherent long-term rate stability.”

Policyholders should also consider a multi-year program that offers a fixed rate for a specified period, he said.

In addition, bundling various coverage lines with the same insurers is a “one-stop shopping approach” that achieves “economies of scale” through discounts, Mr. O’Brien said.

“When you bundle primary casualty and umbrella excess casualty, you get an inherent discount. When you add in things like property, or maybe some executive protection lines, you’re getting even more of a discount,” he said.

Both brokers also stressed the importance of risk managers regularly meeting with underwriters to differentiate their risks compared with their peers.

Shane Dilworth