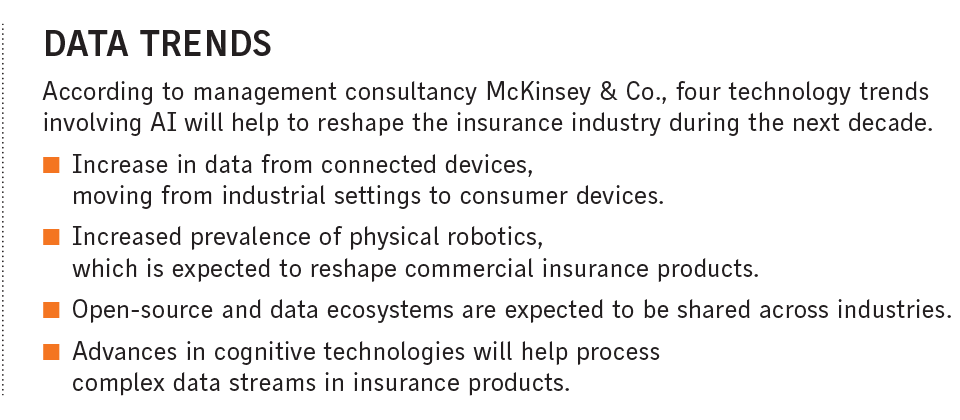

AI technology builds momentum in claims sector

Reprints

The insurance claims sector is tapping into technologies such as machine learning and artificial intelligence to increase efficiency, improve outcomes and detect fraud.

Whether it is a simpler version of AI that can be used to automate back-office processes or the newer generation AI, which can be used to analyze policyholders’ claims history and policy preferences, these new technologies are becoming more widely used in the industry.

“There are a lot of policies that are written and a lot of claims that occur, which all have data around them,” said Stan Smith, founder and CEO of Boston-based Gradient AI, which provides AI services for the insurance industry. “As I looked into it, claims were more of a challenge than underwriting. There was a lot of focus on how to get our claims costs under control.”

Yet “the vast majority of claims being pretty benign means a lot of people have busy work to do,” he said, adding that technology can help mitigate workloads.

Gia Sawko, Gradient’s senior product manager of claims, said AI will change the way jobs are performed.

“There are jobs out there that are duplicative, or the resources could be divided differently so you’re spending more time on the complex claims,” Ms. Sawko said. “There are things that could be done that could be automated with the use of AI.”

While the term AI is used broadly, it encompasses various platforms and processes. Automation and AI, for example, are sometimes used interchangeably, but they differ, said Leah Cooper, Chattanooga, Tennessee-based managing director of IT for Sedgwick Claims Management Services Inc.

“AI is just the tool,” Ms. Cooper said. “Automation is putting all of the pieces together.”

When rolling out AI pilot programs, Sedgwick saw success in document digitization and validation, reading for content, and automatic eligibility confirmation used to validate whether someone has proper coverage.

“AI is not going to replace someone’s job. What it’s going to do is take the red tape and the busy work off someone’s desk so that you change the story about that person’s job,” Ms. Cooper said.

She said AI is also being used to detect claims oddities and discrepancies that could potentially signal insurance fraud (see related story below).

“There are a lot of different opportunities when it comes to plugging into tools that can spot abnormalities,” she said. “Using AI, we’re able to spot the outliers, what’s not normal.”

The insurance industry traditionally lagged in technology, said Cheryle Tuttle, Tampa, Florida-based vice president of property/casualty and workers compensation for Sapiens International Corp.

“A lot of the problems have not changed,” Ms. Tuttle said. “It’s just technology and things like AI, data analytics, automation, these are all helping people in being proactive instead of reactive.”

New technologies such as AI have “tremendous promise for our industry but if misused could be certainly damaging and counterproductive,” said Joe Powell, Fort Wayne, Indiana-based senior vice president for data and analytics with Gallagher Bassett Services Inc.

Mr. Powell drew distinctions between the different forms of AI, including “narrow” AI, or machine learning, where models are built or “trained” on data targeting a specific desired decision outcome, and generative AI, which can involve taking a “single, very general model and (applying) it to a whole host of use cases.”

“Those two are not substitutes for each other,” he said. “It’s not like we’ve moved from one to the other. I think the new, generative AI models are going to complement our narrow AI models in a lot of ways,” Mr. Powell said.

Generative AI has the potential to improve the claims process because it enables claims professionals to “deliver a consistent product in an efficient way,” he said.

Mike Cwynar, Orange County, California-based senior vice president of product delivery for Mitchell Casualty Solutions Group, said AI can benefit back-office claims management as well as customer service and document digitization tasks.

“A lot (of our clients) are really putting thought into how to make it a really user-friendly claims experience,” he said.

Insurance personnel considering using generative AI should start small. “I wouldn’t go in and try to rewrite your back-office process here,” Mr. Cwynar said.

“It’s key to partner with folks who understand not just the technology but the business domain, the problem that you’re trying to solve, and being really careful in what you end up going after,” he said.

Generative AI, he said, can generate content such as photos, video, text and code, and attempts to read questions and provide answers. But it can also suffer from what’s known as “hallucination,” a term referring to times when AI provides an answer not in line with what is expected.

“You really need to understand what you’re trying to get out of tools like this, because they’re tools right now,” Mr. Cwynar said. “I wouldn’t throw generative AI at the most complicated problem that I have out there. I’d use it to automate tasks and build my expertise and sophistication with it over time.”

Machine learning powers fraud detection

As artificial intelligence becomes more widely used in the insurance industry, one function that can benefit from its implementation is fraud detection.

Generative AI can look at various factors in claims filings to see if there are any indicators of fraud, such as “falsification of details around the damage level,” said Leah Cooper, Chattanooga, Tennessee-based IT managing director for Sedgwick Claims Management Services Inc.

AI can be used to detect atypical behavior, a sign of potential fraud, said Joe Powell, Fort Wayne, Indiana-based senior vice president for data and analytics with Gallagher Bassett Services Inc.

“What’s great about these AI systems is that they can learn what’s typical across a much broader spectrum of data than a human can ever look,” Mr. Powell said.

AI, especially Microsoft OpenAI’s language model GPT, can be particularly useful in fighting fraud, since it can “analyze vast amounts of claims or communication data, spotting patterns and inconsistencies that may suggest fraudulent activity,” said Gregg Barrett, CEO of Kalispell, Montana-based insurance software provider WaterStreet Co.

QBE North America partnered with Vejle, Denmark-based DETECTsystem A/S after learning about that company’s fraud detection system, FDS, which uses advanced technology to detect image and document fraud in claims, said Brian Wilson, vice president and head of the special investigations unit at the New York-based insurer.

“You receive a lot of these (supplemental documents) with every single claim that comes in,” said Dan Gumpright, Scottsdale, Arizona-based executive vice president of products and operations for DETECTsystem A/S. “It’s kind of like looking for a needle in a haystack.”

Putting a human on fraud detection would be “very inefficient in terms of cost,” whereas AI can complete the task quicker and more accurately, he said.