Insurers back away from police liability

Reprints

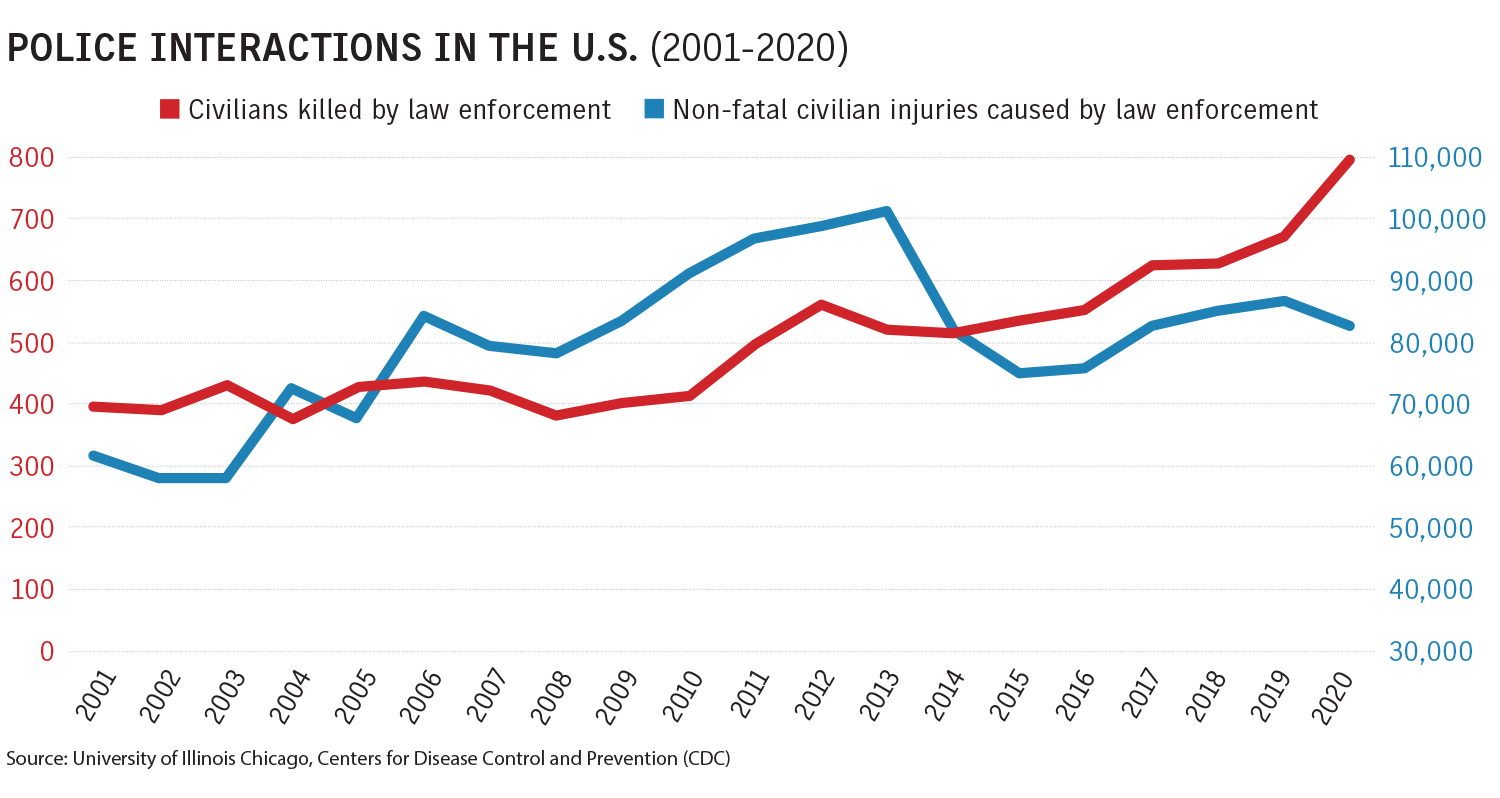

Three years after the murder of George Floyd by a Minneapolis police officer, law enforcement departments across the United States continue to struggle with the risk management repercussions of Mr. Floyd’s killing and similar incidents.

In addition to Mr. Floyd’s death by asphyxiation during an arrest in 2020, other high-profile incidents include Breonna Taylor’s shooting death by police in Louisville, Kentucky, the same year and Tyre Nichols being beaten by police officers in Memphis, Tennessee, in January. Mr. Nichols died three days later.

The deaths have had a significant impact on the law enforcement liability insurance market as underwriters factor into their considerations litigation arising from such incidents, a wary and sometimes hostile public, rising court awards and a shortage of qualified police candidates.

Observers say insurers are generally seeking price hikes ranging from single-digit percentages to 20%, depending on the risk. While some say the market is more stable compared with a couple of years ago, it remains relatively hard and is not expected to soften soon.

The risk is either covered on a standalone basis or as part of public entity coverage, which is often written by pools. While a greater number of law enforcement entities obtain their coverage as part of a general public entity package bought by a municipality, larger police departments are more likely to buy their own insurance.

Major issues facing police departments include dealing with disturbed individuals and recruitment (see related stories here and here).

The number of insurers writing law enforcement liability insurance has declined from about 30 several years ago to about 10, and limits have also contracted.

“You really have to build a lot of limits” to create a coverage tower, said Lindsay Cunningham, Seattle-based North American public sector and education industry division leader for Willis Towers Watson PLC.

Insurers rarely offer more than $5 million in limits in any one layer, exclusions are broadening, and rates are increasing, brokers say.

CLICK IMAGE TO ENLARGE

“We’re still very careful about putting out too much capacity in the wrong jurisdiction, where public sentiments are still somewhat negative for law enforcement,” said Mark Dillard, president of Richardson-based Public Risk Underwriters of Texas.

Many underwriters “won’t look at the class,” said Alan Mooney, CEO of Hamilton-based Amwins Bermuda Ltd., a unit of Amwins Group Inc. There are insurers that have decided to stop writing that particular line or are continuing to do so with sublimits and applying aggregate limits, he said.

But there are geographical variations, said Daniel Howell, managing director of Alliant Public Entity, a unit of Alliant Insurance Services Inc., in Seattle.

“It ranges from firm in most parts of the country to very firm, bordering on hardening, in certain jurisdictions,” including major metropolitan areas where there are no tort caps.

The market has stabilized since 2020 and 2021, when there was much debate over the issue of police, including calls to defund police departments “but it stabilized on the high side,” said Anthony DiBernardino, national public entity and education practice leader for USI Insurance Services LLC in Philadelphia.

“The claims are the same,” he said. “What’s changed is, claims are on the rise, and clients that have never before seen claims” are now encountering them, while higher court awards are driving up settlements.

Insurers are concerned about the unpredictable nature of police-related risks, said Jose Peralta, Washington-based managing director, U.S. public sector, and national practice leader, commercial risk, at Aon PLC.

“There’s a perception of volatility, and that’s causing much of the consternation we’re seeing from the carriers,” he said.

Insurers are “looking for a lot of information about policies and procedures and adherence to best practices,” Mr. Peralta said. In addition, they are concerned about incidents being picked up by social media, leading to large settlements, he said.

When insurers provide the coverage, it is often with very large deductibles and low limits, said Edward Cooney, partner and senior account executive with broker Conner, Strong and Buckelew in Parsippany, New Jersey, who works with New Jersey’s Municipal Excess Liability Joint Insurance Fund. The Parsippany-based fund insures about 550 municipalities, about 90% of which have law enforcement exposure.

He said the fund has not had problems obtaining coverage because of its loss history.

Underwriters are approaching risk “with increased scrutiny and a much more thorough evaluation of the law enforcement agency’s risk profile,” said Terry McCann, president of RT Specialty Chicago, a unit of Ryan Specialty Holdings Inc.

“The insurance companies that have not withdrawn are tightening up the offerings that they’ve made or broadening (their coverage) and charging an appropriate premium” when they extend coverage to include civil rights violations or wrongful use of force, he said.

“They’re going to look at factors such as training protocols, internal policies, complaint history and community relations,” Mr. McCann said.

Many experts point to public perception as a factor driving the increased claims.

After the outcry following the murder of Mr. Floyd, prospective jurors are more likely to question law enforcement operations, which changes the profile of liability risks, said Jeb Brown, senior counsel with Liebert Cassidy Whitmore in Los Angeles, who represents public entities.

People “are inclined to give the benefit of the doubt” to the accused rather than the police officer, for whom “it’s an uphill battle to defend,” Mr. Dillard said.

“Often, it’s easier to just pay a small, monetary settlement as a frivolous payment” rather than to defend a lawsuit, said Tom Kulhawik, Stamford, Connecticut-based Northeast regional program manager for the Commission on Accreditation for Law Enforcement Agencies, who retired as police chief of Norwalk, Connecticut, in January.

Sandra McFarland, New York-based senior vice president in Marsh LLC’s U.S. public entity casualty placement practice, said, “We’re definitely seeing more stabilization this year than we have in prior years, but we haven’t really seen additional capacity, or carriers putting up additional limits, so the outlook is for continued rate increases.”