Cat bond structures build cyber capacity

Reprints

The market for insurance-linked securities supporting cyber exposures reached a critical mass in the first quarter, and market participants are optimistic that more deals will be announced this year.

Demand for coverage and reinsurance capacity dovetailed with advances in modeling to facilitate transactions sponsored by London-based Beazley PLC and German reinsurer Hannover Re SE in January, with support from brokers, cyber insurtechs and key investors.

In some ways, the emergence of capital market support for cyber exposures parallels the early days and development of the catastrophe bond market for hurricane and earthquake risks, which also initially featured smaller deals and was a response to market demand for coverage expansion, sources said.

The ILS market has expanded to include a variety of structures, such as sidecars and collateralized reinsurance vehicles, and has become a significant part of the overall reinsurance market, particularly the retrocessional market.

“When you go back to why the catastrophe bond market was created some 25 years ago, it was because demand for the product was outstripping supply from conventional sponsors,” said Paul Schultz, Chicago-based CEO of Aon Securities, a unit of Aon PLC.

Cyber insurance markets are beginning to face a similar quandary.

“The direct market now for insurance companies is very expensive and very limited,” said Jeff Mohrenweiser, Chicago-based senior director of global securities for Fitch Ratings Inc.

Cyber reinsurance markets are “materially underserved” by traditional reinsurers, and capital markets are essential to allow the business to grow, said Theo Norris, London-based cyber account executive, insurance-linked securities, at Gallagher Re, the reinsurance brokerage arm of Arthur J. Gallagher & Co.

Paul Bantick, head of global cyber & technology at Beazley, said the cyber insurance market is generally thought to be roughly $10 billion in premium. “If we’re going to go from $10 billion to $30 billion or $40 billion and manage the systemic exposure as we do that, we need to create a catastrophe market for cyber.”

The Beazley and Hannover Re deals broke the ice.

Beazley’s $45 million private Section 4(2) cyber cat bond is designed to cover remote probability catastrophic and systemic events and gives Beazley indemnity against all perils in excess of a $300 million catastrophe event, with the potential for additional tranches to be released through 2023 and beyond.

The Beazley cyber bond is backed by investors including Fermat Capital Management LLC, and was structured and placed by Gallagher Securities, the ILS business of Gallagher Re.

The Hannover Re deal involved Stone Point Capital investing $100 million in what was termed “a proportional reinsurance solution” for retrocessional coverage. The deal “covers cyber risks in Hannover Re’s worldwide portfolio and has a long-term orientation,” according to a Hannover Re statement announcing the deal.

Mr. Bantick said the Beazley bond used both internal and external models (see related story) and the specialty insurer spent months informing and courting investors prior to the deal.

Since going public, investor interest in the deal has multiplied, Mr. Bantick said. Some investors that were not ready to invest in January likely will invest in similar deals later this year, perhaps in the second and third quarters, he said.

Capital market support for cyber exposure is “likely to start in a measured way, no different than the catastrophe bond market,” Mr. Schultz said. “We’ll start slowly. We’ll start to bring investors into these transactions. Comfort and transparency will grow over time.”

“I think there are investors who are willing to be first movers,” Mr. Mohrenweiser said, noting that against the multibillion-dollar scale of the investment funds involved, the size of the new cyber bonds does not represent an existential risk. Both he and Mr. Schultz said 2023 will likely produce additional cyber capital markets deals, a view widely shared.

Gallagher Re’s Mr. Norris said the broker “is currently working closely with a range of cedents to bring more cyber ILS deals to markets — from bonds to sidecars.”

Oliver Brew, London-based cyber practice leader for Lockton Re, the reinsurance business of Lockton Cos. LLC, called the Beazley cyber bond “a forebearer of deals to come.”

One reason for the pivot to the capital markets for additional coverage is the exposure to accumulations of risk for insurers and reinsurers, said Sharon Haran, chief commercial officer in Tel Aviv, Israel, for Parametrix Insurance Services LLC. Parametrix provides index-based coverage for cloud service outages and regularly monitors that sector for such activity as part of its operations.

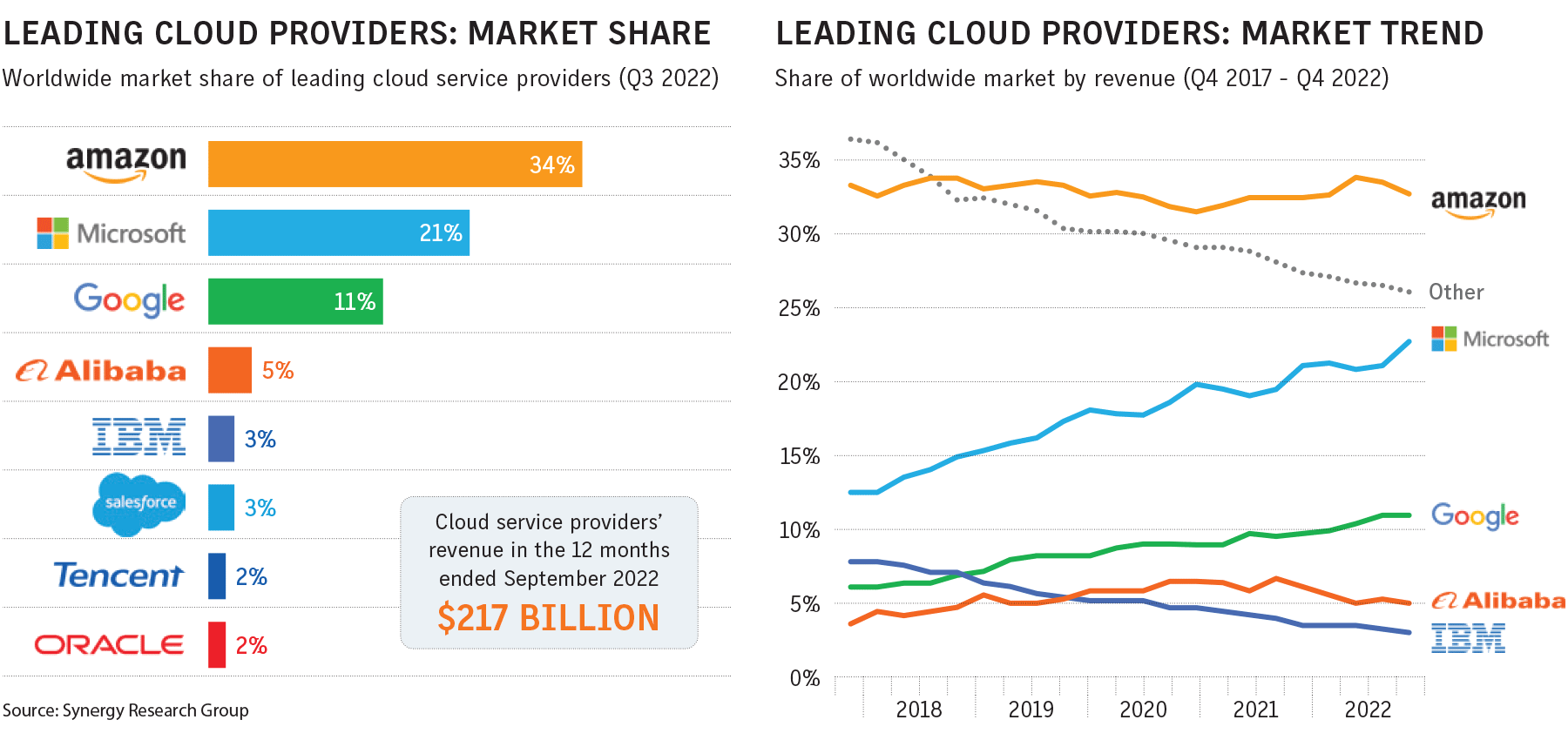

With cloud services market share concentrated largely among three top providers (see charts) and surveys showing that 60% to 70% of enterprises use cloud services, Mr. Haran said an insurer or reinsurer could have multitudes of unrelated clients compromised at once.

CLICK IMAGE TO ENLARGE

Location plays an integral role in evaluating such exposures because the cloud is not a monolithic entity but based in regions, so downtime at a given data center serving a specific region could lead to a contagion of exposure.