D&O rates fall but economy fuels unease

Reprints

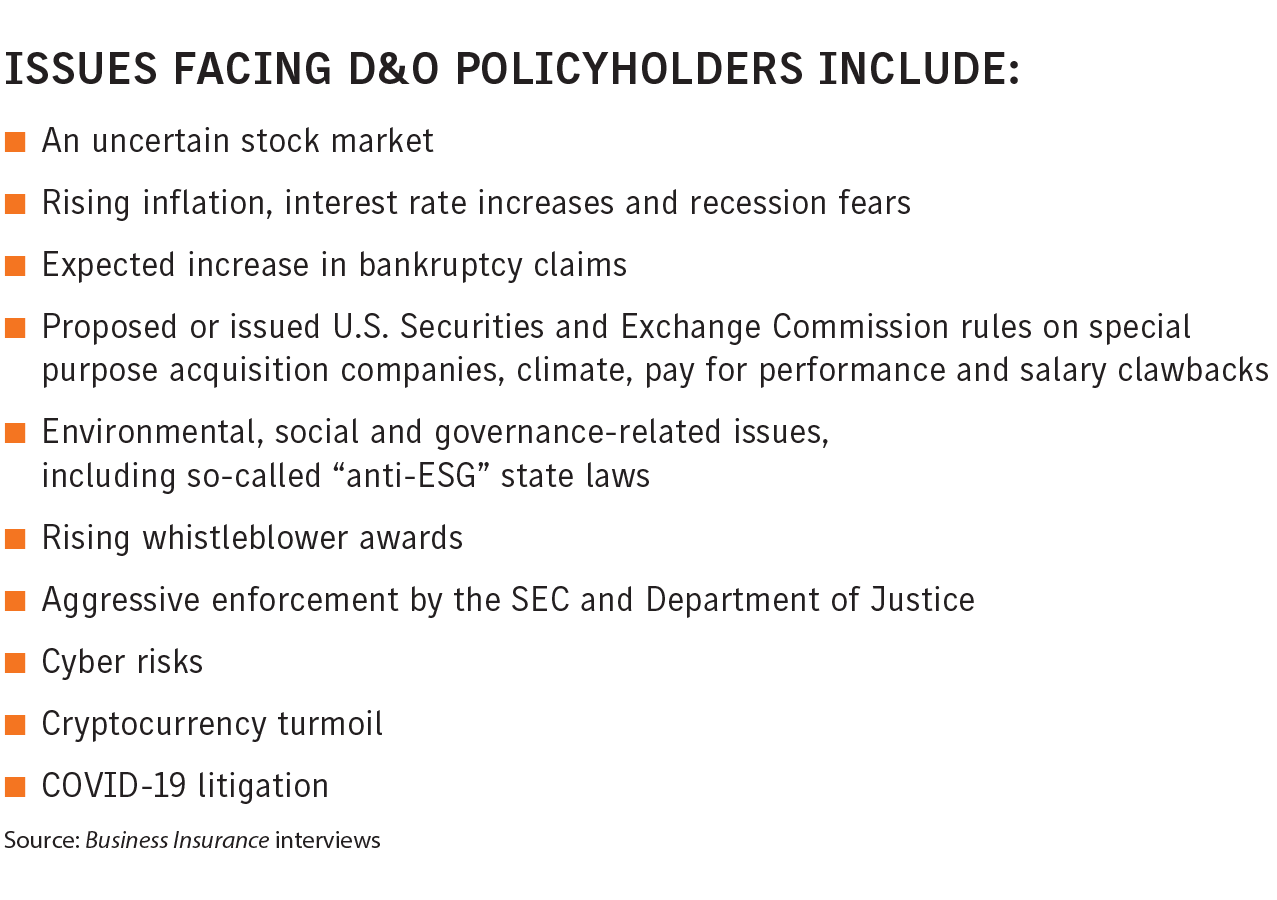

Directors and officers liability insurance policyholders are seeing their first soft market in years, but a host of issues are creating significant uncertainty.

These include the economic outlook, which has led to concern about increased bankruptcy-related claims; an aggressive U.S. Securities and Exchange Commission and Department of Justice; and cyber, cryptocurrency, COVID-19 and environmental, social and governance-related issues.

There is “a bit of a minefield ahead of us which we’re trying to navigate,” said Mike McGuinness, New York-based senior vice president-public management liability, for QBE North America.

Experts say with fewer initial public offerings and the special purpose acquisition company market’s collapse, more capacity has been freed up, which has prompted new and established insurers to compete more vigorously for the remaining business.

While D&O rates are decreasing it’s unknown how long that will continue, experts say.

The tipping point will be when the overabundance of capacity dries up and rates fall below breakeven, said Matthew Azzara, head of management liability for North America for Allianz Global Corporate & Specialty SE.

Beginning last year, D&O rates overall have decreased by several percentage points, with the declines particularly strong in excess layers, where new capacity is generally focused. Insurers are generally not increasing limits, experts say.

“I’ve been surprised by the rapidity with which rates have fallen,” and it remains to be seen how low the floor will be, said Priya Cherian Huskins, San Francisco-based partner and senior vice president at broker Woodruff Sawyer & Co.

“We’re still not back to where we were in the hard market, but the question for everyone is what happens in 2023,” said Kevin LaCroix, executive vice president in Beachwood, Ohio, for RT ProExec, a division of R-T Specialty LLC.

He said that while some have predicted the market will plateau at a lower level, he’s “a little more skeptical.”

Some insurers “are holding the line and slowing down the increases, but we still see an overall trend down for some time,” said Larry Fine, New York-based management liability coverage leader for Willis Towers Watson PLC.

Furthermore, the more than 30 new D&O markets that have recently entered the sector “haven’t started to drop out or consolidate yet,” while the increased premiums insurers had anticipated from SPACs and IPOs did not materialize, he said.

“We just have to make sure that these insurers are here to stay” and that they are financially stable, said Devin Berensheim, New York-based executive vice president, specialties practices, with Lockton Cos. LLC.

First-quarter renewals will be more telling as accounts that had reductions last year are renewed, said Patrick Whalen, a New York-based underwriter on Beazley PLC’s executive risk team.

“There’s a lot of talk in the marketplace about stability,” with insurers pointing out the inventory of claims from earlier calendar years that have not yet been settled, said Tim Fletcher, Los Angeles-based CEO of Aon PLC’s financial services group in the United States.

They are “talking about trying to hold the line,” and at least for the next few months “we’re expecting a similar pricing environment” to the current one, he said.

There is ample capacity and competition among established and newer insurers, Mr. LaCroix said.

Other factors could also change the market, said David Lewison, senior vice president and national professional lines practice leader for Amwins Group Inc. in New York. “There’s always some wild card thing that happens that changes the market a little bit.”

Frequently cited as a worry by D&O experts is the economic uncertainty, with higher interest rates and a jittery stock market. The S&P 500 was down 19.44% for 2022.

Litigation tends to increase when the stock market tightens, which could affect D&O, said Ernest Martin Jr., a partner with Haynes & Boone LLP.

The concern is “about whether we’re going to have a rough economic year in 2023,” said Andrew Doherty, New York-based national executive and professional risk solutions practice leader for USI Insurance Services LLC.

“I don’t think we’ve begun to see the full impact of the high inflationary environment on corporate earnings,” as companies anticipate the impact of federal policies, Mr. McGuinness said.

Earnings continue to be propped up by a strong labor market and stimulus money, but that money is starting to dry up, he said. “We’re seeing now a wave of corporate layoffs” that will lower consumer spending and increase the risk of missing earnings estimates, he said.

Depending on how the economy develops, some observers expect more bankruptcy-related claims.

“I expect to see an uptick in claims due to the headwinds many of these companies are still facing,” Mr. Azzara said, adding he expects underwriters to scrutinize companies’ capital, earnings and liquidity.

“I would expect an increase in bankruptcy activity in the next 12 to 18 months, Mr. McGuinness said. “We’ve seen a lot of immature and speculative companies come to the public markets in the last two years,” especially in the SPAC sector, he said, predicting they will not find the capital they require.