Broker mergers slow in changing economy

Reprints

Changes appear to be afoot in the brokerage mergers and acquisitions sector as a significant rise in interest rates and economic uncertainty are likely forcing some buyers to pull back and causing nearly all buyers to proceed more cautiously.

The total number of transactions declined 8% to 987 in 2022, from 1,075 in 2021.

These totals include U.S. and Canadian property/casualty and employee benefits brokerages, third-party administrators and related managing general agent operations, and the tally has been expanded for 2022 to include agencies solely focused on life insurance, investment or financial management, consulting and other business connected to insurance distribution. We collect the information from public announcements, buyer websites and other sources in a consistent manner from year to year, but the count does not include all transactions because many are never announced publicly.

When the newly admitted categories of sellers are excluded, the decline is even more dramatic as the number of transactions on a year-over-year basis declined 17% from 1,066 in 2021 to 885 in 2022.

Last year was a tale of two halves. The robust first half was driven by a built-up inventory of deals yet to be completed and still favorable economic conditions; the buying spree continued as there were 24% more deals done than in the same period in 2021. But as soon as the third quarter began and deal inventories fell, the effect of rising costs of capital was felt and the flow slowed. The deal count in each of the first six months of 2022 was higher than the same time frame in the previous year, but the reverse was true in the final

six months.

Looking at all transactions reported, the 530 reported second-half transactions in 2022 fell by 25% from the prior-year total but were still 24% above the previous five-year average. During the first half of 2021, there were 674 transactions reported compared with 488 for the same period in 2020. In fact, the decline picked up pace as year-over-year 2022 third-quarter results were down 18% while the fourth quarter accelerated to a 30% decline compared with the prior year.

Removing the newly added seller categories to study changes over time on an apples-to-apples basis, there were 482 first-half transactions in 2022, which represented a 32% decline in the sales of retail property/casualty and benefits agents and brokers, wholesalers and TPAs.

Yet, compared with longer-term historical activity, each quarter of 2022 outpaced the previous five-year average, even when the new categories of sellers are excluded, which highlights the “deal bubble” that was 2020 and 2021. Some buyers may choose to suspend pursuing deals going into 2023, and many others will likely take a “slow as you go” approach, though there may be a few that see opportunities of potential reductions in valuations that come from increased costs of capital and concern over a potential recession.

Buyers are broken down into the following categories:

- PE-hybrid — Private equity-backed and private firms with significant outside acquisition financial support

- Publicly traded

- Privately owned

- Bank-owned

- Others

Acrisure LLC continued to report the most activity, with 107 closed transactions, a decline from the 122 transactions completed in 2021 but equal to its long-term average. While PCF Insurance Services followed with the next highest volume at 71 deals, its activity dropped dramatically in the third and fourth quarters. Hub International Ltd. announced 70 transactions, bucking the industry trend with a 13% increase in deals over 2021.

The PE/hybrid group remains the most active group of buyers, occupying each of the top 10 spots (see table) and accounting for 735 of the 987 transactions for the year, fully 74% of all agency transactions. The concentration of deals by the top 10 buyers — as measured in each year independently — were 53% and 51% in 2021 and 2022, respectively. Of the top 10 buyers, only Inszone Insurance Services, which announced 30 more deals; Liberty Co. Insurance Brokers Inc., up 23; and Hub International, up eight, increased their number of deals in 2022. The largest decline in the number of deals among this group was at PCF, down 28; High Street Partners, down 27; and Assured Partners, down 19.

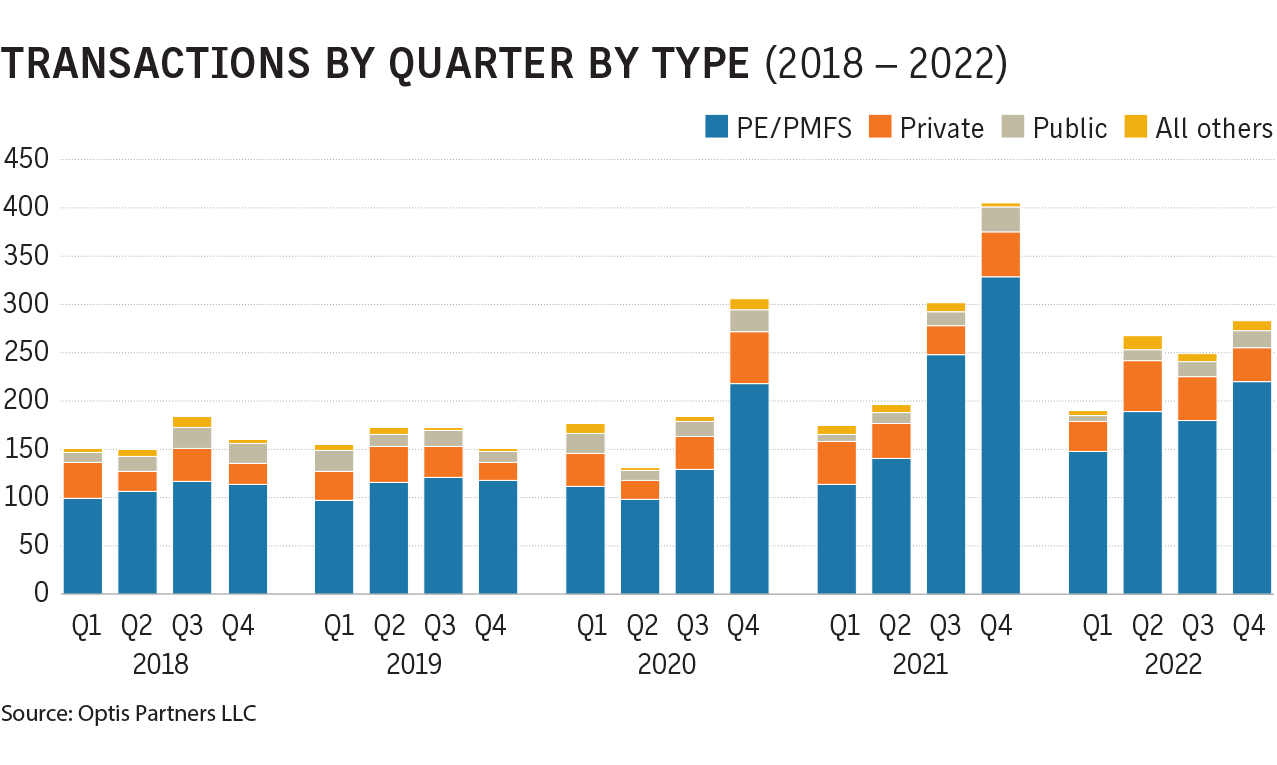

The past three years offer a fascinating look at the industry through the lens of deal activity (see graph). In the first half of 2020, deal activity slowed notably as the world learned how to work in a pandemic. The six quarters that followed produced the greatest number of deals ever, largely driven by fear of a potentially significant increase in capital gains rates, which did not go through. This high-level activity continued in the first half of 2022, but the flow slowed as soon as the third quarter as interest rates rose, inflation concerns were realized, and a possible recession loomed.

Some other statistics from the 2022 activity:

- 36 different PE-hybrid buyers acquired a combined 735 agencies in 2022, an average of 20 transactions each; six PE-hybrid buyers made their first acquisition in 2022.

- There were 66 privately owned firms that acquired a combined 163 agencies, compared with 76 that bought 155 agencies in 2021, an average of 2.5 and 2.0, respectively.

- 72 firms acquired only one agency in 2022, while 36 acquired five or more.

- There were 54 first-time buyers in 2022.

Property/casualty brokers continued to dominate the sell-side M&A landscape, accounting for 557 of the 987 transactions, or 56% of the total. Employee benefits brokers were the second most acquired companies in 2021, with 147 transactions representing 15% of the total. In all, the combination of all property/casualty and employee benefits retail sellers was 834, or 84% of all deals done in 2022.

There were eight firms whose revenue exceeded $25 million sold during 2022.

The M&A scene is in a state of change across all industries including insurance distribution. We can expect to see a slower pace of deals over the next six months as buyers navigate the waters of rising interest rates and economic uncertainty. With that said, some dynamics haven’t changed, namely the continuation of an aging ownership base that must sell at some point and investors with plenty of dry powder.

Steve Germundson, Timothy Cunningham and Daniel Menzer are principals at Optis Partners LLC, a Chicago-based investment banking and financial consulting firm that serves the insurance distribution sector. Mr. Germundson can be reached at germundson@optisins.com or 612-718-0598; Mr. Cunningham can be reached at cunningham@optisins.com or 312-235-0081; and Mr. Menzer can be reached at menzer@optisins.com or 630-520-0490.