Worldwide events hit political violence market

Reprints

Businesses that purchase standalone political violence and terrorism coverage can expect substantial rate increases and tightening capacity as insurers respond to mounting losses and rising reinsurance costs.

Russia’s invasion of Ukraine led to a hardening market, and conditions intensified at Jan. 1 reinsurance renewals, with the effect on insurer political violence and terrorism books of business still evolving, experts say.

Risk aggregations are being scrutinized, and insurers’ net positions are shifting, which will likely lead to further rate hikes, they say. In recent years, political violence coverage has broadened to a widening range of perils, and demand has increased while losses have been more frequent.

The Ukraine war alone caused an estimated insured loss to the war, terrorism and political violence market of between $1.5 billion and $5 billion, not including aviation and marine losses, said Morgan Shrubb, New York-based head of terrorism for Axa XL, a unit of Axa SA.

An uptick in mass shooting events in the U.S., riot losses in South Africa in 2021, increasing social unrest due to the cost-of-living crisis, and recent political uprisings in Brazil and Peru have had a “tail wagging the dog” effect, she said.

“Now that reinsurance costs have gone up, obviously insurers can’t absorb all those losses on their book and have to start increasing rates to keep up with increased costs and increased risk,” Ms. Shrubb said.

Some capacity has retreated from the market because several insurers were unable to negotiate successful Jan. 1 treaty renewals at premiums that would permit them to continue writing the business, said Jen Rubin, New York-based senior underwriting executive and head of war and terrorism at Liberty Specialty Markets, a unit of Liberty Mutual Insurance Co.

Liberty Mutual remains committed to the market but is looking at terrorism and political violence risks with a sharper lens, she said.

“We are seeking rate increases across the portfolio to offset our increased cost of doing business because of the reinsurance rate increases and inflation that we’re seeing in the market,” Ms. Rubin said.

Across the industry many insurers are seeking minimum 20% rate increases, but rates vary based on the individual risk profile and geographic footprint, she said.

Adam Posner, Miami-based head of U.S. terrorism and political violence at Munich Re Specialty Insurance, a unit of Munich Reinsurance Co., said capacity in the terrorism and political violence market remains robust.

The effect on the primary market of reinsurance treaty renewals is still playing out, but “there is still significant capacity in the standalone terrorism market to be able to cater for the large risks,” Mr. Posner said. Munich Re Specialty can deploy $425 million in capacity for a terrorism placement and its appetite hasn’t shifted, he said. For political violence perils, capacity varies depending on the threat level of a country, up to $35 million per risk, he said.

It’s too early to say how policy language could change, he said.

Political violence and terrorism risks are experiencing limitations in coverage, said Tarique Nageer, New York-based terrorism placement advisory leader for Marsh LLC. Russia’s invasion of Ukraine has driven insurer concerns about other geopolitical hot spots such as Taiwan, where there is a “decrease in appetite for political violence cover, with markets looking to reduce their exposures and electing to sublimit perceived higher-risk territories” for operations located there, Mr. Nageer said.

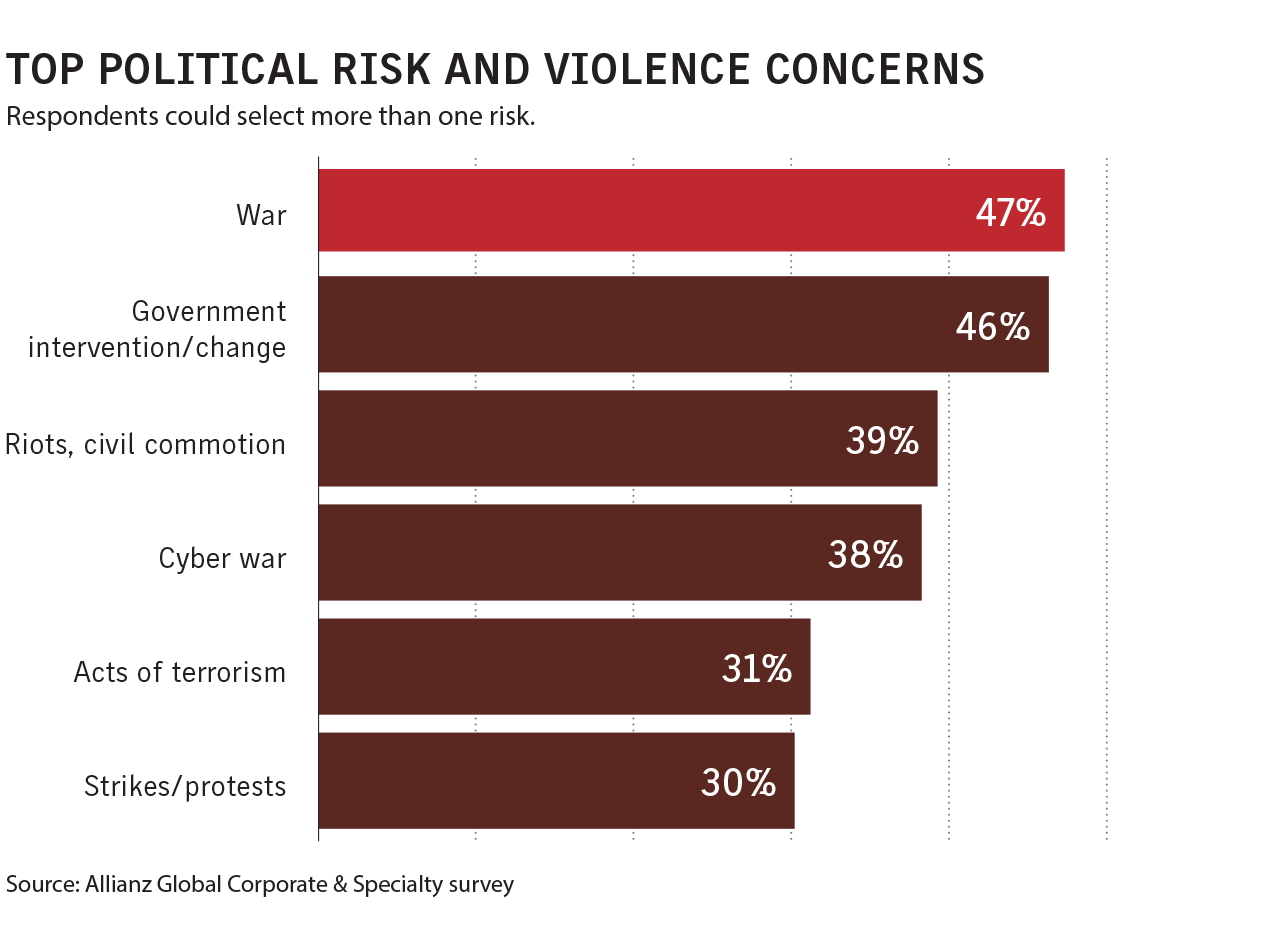

In the past five years, coverage under the political violence umbrella has stretched to include events such as strikes, riots and civil commotion through to war, said Adam McGrath, London-based head of international, political violence, at Mosaic Insurance Holdings Ltd.

Greater awareness of the potential for systemic loss has led to a shift in the breadth of coverage afforded, Mr. McGrath said.

“There’s a clear trend of markets trying to limit extensions for things like strikes, riots and civil commotion” through monetary sublimits and narrowing coverage, he said.

Data and analytics can help businesses continue to secure broad coverage terms from underwriters, but contingent time element coverage extensions are contracting, said Fergus Critchley, New York-based head of crisis management North America at Willis Towers Watson PLC.

“Insurers want a lot more information in order to provide that coverage and they’re really only offering coverage for named customers and suppliers,” he said.

Businesses should align their exposure with the appropriate coverage, “because not all of these products are created equal,” said Jeff Buyze, Fort Lauderdale, Florida-based vice president, national property practice leader, at USI Insurance Services LLC.

“The details matter here because if you pick up any monoline terrorism policy, they’re all going to have different exclusions, wordings or definitions of what terrorism actually is,” Mr. Buyze said. “One line can make the difference between getting paid or not getting paid,” he said.

Big increase in insurance rates prompts review of exposures, risk appetite

Businesses should closely evaluate their exposures and coverage needs in a hardening market as political violence and terrorism threats evolve, experts say.

Policies are highly customizable and businesses can choose which locations coverage applies to, said Jeff Buyze, Fort Lauderdale, Florida-based vice president, national property practice leader, at USI Insurance Services LLC.

Businesses need to understand their risks and vulnerabilities and identify appropriate limits, he said.

“Too many times I see insureds buying to their full total insured values for terrorism across their schedule. They have a good spread of risk. There’s no sense buying, say, $100 million in coverage when they really only need $10 million,” Mr. Buyze said.

Many companies overbuy terrorism coverage, so reducing limits can be an effective way of reducing costs, said Morgan Shrubb, New York-based head of terrorism for Axa XL, a unit of Axa SA.

“Increasing deductibles doesn’t really do anything. It’s a hard market,” she said. Another approach would be to purchase coverage supported by the U.S. federal backstop that was brought in by the Terrorism Risk Insurance Act of 2002, but with property markets still hard, prices are going up and coverage through TRIA is more costly, she said.

Global businesses entering regions with a history of violence and volatility inevitably face associated security and insurance costs in terms of terrorism or strikes, riots and other events, said Adam McGrath, London-based head of international, political violence, at Mosaic Insurance Holdings Ltd.

In the case of strikes and riots, security for soft-target properties is critical, Mr. McGrath said. For example, automatic shutters can immediately protect properties and prevent systemic loss when multiple stores are looted, he said.