Viewpoint: Resilience takes investment

Reprints

As southwest Florida continues its recovery from Hurricane Ian and the insurance and risk management sector debates ongoing concerns about capacity, availability and cost of coverage, the message to policyholders to invest in resilience measures to protect their properties from a changing climate is louder than ever.

Whether it’s upgrading roofs and windows, raising properties on stilts in flood-prone areas, or clearing brush to create defensible space around buildings to slow or stop the spread of wildfire, the strong advice from brokers and insurers is for property owners to take seriously the importance of taking preventive steps. The latest hurricane bears this out.

Despite Ian’s devastation, and the estimated insured losses of $50 billion-plus across the global property/casualty insurance and reinsurance industry, brokers report that newer construction, including metal and tile roofs, proved more resistant to the storm.

At the community level, measures such as upgraded building codes are critical. A 2021 report by the Insurance Institute for Business and Home Safety ranked Florida and Virginia highest in the adoption and enforcement of building codes.

Another story of resilience following the Category 4 storm was that of a little-known 100% solar-powered community — Babcock Ranch — just 12 miles northeast of Fort Myers. Ian, with its record-breaking storm surge and winds up to 150 mph, severely damaged infrastructure such as roads and bridges and parts of the electric grid in local communities. However, according to news reports, the energy-efficient homes and properties of Babcock Ranch survived the storm intact and did not lose power, water and internet. Eco-conscious city living may not yet be accessible or a practical solution for everybody, of course, but it clearly has benefits.

Insurers gradually have been offering incentives to policyholders that invest in mitigation measures, but with inflation pushing up insured values across the board and property rate increases showing no sign of relief, they will need to turn up the volume of their messaging on these efforts. FM Global, for example, in October added to its well-publicized $300 million climate credit for policyholders by launching two climate reporting tools also designed to incentivize investments in climate mitigation.

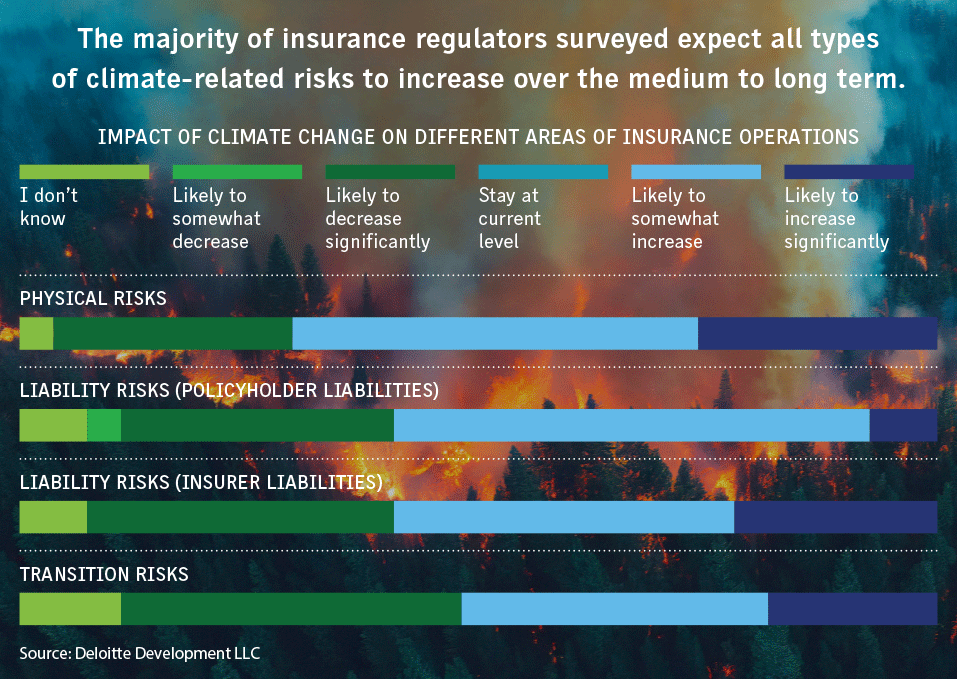

Regulators, meanwhile, have started to add to the pressure on insurers to reward policyholders for their efforts. In California, the Department of Insurance in October introduced new rules requiring insurers to provide discounts to property owners who take wildfire safety and mitigation steps. Under the rules, insurers are required to submit new rate filings within 180 days incorporating wildfire safety standards set by the department and to establish a process for releasing wildfire risk determinations to businesses and residents. Such regulatory mandates are likely to become more widespread as the risks of severe weather events increase and affordable insurance becomes less available in catastrophe-prone areas amid the changing climate.

Many large corporate insurance buyers are already self-insuring to substantial levels, while dealing with even more costly and restrictive coverage, and nobody wants a market that is stymied by regulatory intervention. A mindset of rebuild and recover is not enough. Insurers need to engage proactively with policyholders in order to incentivize them to invest in offsetting climate-related risks so as to avoid the need for regulations telling them how to act. The more transparent this process is, the better insurers and risk managers will be able to mitigate the impacts of climate change.