Surplus lines market attracts more business

Reprints

Wholesale commercial insurance markets are seeing increased business as policyholders, brokers and prospective buyers seek alternatives to continuing firm primary market rate conditions and capacity constraints.

The growth in the nonadmitted market was reflected in comments from sources attending this year’s Wholesale & Specialty Insurance Association’s Annual Marketplace in San Diego in September and in a sector report from A.M. Best & Co. released just ahead of the conference.

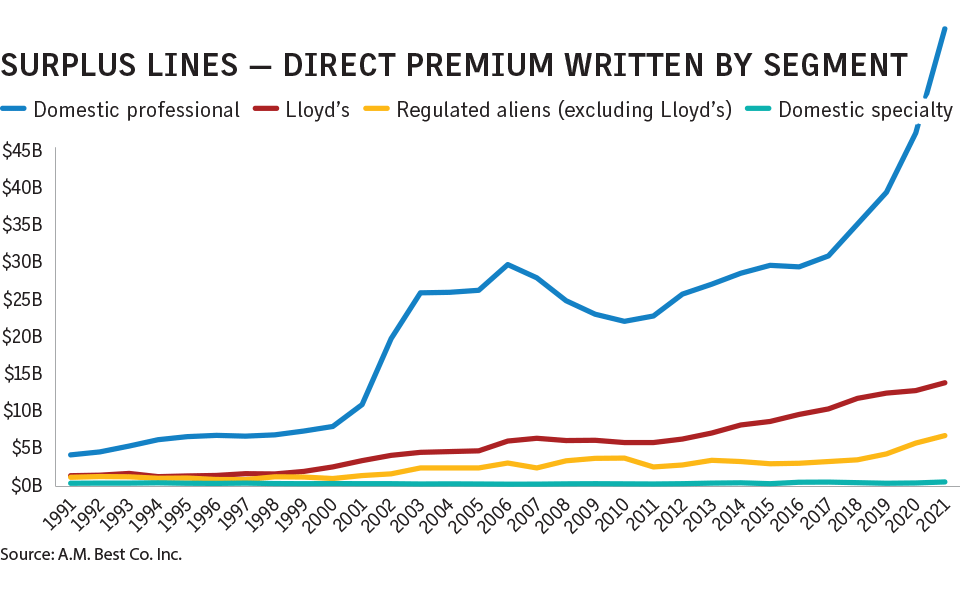

Total U.S. surplus lines direct premiums written rose to a record $82.65 billion in 2021, according to Best. The 25% year-over-year premium growth last year was the largest rise since 2003. Best’s data also showed surplus lines premiums growing to their current level from just $11.66 billion in 2000.

CLICK IMAGE TO ENLARGE

The largest players in the surplus lines market are insurers at Lloyd’s of London, with an aggregate market share of 16.6%; followed by Berkshire Hathaway Inc. and American International Group Inc. both at 5%, according to Best.

While the steep rate increases in the primary market appear to be moderating, rates are still rising and capacity withdrawals from troubled areas such as catastrophe-exposed property risks have made the nonadmitted market more appealing, sources say. Surplus lines insurers face fewer regulatory constraints than admitted insurers but often charge higher premiums.

As a result of the hardening market, business has been flowing into surplus lines insurance markets from the primary side as policyholders and brokers seek alternatives.

“We have seen a large influx of business into the excess and surplus marketplace,” said John Anthony, senior vice president for excess and surplus wholesale, contract property and casualty, excess and umbrella in Scottsdale, Arizona, for Nationwide Insurance Co.

Tumult in the primary markets has prompted policyholders and brokers to explore other options.

“A number of retail brokers were challenged with the dramatic change in the market conditions and needed to find capacity or product expertise in certain lines of coverage,” said Jack Kuhn, Berkeley Heights, New Jersey-based president of Westfield Specialty, a unit of Westfield Insurance Co.

Exposures not adequately covered by primary markets can be addressed through the excess markets, experts say.

“We see more buyers moving into excess and surplus because of the flexibility we have around rate and form,” said Bob Mescher, senior vice president at Admiral Insurance Group, a unit of W.R. Berkley Corp. in Mount Laurel, New Jersey. “As a marketplace, excess and surplus lines is set up to respond to the business that doesn’t fit” in the general commercial insurance marketplace.

Ben Johnson, Boston-based senior vice president, wholesale field operations, for Liberty Mutual Insurance Co.’s global risk solutions division, said that in addition to macroeconomic pressures and primary coverage rate hikes, continued consolidation in the retail brokerage market by private equity groups and “roll-up” agencies has also helped push business into the wholesale markets as choices dwindle.

Most sources suggested that firm rates and capacity constraints are likely to continue in the wholesale and specialty insurance market for the remainder of this year and into 2023, even as some areas moderate.

“The market is still tight but more stable than it has been in recent years,” said Bill McElroy, portfolio director for casualty with Aspen Insurance Holdings Ltd. In New York. “Capacity is still tight in certain areas, and we expect that to be the case for the balance of the year and into 2023. We’re not expecting any major shifts.”

Wholesale markets continue to benefit from capacity issues in the primary market.

“We’re very bullish” that market conditions will continue in the short term absent any major capital shifts in the primary market, Mr. Anthony said. He added that despite the exodus of players and capacity from catastrophe-exposed coastal properties, Nationwide still has measured appetite in the space.

Some sectors may see rate moderation.

“We’ll continue to see rate moderation on desirable classes of business, including commercial construction and manufacturing,” said Bill Wilkinson, president of national casualty brokerage in Alpharetta, Georgia, for Risk Placement Services Inc.

While in general terms rate increases continue to exceed loss cost trends across most of Axis Capital Holdings Ltd.’s portfolio, there is evidence of some lines seeing moderation, such as public companies directors and officers liability coverage, said Vincent Tizzio, CEO of Axis Specialty Insurance and Reinsurance.

Other lines may continue to be challenging.

“This will be the hardest property market we’ve seen since Katrina. I see a significant capacity crunch in property,” said Liberty’s Mr. Johnson.

Advances in technology tools play bigger role in underwriting

Policyholders and brokers are using technology to help differentiate submissions amid capacity constraints and hard-market conditions, while insurers are also turning to technology to bolster underwriting and growth, according to experts at the Wholesale & Specialty Insurance Association’s Annual Marketplace in San Diego last month.

The variety and availability of technology tools “just keeps expanding,” said Vanessa Sullivan, New York-based senior vice president, excess and surplus underwriting manager, for Munich Re Specialty Insurance, part of Munich Reinsurance Co. She added brokers are also embracing technology and analytics to a greater degree and that “as an underwriter, I’m always looking for that extra data.”

Such new tools and information can be used to differentiate submissions, said Christa Nadler, Chicago-based area executive vice president, property broker, for Risk Placement Services Inc., a unit of Arthur J. Gallagher & Co.

“Ten years ago, we couldn’t open up Google Earth to take a look at what the roof looks like. Now, we can include in our submission a picture of the roof,” where previously such an image might have required the use of an aircraft, she said.

Technology can also help fuel growth and sharpen underwriting among insurers.

“We’ve made large investments in advanced analytics, as well as technology platforms,” to bolster underwriting processes, said John Anthony, senior vice president for excess and surplus wholesale, contract property and casualty, excess and umbrella in Scottsdale, Arizona, for Nationwide Mutual Insurance Co.

“We’re doing a lot on the information technology side to support the business to be as efficient as possible. We’ll continue to make those investments,” said Jack Kuhn, Berkeley Heights, New Jersey-based president of Westfield Specialty, a unit of Westfield Insurance Co. He added that such investments would be “significant” as the company builds out its capabilities for new lines of coverages during the coming years.