Greenwashing comes under fire

Reprints

Businesses in financial services and other sectors could find themselves in the crosshairs of so-called greenwashing allegations as the regulatory focus on environmental, social and governance-related disclosures intensifies.

Heightened enforcement activity includes recent charges brought by the U.S. Securities and Exchange Commission against the investment management arm of BNY Mellon for alleged misstatements and omissions concerning its ESG funds. BNY Mellon Investment Advisor Inc. agreed in late May to pay a $1.5 million penalty to settle the SEC charges.

Companies making climate-related claims and promises about the sustainability of their operations or investment recommendations based on ESG factors could be the target of litigation exposing insurers to potential directors and officers liability claims, experts say.

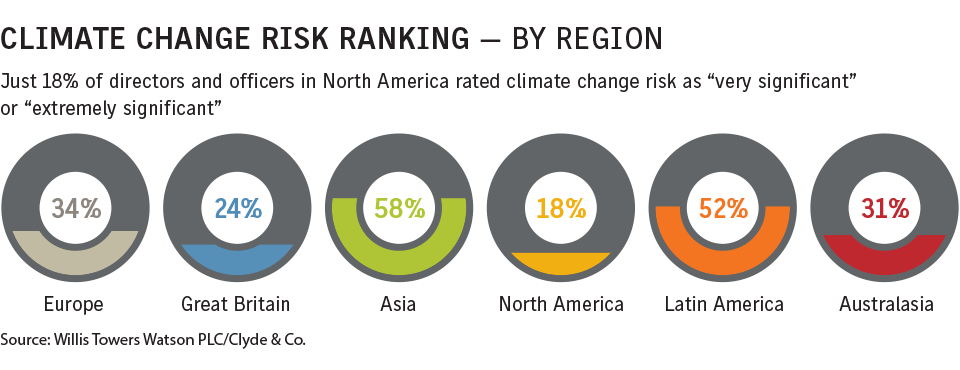

So far, there have been just a handful of claims, but the complexity of rules and emerging guidance coming from the SEC, the United Nations 17 sustainable development goals and United Kingdom net zero transition plans create “areas for companies to trip up,” said James Rizzo, New York-based underwriter for U.S. executive risk at Beazley PLC.

Greenwashing describes when a company or organization markets its operations, products or initiatives as more environmentally friendly than they actually are.

A greenwashing claim could come down to an overpromise, an error or omission in the execution of a service, or a failure to achieve a certain goal, Mr. Rizzo said. “All these things lead to a disappointment, which can ultimately lead to a negative reaction in a company’s stock, shareholder litigation, derivative matters and regulatory litigation,” he said.

In terms of insurance coverage, the obvious target would be D&O policies, said Dennis Artese, shareholder at Anderson Kill in New York.

“We expect to see certain hurdles but in many of these greenwashing cases it will be covered and at a minimum will be defended,” Mr. Artese said.

Other insurance coverages such as reputational risk, errors and omissions, product liability, environmental and commercial general liability could also come into play, sources said.

Under any type of professional liability policy, the coverage trigger is an act, error or omission in that service that could give rise to a claim, said Stephanie Snyder Frenier, Chicago-based senior vice president, business development leader of professional and cyber solutions, at CAC Specialty.

“If an investment adviser, for example, recommends things that have greater ESG initiatives and they in fact don’t and it is an error or omission, there is a potential for coverage under the policy,” depending on terms and conditions and the allegations made, Ms. Frenier said.

Chubb Ltd. CEO Evan Greenberg warned insurers to expect shareholder lawsuits alleging greenwashing against their D&O policyholders and that net zero disclosures pose a particular challenge to the industry.

The net zero commitment “sounds great in the beginning, but you’re going to have to disclose very quickly what’s your progress. ... If it’s just vague words there are going to be a lot of shareholder suits because companies are overpromising,” Mr. Greenberg said during S&P Global Ratings Inc.’s 38th annual insurance conference last month.

A shareholder lawsuit filed in 2021 against bed and mattress manufacturer Sleep Number Corp. following winter storms in Texas and Louisiana illustrates how a company’s statements on their resilience in extreme weather could lead to D&O claims, said Kevin LaCroix, executive vice president in Beachwood, Ohio, for RT ProExec, a division of R-T Specialty LLC.

The suit, filed in U.S. District Court in Minneapolis, alleged that Sleep Number Corp., its CEO and chief financial officer made false and misleading statements and failed to disclose that the company had suffered a severe disruption in its supply chain for mattress foam as a result of winter storm Uri.

The company had touted its integrated supply chain while attempting to assuage investor concerns about its ability to meet surging customer demand during the COVID-19 pandemic, according to the complaint filed last December.

That example of a company being knocked offline by an extreme weather event raises the question: “Are there going to be those kinds of claims?” Mr. LaCroix said.

With the significant increase in greenwashing allegations, it’s “reasonable to assume litigation will increase and insurers will be much more cautious of writing policies,” said Michael Miguel, Los Angeles-based principal at McKool Smith.

Policyholders should be taking a much harder look at their insurance coverage and how it would respond, Mr. Miguel said.

In a 2014 case, Meyer v. Jinkosolar, 2nd U.S. Circuit Court of Appeals in New York held that shareholders could proceed with their greenwashing lawsuit against solar panel manufacturer Jinkosolar Holdings Co. Ltd., its officers and directors, and underwriters. Shareholders alleged the company made materially misleading statements in its public offering prospectus about its compliance with environmental regulations at a production facility in China. The case was subsequently settled for more than $5 million.

ESG trend raises cover questions

Businesses should ensure they can back up their climate-related promises and review their insurance coverage for specific ESG references, experts say.

When it comes to being green, there is a lot of gray, said Stephanie Snyder Frenier, Chicago-based senior vice president, business development leader of professional and cyber solutions, at CAC Specialty.

“Organizations need to be mindful and cautious around what they are doing and representing to avoid potential liability,” Ms. Frenier said.

Companies should check to see if their insurance policies address ESG and greenwashing directly, said Brian S. Scarbrough, a partner with Jenner & Block LLP in Washington.

They should “see if insurers are trying to reduce their liability for these types of claims and, conversely, if insurers are putting in affirmative coverage grants for these types of claims,” Mr. Scarbrough said.

More insurers are asking about a company’s ESG disclosures in the underwriting process, but because there is no universal standard or regulatory framework there’s no way to verify if a company is meeting its promises, said Sojee Kim, head of claims at Founder Shield, a New York-based brokerage.

“Once there is more of a regulatory framework it will be easier and much more of a requirement when carriers are underwriting risk,” Ms. Kim said.

Companies should provide concrete examples of their ESG commitments that stand behind what they are saying, said Eric Jesse, a partner at Lowenstein Sandler LLP in Roseland, New Jersey.

This can help insurers get more comfortable that they are a good risk, Mr. Jesse said.