Insuring fintech firms presents challenges

Reprints

Financial technology companies — from investment, lending and payment platforms to robo-advisers, insurtechs and cryptocurrency exchanges — are taking root, as the pandemic has accelerated a shift to digital operations.

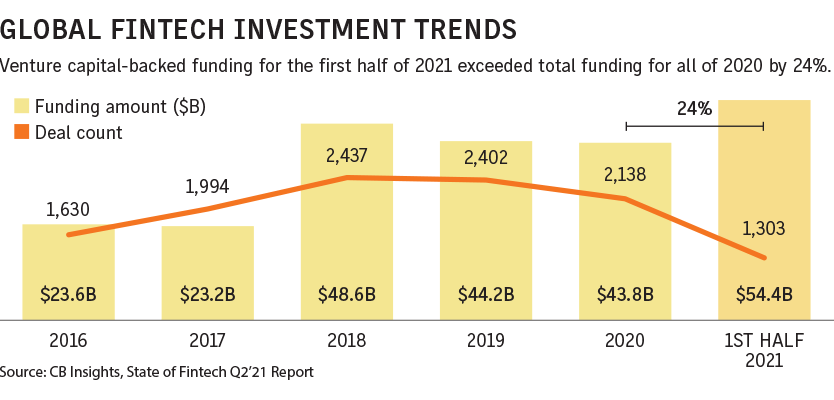

Global venture capital-backed fintechs raised a record $30.79 billion across 657 deals in the second quarter of 2021, a 30% increase from the first quarter, according to a July report from CB Insights. Total funding in the first half of 2021 exceeded all funding raised in 2020 (see chart).

But insuring these innovative companies, many of them startups, can be challenging due to the combination of financial, human and digital risks they present and changing regulatory exposures they face, experts say.

Claudia Ramone, New York-based vice president, alternative asset management at EPIC Insurance Brokers and Consultants, said insurer risk appetite for fintechs is limited, with only a “select” number of insurance markets willing to write the risks.

In the case of a technology company such as a software developer, “I would have 10 markets that I’m consistently able to go to,” Ms. Ramone said. But when it comes to fintechs only three or four markets, “maybe 25% or 30% of your market pool would have an appetite,” she said.

What makes a fintech challenging is that it is both a financial institution and also a technology company, said Thomas Tierney, FINPRO financial institutions practice leader at Marsh LLC in New York.

“You have elements of financial institution errors and omissions coverage, technology E&O coverage and cyber E&O coverage all embedded within the same risk profile. How you effectively manage that risk and transfer it to reinsurance has always been a challenge,” Mr. Tierney said.

Fintechs in the payments, digital banking, insurtech and business processing sector tend to be viewed more favorably by insurers, while it can be more difficult to secure coverage for cryptocurrency, nonbank lenders, robo-advisers and online broker dealers. “It requires more transparency and conversations with insurers,” he said.

As well as E&O, important coverages for fintechs include directors and officers liability, employment practices liability, cyber liability and fiduciary insurance, brokers say.

Securing adequate and affordable E&O coverage is the most challenging piece for fintechs, said Jacob Decker, Seattle-based vice president and director of financial institutions at Woodruff Sawyer. Many existing policies were not written with new business models in mind, so how they define a fintech’s products and services may be inadequate and may not fully encapsulate what they do, he said.

Another concern for early-stage companies is the cost of coverage. “It’s high-risk insurance. If you’re an early-stage company and you just raised an A round or a C round it’s very likely you don’t have a budget that would be sufficient to justify buying that type of cover yet,” Mr. Decker said.

Insurance pricing for fintechs is in the multiples of what it would be for a traditional financial services company, said Scott Warren, assistant vice president at Founder Shield, a New York-based insurtech company that in July was acquired by broker BRP Group Inc.

Venture capital and private equity firms provide a reference point, he said. For fintechs with a technology interface “the pricing is multiples of that. We see anywhere from $30,000 to $100,000 in premium for a base level $1 million limit in this space,” Mr. Warren said.

Tim Braun, New York-based head of financial institutions at Axis Insurance, U.S., said that underwriters consider three key components: the capital, investments and investors behind the startup fintech; its leadership and skillset; and its corporate or reputational risk.

“The fintech company has to have some understanding and appreciation of these risks and a way to manage them,” Mr. Braun said.

Startups tend to have a high failure rate, which can make fintechs a less attractive risk for insurers because they may not be around long enough to generate renewable income, premium and commissions, said Scott Whitehead, managing director at Markel Insurtech Underwriters, a unit of Markel Corp. in Glen Allen, Virginia.

Another factor is that many startups haven’t started generating steady revenue when they are required to get insurance. “That’s a practical issue for an underwriter in trying to charge the right rate,” Mr. Whitehead said.

David Roque, Fort Lauderdale, Florida-based vice president at USI Insurance Services LLC, said many cryptocurrency exchanges and digital asset companies have hit brick walls with insurance markets.

“Carriers aren’t familiar with the territory and the lack of regulatory involvement. It scares a lot of insurers away,” Mr. Roque said.

Insurers tend to be more comfortable when the cryptocurrency tokens traded have been in the industry for some time, when they understand the structure, and when they know the states and countries in which the cryptocurrency companies operate, he said.

Fintechs need to keep on top of regulatory compliance because the regulatory environment is changing rapidly, said Jim Wetekamp, CEO of Atlanta-based Riskonnect Inc., a risk management technology company. How regulations are interpreted and understanding how cryptocurrencies fall into the regulatory framework are important considerations, Mr. Wetekamp said.

Data breaches put focus on digital risk management

Fintechs must increase their efforts to manage digital risks as recent cyber events, such as the Colonial Pipeline ransomware attack, have exacerbated an already-difficult cyber market, experts say.

Data security and privacy exposures are a critical risk for fintechs that interact with customers through a platform or web interface, said Jacob Decker, Seattle-based vice president and director of financial institutions at Woodruff Sawyer.

“Online financial services companies are attractive targets for hackers and criminals. They represent potential honeypots of information that would be of interest to them,” Mr. Decker said.

If a fintech is a fiduciary of data, especially in the consumer and retail sector, it can hold tremendous amounts of information, said Claudia Ramone, New York-based vice president, alternative asset management, at EPIC Insurance Brokers and Consultants.

For one fintech client with more than 25 million personally identifiable information points, finding coverage in the cyber market was “extremely difficult,” she said.

“It’s like a dental exam every time you submit an application. It’s very tedious. The market has pulled back tremendously and they’re asking so many questions. I’ve seen limits reduced, retentions increase. Pricing is up a minimum of 15%, north of 50%,” Ms. Ramone said.

Digital risk is a top concern for financial services due to the fraud environment and their fiduciary responsibility, said Jim Wetekamp, CEO of Atlanta-based Riskonnect Inc. Fintechs could also face third-party risk if they outsource services, he said.