Comp outlook shifts amid rapid changes

Reprints

The uncertainties of COVID-19, unemployment, aging workers, national proposals to raise the minimum wage and a decline in interest rates, are set to change the workers compensation market, experts say.

The pandemic is a leading factor in what’s to come, they say, having already prompted a wave of COVID-19 presumption laws, executive orders and pending proposals in more than 20 states as of February. The legislative actions mark a first step into the realm of infectious disease compensability for many states.

“COVID has been the big wild card,” said Mark Moitoso, Atlanta-based risk practices leader for Lockton Cos. LLC, on how the disease will affect claim activity and future rates.

The COVID-19 presumption laws have “changed how folks think about comp,” said Matt Waters, Boston-based executive vice president and general manager of middle markets for property/casualty at Liberty Mutual Insurance Co.

Data collection when it comes to COVID-19 claims has been essential, experts say.

“We are collecting COVID claims to see what they look like,” said Jeff Eddinger, Boca Raton, Florida-based senior division executive for the National Council on Compensation Insurance, which has released some data.

In studying third-quarter 2020 industry figures, NCCI found that 20% of COVID-19 claims reported an inpatient hospital stay, with 19% of those claims requiring intensive care services. The cost of hospital stays averaged $38,500.

Most claims, however, “tend to be mostly inexpensive,” Mr. Eddinger said, adding that NCCI will continue to examine the costs associated with the infectious disease and what that will mean for rates.

Meanwhile, there remains uncertainty about the duration of the pandemic, said Mauro Garcia, Schaumburg, Illinois-based technical director and head of workers compensation underwriting for Zurich North America.

“COVID is going to be a driver” of the future of the workers comp market, Mr. Garcia said. “There’s a lot of uncertainty on the impact that COVID is going to have.”

On renewals in early January, experts predicted that this year would see a reversal of the trend of flat or lower renewals for workers comp coverage.

“In the rate environment we are starting to see it tick up from a flat renewal to the low single digits” on average, said Rob Stein, New York-based middle market client segment leader for Aon PLC. “This is a reverse trend from the large decreases that we have seen.”

Low interest rates have caused the industry to “shift gears and focus on the underwriting results,” Mr. Garcia said. “You can’t rely on the investment income for a long-tail line like workers comp to boost profitability.”

Dan Aronson, New York-based U.S. casualty practice leader for Marsh LLC said, “The interest rate concern is a main driver as to why carriers are looking for increases in rate.”

“It’s driven by (the) interest rate environment that continues to get worse for carriers,” he said. “Some of the rhetoric as to why rates are going up is the unknown of COVID. What we have seen so far is while COVID claims are up, core operational claims are down. … COVID claims are not as significant as they could have been.”

“You have to make an underwriting profit because you can’t make an investment income,” said JJ Ihrke, Minneapolis-based head of analytics and chief scoring officer at Insurity LLC, a data analytics company whose workers comp trends report for January 2021 highlighted interest rates as a key driver for higher comp premium going forward.

Meanwhile, adding to the effects of the pandemic are U.S. employment figures — and related total workers compensation premium. After plummeting last March amid government lockdowns to slow the spread of the coronavirus, the economy ticked up gradually in the months that followed. NCCI in its January economic outlook report predicted that the economy is likely to recover more “slowly” this year than in the later months of 2020.

Permanent job cuts are also an issue: At year-end 2020, four out of five lost jobs were concentrated in service sectors, characterized by high physical proximity and low essentiality, with two out of five lost jobs in leisure and hospitality, according to the NCCI report.

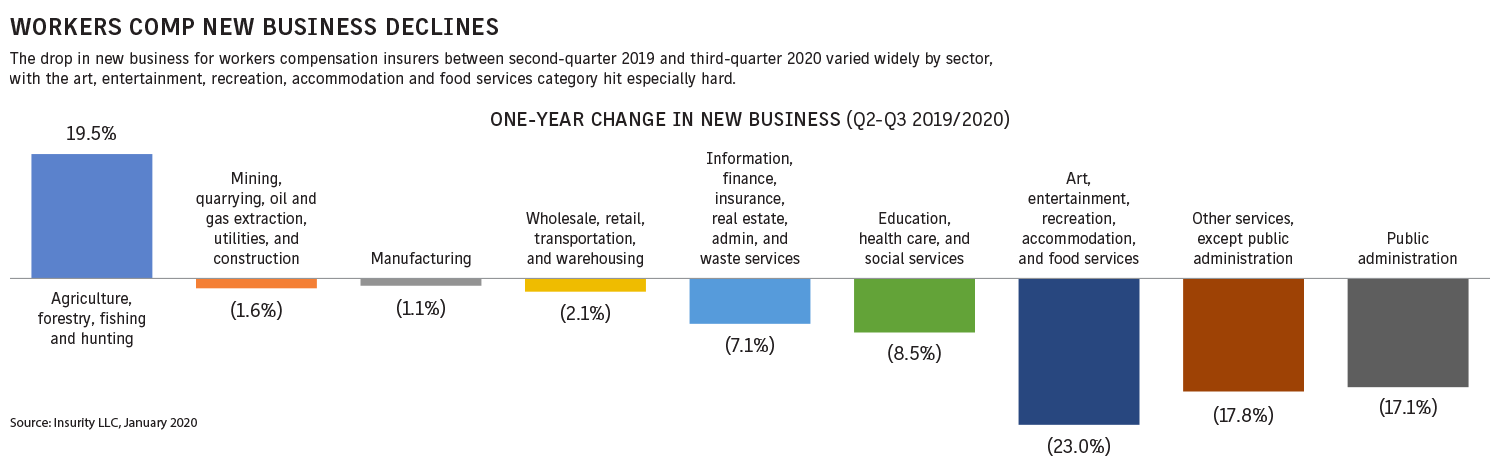

“The pandemic is really causing consternation” in the market, said Mr. Ihrke, whose trends report also pegged job losses as having a major effect on workers comp business. (See chart.)

CLICK IMAGE TO ENLARGE

“New business quotes are down. With new business down … you have to maintain your renewal business. On the surface it looks like your renewal business was OK, but you will be returning a lot of premium to those policyholders because there were no losses. That’s what we are expecting ... a lot of those workers aren’t working,” he said.

A national proposal to increase the minimum wage is another issue that could affect workers comp going forward, according to Robert Hartwig, clinical associate professor and director of the Risk and Uncertainty Management Center at the University of South Carolina in Columbia.

Nearly half of the states each year have increased their minimum wage for the past several years, Mr. Hartwig said in an e-mail. With the Congressional Budget Office projecting that a rise in the minimum wage to $15 per hour would result in 1.4 million job losses, “it’s difficult to say what the net/net of this is for (worker comp) insurers,” he added. “The increase in premium exposure due to the increase in the minimum wage will be partially offset by job losses among the same categories of workers.”

The aging workforce is also contributing to the market conditions, said Mr. Waters of Liberty Mutual. In 2021, 25% of workers are over the age of 55, he said.

“In 2009 that was 12%. ... With an aging workforce you get a slower return to work and an onslaught of comorbidities, and that will only increase severity,” he said.

Angela Childers contributed to this report.

Read Next

-

Research & Rankings: Workers Compensation

CLICK IMAGE TO ENLARGE