Climate change shines light on risk management

Reprints

Risk managers face evolving climate-related liabilities and exposures as they grapple with rising losses from unusual weather events and rapidly changing climate policies in the United States.

The raised bar on regulation and disclosure requirements and how companies prepare for climate risks comes amid greater investor scrutiny of their exposures to environmental, social and governance issues, experts say.

It also comes as governments, businesses and investors accelerate efforts to transition to a greener economy.

The cumulative effect of recent weather disasters, such as the February polar vortex and winter storm that hit Texas and the South, causing widespread power outages and billions of dollars of damage, has brought management of these risks into sharp focus.

Last year was memorable for many reasons, said Joseph Gates, chief risk officer at American Family Mutual Insurance Co. in Madison, Wisconsin.

In addition to historic wildfire events in the western United States, severe convective storm activity and a derecho that hit Iowa and Illinois, the year saw a record hurricane season, he said.

Natural disasters in the U.S. caused $95 billion in economic losses in 2020 with $67 billion in insured losses, versus $51 billion in economic losses and $26 billion in insured losses in 2019, according to data from Munich Reinsurance Co.

Even if a specific weather event cannot be tied to climate change, the increases in frequency and severity of losses must be recognized, experts say.

With accelerating wildfire, hail and winter storm events “what we’re seeing is that there are new asset exposures that haven’t really been contemplated,” said Amy Barnes, London-based head of sustainability and climate change strategy at Marsh LLC.

As a result, risk managers have to re-evaluate their portfolio and modeling, she said.

“Financial planners say the past is not always a guide to the future, and that is really proving to be the case with a lot of the modeling that we do around natural catastrophes,” Ms. Barnes said.

In March catastrophe modeler Risk Management Solutions Inc. said it will incorporate forward-looking analysis of climate change into its major catastrophe risk models, including its North Atlantic hurricane model, from June.

Swiss Re Ltd. analyzes not just historical trends and loss experience but increasingly forward-looking climate-based projections in its underwriting, said Pranav Pasricha, New York-based global head of property and casualty solutions at the reinsurer.

“This might mean that, based on the peril or region, we may consider a longer or shorter time period for our models that more accurately reflects our view of how climate change may influence the frequency or severity of that peril,” Mr. Pasricha said.

The unprecedented winter storm that blanketed Texas caused widespread damage, said Jennifer Waldner, Houston-based chief sustainability officer at American International Group Inc.

“The state’s independent power grid failed. It left millions of people without heat or power for many days; many were left to deal with frozen and busted pipes, and about half the state’s population was without potable water. Many things went wrong,” she said.

Ms. Waldner made the comments during a webinar hosted last month by the Institute of International Finance and EY Global Insurance practice.

“It’s clear there’s much more work to be done to advance climate adaptation initiatives to help communities in building to withstand the physical impacts of climate change,” she said.

Policy shift

As weather and climate-related losses continue to exact a growing toll on businesses and their insurers, the Biden administration has placed environmental, social and governance issues and climate change firmly on its agenda.

On Jan. 27, President Joe Biden issued executive orders mandating that climate change must be at the center of national security and foreign policy. This followed actions taken on his first day in office, such as rejoining the Paris climate agreement, canceling the Keystone XL pipeline permit and reinstating numerous environmental regulations rolled back by former President Donald Trump.

Another executive order, issued by President Biden on Feb. 24, is aimed at making supply chains in the U.S. more resilient, diverse and secure. It references threats to supply chains from “climate shocks and extreme weather events,” among the various conditions that should be reviewed.

ESG and climate change are no longer just a discussion or a societal issue but are fundamentally driven by government, said Atul Vashistha, founder and chairman of Supply Wisdom, a risk intelligence company based in New York.

The trickle-down effect started with a March 3 announcement by the U.S. Securities and Exchange Commission’s examinations division that said the agency “will need to see firms integrate climate and ESG considerations into their disclosures and into their practices related to investments,” he said.

In its statement, the division said it will review “whether firms are considering effective practices to help improve responses to large-scale events.”

On March 4, the SEC announced the creation of a climate and ESG task force in its enforcement division.

Climate change has also become a focus of the U.S. Federal Reserve, said Nigel Brook, a London-based partner at Clyde & Co. The development is not just because of the change in administration but because “it’s more and more obvious that this is a risk affecting financial institutions more broadly,” he said.

The situation is dynamic, with a lot of change, and “risk managers have to get ahead of it,” said Vince Morgan, a partner at Houston-based law firm Bracewell LLP and a past chair of the insurance law section of the State Bar of Texas.

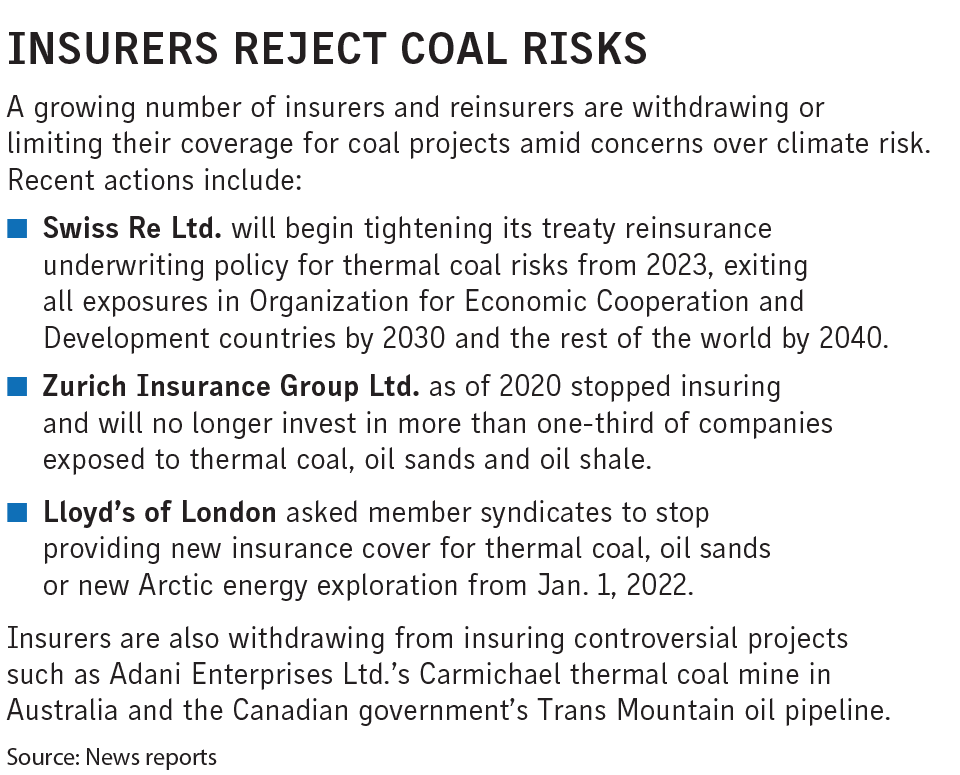

CLICK IMAGE TO ENLARGE

Like the tobacco litigation that took awhile to work its way through the courts “you’re going to see people raising (climate) issues in all kinds of ways that you can’t predict,” Mr. Morgan said (see related story).

In addition to enforcement and regulatory changes, there will be changes as President Biden appoints federal judges, he said.

Pricing challenges

Meanwhile, risk managers looking to better mitigate the financial effect of climate risks continue to navigate challenging commercial insurance market conditions.

In a tightening market it is more difficult to place insurance coverage, and the greater the risk, the harder it is to place the coverage, said Katherine Klosowski, global vice president of natural hazards and structures at FM Global, in Johnston, Rhode Island.

Companies need to protect against the damage of climate change, because “they may not be able to get full insurance coverage for that risk,” Ms. Klosowski said.

Technology is playing a growing role in helping companies understand, evaluate and reduce climate risks, she said (see related story).

Insurers are in a difficult spot in terms of selecting the right risk or binding the right coverage at the right price, said Scott Ritto, vice president of risk management at Kilroy Realty Corp. in Los Angeles.

“Sometimes we say this market is hardening because insurers have paid on losses that they’re trying to claw back or to collect premium back to make up for the losses they’ve paid, but they have to look at the future losses as well,” Mr. Ritto said.

It is important for businesses to make sure their insurers understand exactly what they’re doing to manage the physical and reputational risks related to the climate, he said.

Insurers have a role to play to make sure that communities are resilient moving forward with the expectation that the climate is going to be more volatile than it has been in the past, said Mr. Gates of American Family.

“As best we can, we’re responding to try to strike that right balance between the risks we’re onboarding to the company and the premium that we’re taking to offset that,” he said.

Natural catastrophe risks may become “less insurable” in the future due to climate change, a rise in insurance density and economic growth, analysts at Fitch Ratings Inc. said in a report Feb. 22.

Policyholders may become unwilling or unable to pay for costly natural catastrophe protection, which could lead to a gradual withdrawal of insurance for natural catastrophe risks, Fitch said.

Read Next

-

Technology addresses climate risk

Improved data and rapidly developing technology are helping companies better manage climate-related risks, with satellite imagery, internet of things sensors and machine learning being deployed.

Related Stories

Most Read in Risk Management

-

2. Judge dismisses some of Marsh unit’s counterclaims against former exec

-

4. Jury awards $3M to USI in broker poaching suit against Lockton