Terrorism insurance backstop renewal helped keep rates down

Reprints

The reauthorization of the federal terrorism insurance backstop early this year helped create favorable terrorism insurance pricing for most policyholders, according to a report released Wednesday by Marsh L.L.C.

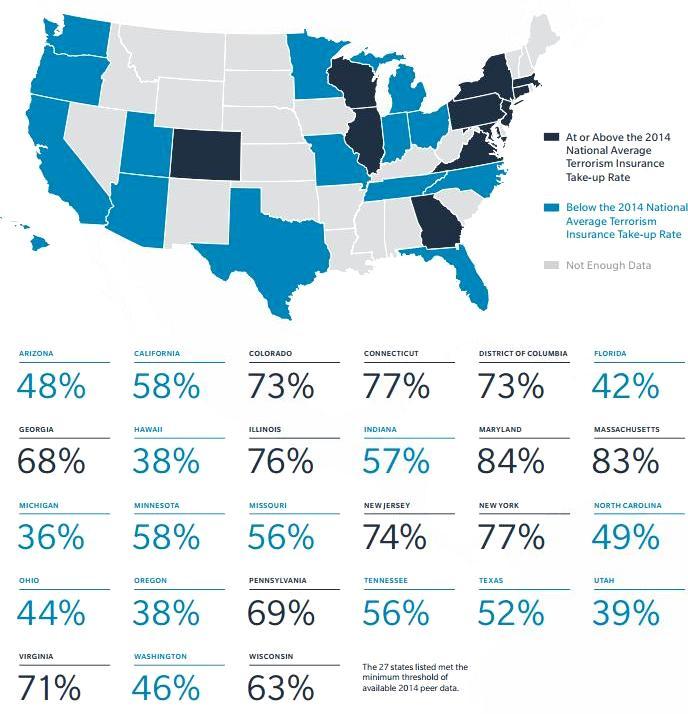

Marsh's “2015 Terrorism Risk Insurance Report” found that uncertainty over renewal of the program, which was created by the Terrorism Risk Insurance Act of 2002, led to a slightly lower takeup rate for terrorism insurance in 2014 — 59% — than had been the case in 2013 and 2012, when takeup rates stood at 62% for each year.

The program expired temporarily on Dec. 31, after lawmakers failed to move on reauthorization legislation before recessing. Congress passed legislation extending the program through 2020 in early January.

The reauthorization “blunted any short-term increase in pricing that may have been caused by the law's temporary lapse,” according to the report.

The report also found that among 17 industry segments surveyed, education organizations had the highest takeup rate at 82%, while energy and mining had the lowest at 38%. Policyholders in the Northeast had the highest takeup rate among regions at 74%, while those in the South and West had the lowest at 54%, according to Marsh.

The combination of a renewed federal terrorism insurance backstop as well as “robust” flows of capital into insurance and reinsurance, among other things, created “pricing conditions favorable to most insureds,” said Marsh. “Most insureds are seeing rate and premium decreases as well as coverage improvements, mostly driven by a competitive marketplace.”

Read Next

-

TRIA's temporary lapse sparks interest in private coverage of terrorism risks

The temporary lapse of the federal terrorism reinsurance backstop has spurred growth in the stand-alone market, with greater buyer interest in purchasing private insurance and more insurers offering private coverage of the risk, brokers and insurers say.

Related Stories

-

TRIA's temporary lapse sparks interest in private coverage of terrorism risks

-

Private terrorism insurance coverage costs fall sharply amid competition

-

Insurers expand terrorism coverage offerings as private market softens

-