Commercial marijuana insurance market grows as premiums rise, more states legalize pot use

Posted On: Feb. 16, 2023 12:00 AM CST

As the legal use of cannabis for both medicinal and recreational purposes spreads to more states with each election cycle, commercial insurance for cannabis operators is finally becoming easier to obtain and afford, as more insurers move into the sector.

Line sizes for property coverage have increased, and professional coverages, such as directors and officers liability insurance, have fallen in price, experts say. Still, contract language continues to be an issue in a sector dominated by manuscript policies and specific lines can see challenges, such as crime policies.

The wider availability of coverage and lower pricing are a relief for buyers in a sector that chafed under high rates and constrained supply as recently as two years ago.

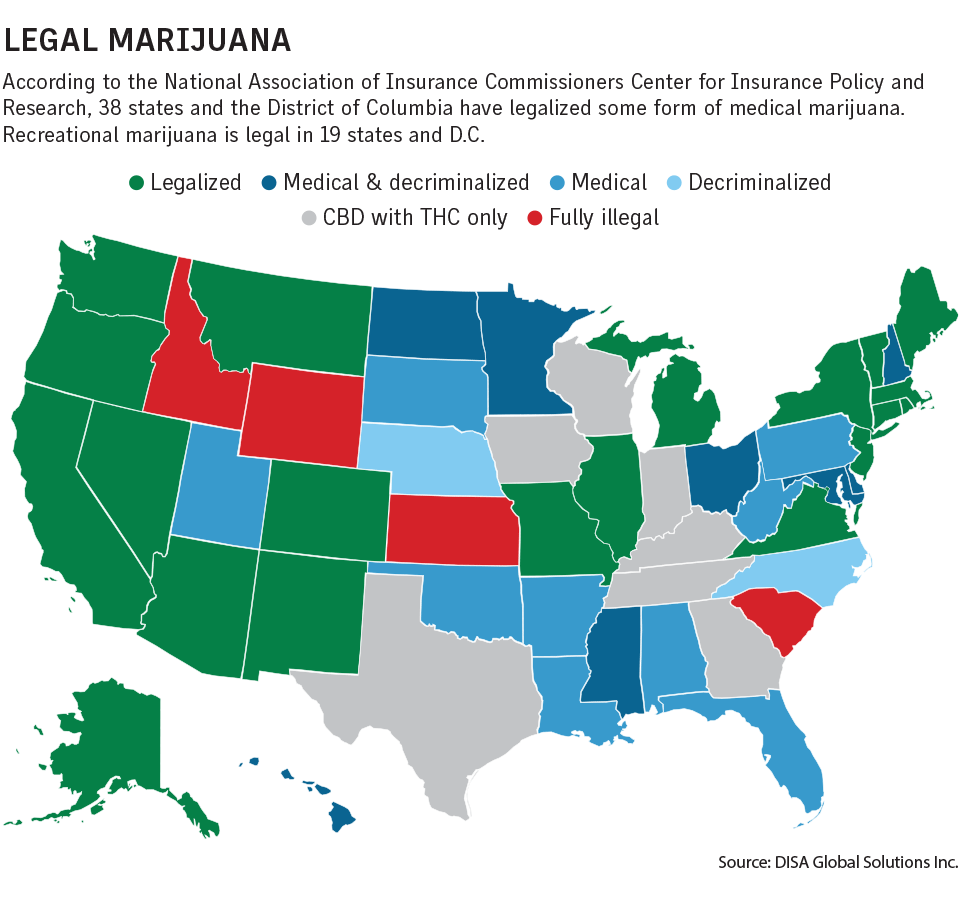

Since 1996, when California became the first state to permit medical marijuana, the medical use of cannabis has been legalized in 39 states and the District of Columbia. The recreational or adult-use of cannabis has been approved in 21 states and D.C.

Cannabis remained fully illegal in just four states — Idaho, Kansas, South Carolina and Wyoming — as of January, according to third-party administrator DISA Global Solutions.

“Our capacity for any product line usually doubles on a year-over-year basis to keep up with demand,” said Charles Pyfrom, Livermore, California-based chief marketing officer for managing general underwriter CannGen Insurance Services LLC.

Line sizes are increasing as well, he said. CannGen previously offered property limits up to $30 million, but in the past year has offered limits on some risks for close to $100 million per location, he said.

“It’s growing,” Mr. Pyfrom said, adding that buyers have become more sophisticated and risk focused.

The supply of insurance to the cannabis sector grows between 80% and 100% a year and the added capacity has increased competition and helped soften pricing, said Michael Hall, vice president of Golden Bear Insurance Co. in Stockton, California.

Rates for property and liability coverage have fallen as much as 50% from two years ago, when tight availability led to high pricing, he said.

The high pricing, in turn, attracted more insurers to the sector, leading to greater supply and ultimately lower prices and profit margins for insurers.

Product availability has also widened. Golden Bear launched its D&O program in January 2022.

“Two years ago, there were two markets writing directors and officers coverage for cannabis companies,” Mr. Hall said, adding that the number of D&O insurers in the cannabis sector has more than doubled.

CannGen in August 2021 launched its CannGenPro division, which offers management and professional liability insurance to the cannabis sector.

Embroker Inc. added cannabis insurance to its offerings because it is a “dynamic, entrepreneurial space” similar to the tech startups forming the core of its business, said Ben Jennings, chief revenue officer of the San Francisco-based online commercial broker.

Embroker targets single state dispensaries with less than $5 million in annual revenue for its digital offerings, which can be quoted and bound online, and serves larger, multistate operators through its brokerage operation, Mr. Jennings said. Coverage includes property, general liability, D&O, workers compensation and employment practices liability insurance.

Reinsurance capacity for cannabis risks has also expanded, though hurdles remain.

Mr. Hall estimates there are eight or nine reinsurers in the market, up from just one or two a few years ago. Interest in the sector is most keen among smaller reinsurers and the reinsurance market overall is slightly harder than the primary market for cannabis operators, he said.

Reinsurance growth is also limited by the conflict between state and federal laws.

“The macro view of reinsurance capacity is that the predominance of reinsurers will remain on the sideline until the federal government reclassifies cannabis, removes it entirely from the Controlled Substance Act, or legislation is enacted to establish a federal safe harbor for the insurance and reinsurance industry,” said Matthew Stanwood, Boston-based senior client executive at Lockton Re, the reinsurance brokerage unit of Lockton Cos. LLC.

Mr. Stanwood added that new reinsurance capacity is limited and “generally focused on supporting specific lines of business.”

Risk management is becoming more widespread in the cannabis sector, said Stephanie Bozzuto, a partner with Acrisure LLC and co-founder of Cannabis Connect Insurance Services, a unit of the brokerage.

“It is very common in property lines,” she said, with mandated features such as a safe, a vault, or cages that meet U.S. Drug Enforcement Administration standards for controlled substances, known as “DEA cages.”

“Many industries require protective safeguards to extend coverage,” she said.

Ms. Bozzuto, who joined Acrisure when it acquired Cannabis Connect in 2018, said limited insurance capacity is no longer the acute issue it was a couple of years ago, although there remain constraints in states such as Florida where catastrophe-exposed properties in all industries face hard market conditions.

Other sources noted the cannabis sector, like many other businesses, also faces restrictions and exclusions pertaining to wildfire in the Western United States.

Some areas specific to cannabis coverage remain difficult, said Jay Virdi, Toronto-based chief sales officer for specialty practices at Hub International Ltd., who is responsible for Hub’s cannabis specialty practice. For example, sublimits in crime policies for cannabis businesses can be as low as $5,000. “These limits are very low,” he said, especially amid increased crime exposures.

Ian Stewart, chair of the national cannabis and hemp law practice at Wilson Elser Moskowitz Edelman & Dicker LLP in Los Angeles, said crime coverage can present a challenge because almost all cannabis insurance is provided through bespoke policy forms, and the forms have different definitions of stocks and goods from a theft point of view.

“The crop, the harvested plant material, finished goods ready for sale — each has a different storage requirement,” and there is little consistency in policy language and definitions for each item, he said.

One growing challenge for the cannabis sector may come from an increase in product liability suits, with many centering on labeling, sources said.

“There is absolutely an increase in lawsuits that are premised on under or over reporting of cannabinoid content on labels, and associated claims of consumer fraud and false advertising around labeling and testing,” Mr. Stewart said.

For example, a suit filed in the Superior Court of California in Los Angeles against Ironworks Collective Inc. and Stiiizy LLC alleges violations of various consumer protection laws, misrepresentation and unjust enrichment.

While the number of lawsuits has been limited so far, cannabis operators should consider the product liability risk when evaluating their insurance needs, Mr. Pyfrom said. More widespread testing of products should become available as the industry grows, he added.