Costs, climate, inflation portend higher rates

Posted On: Oct. 5, 2022 12:00 AM CST

MONTE CARLO, Monaco — Reinsurance buyers will likely face rate hikes at Jan. 1, 2023, renewals as reinsurers say exposures are increasing due to rising costs and climate change and inflation is pushing claims higher.

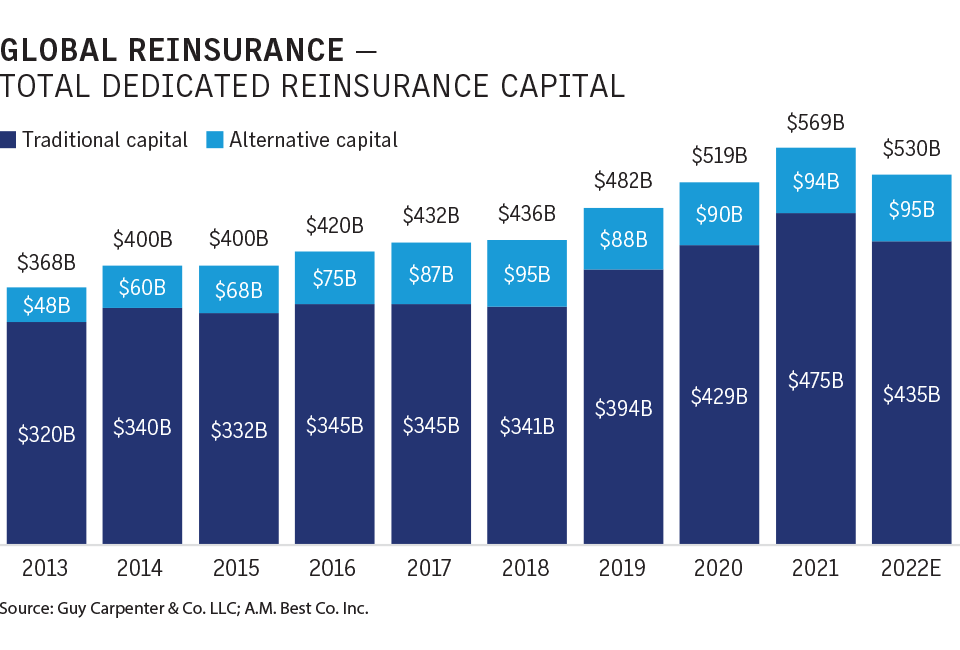

In addition, reinsurance capital is decreasing as higher interest rates attract investors to other investments and some reinsurers pull back, squeezing reinsurance capacity while demand is rising.

Gathering in Monte Carlo last month for the Rendez-Vous de Septembre, which traditionally marks the start of the year-end renewal season, reinsurers and reinsurance brokers said property reinsurance pricing is set to see significant increases, and casualty insurers will likely see lower ceding commissions as losses rise.

CLICK IMAGE TO ENLARGE

“We are definitely in a shifting, hardening market — no question,” Jill Beggs, Warren, New Jersey-based head of North American reinsurance at Everest Re Group Ltd., said at the meeting, which was held in person for the first time since the COVID-19 pandemic hit in early 2020.

Reinsurance rates were flat or included modest rises for many cedents at Jan. 1, 2022, renewals but increases at spring and mid-year renewals were often larger.

“Once we started having the inflation discussions post 1/1, that’s really when the market started hardening,” Ms. Beggs said.

“There’s a sense that there’s just not enough money in the system to be able to fund loss,” said Tim Gardner, New York-based global CEO of Lockton Re, a unit of Lockton Cos LLC.

While the Florida market differs from many other markets — in particular because of the way insurance claims rights can be assigned to a third party — the mid-year increases Florida cedents saw set a tone for the reinsurance market, he said.

“One of the things we very much felt was in June and July the momentum shifted in reinsurers’ favor,” Mr. Gardner said. “It started to have a knock on beyond just cat.”

As insurers assess the effect of inflation on insured values, they will likely seek to buy increased reinsurance limits totaling between $10 billion and $15 billion, said David Priebe, New York-based chairman of Guy Carpenter & Co. LLC.

“Against that backdrop, we haven’t yet seen equivalent capital step up to reenter the market to meet that increased demand,” he said.

Several reinsurers have pulled back property catastrophe capacity over the past year.

Pricing will likely increase as a result and be felt hardest in secondary peril coverages, such as wildfires and winter storms, where inflation has increased the size of the losses, so they are more likely to penetrate reinsurance programs, Mr. Priebe said.

Catastrophe rates

Premium increases for U.S. property catastrophe risks will be “very material” at year-end to reflect increased inflation and rises in exposure, said Jean-Jacques Henchoz, CEO of Hannover Re.

“After a few years of heightened activity, we need to see significant adjustments to the terms and conditions,”

Mr. Henchoz said.

Increased inflation will lead to economic volatility, said Torsten Jeworrek, chair of Munich Re’s reinsurance committee.

“The next renewal is much, much more challenging than last year’s where we had a much more economically stable environment,” he said.

Modeled loss costs, including materials, labor and other factors, have increased by 20% over the past 12 months for some property exposures in the United States, said Marcus Winter, president and CEO of Munich Re U.S. in Princeton, New Jersey.

“There have been price increases on the reinsurance side but not to the extent that is necessary, and that’s why we expect significant price corrections in the next 12 months,” he said.

Demand for reinsurance coverage in the U.S. is such that some cedents returned to the market for additional capacity after the June 1 and July 1 renewals were completed and Munich Re already agreed in early September to a Jan. 1, 2023, renewal contract with one of its cedents, Mr. Winter said.

Increased concentration of people in catastrophe-exposed areas, increased insurance penetration and increased wealth are the main drivers of higher reinsurance claims, said Thierry Léger, group chief underwriting officer at Swiss Re.

The effects of climate change will also drive up claims but not to the same degree as the other drivers, he said.

“Only 20% of the increase between now and 2040 will be due to climate change,” he said.

The reinsurance market is at a similar inflection point as the insurance market five years ago, when substantial, multiyear rate increases began, said Laurent Rousseau, CEO of SCOR.

Casualty

Casualty insurers will likely see lower ceding commissions on proportional treaties at year-end, experts say. Reinsurers pay ceding commissions to insurers to cover business acquisition costs and other expenses and then share in the profitability or loss on the book of business.

Ceding commissions on casualty reinsurance increased significantly at Jan. 1 renewals but have since moderated and will likely decrease further at year-end, as inflation and so-called social inflation, or higher judgments and settlements, drive up liability claims, Ms. Beggs of Everest said.

While ceding commissions vary by program, “it’s not uncommon” to see them in the low-to-mid 30% range, she said.

Underlying casualty insurance prices have increased over the past three years and reinsurers have been willing to pay high ceding commissions to access the portfolios, Mr. Gardner of Lockton said.

But as losses increase, some ceding commissions may decrease, he said.