Rising interest rates could boost insurers

Reprints

Commercial insurers could see higher investment income and changes in exposures because of recent and projected U.S. interest rate hikes aimed at curbing inflation.

Whether the monetary policies have the desired effect on the economy also remains to be seen as policymakers move forward with plans that appear directionally in sync but indicate some differences.

The U.S. Federal Reserve Bank’s Federal Open Market Committee on March 16 increased the target range for the federal funds rate by a quarter percentage point to 0.25% to 0.5% and said it “anticipates that ongoing increases in the target range will be appropriate,” with one committee member dissenting and supporting a half-point rise.

Roland Eisenhuth, economist and assistant vice president of policy, research and international in Chicago for the American Property Casualty Insurance Association, said higher interest rates will have a profound impact on the overall economy, “and this action could also impact the property/casualty insurance industry wherever it is linked to the broader economy.”

Potential increases in investment yields from higher interest rates could help offset any downward pressure on stock valuations, Mr. Eisenhuth said.

Higher interest rates, however, could also reduce demand, leading people to buy fewer cars or homes, which could slow the growth of exposures for property/casualty insurers.

Ludovic Subran, chief economist for Allianz SE in Munich, sees potential opportunity for insurers in the interest rate hikes.

The rising rates might present “good opportunity to reinvest portions of portfolios” at higher yields, he said.

“This is quite positive, as rate hikes mean profitability will increase on the asset side because we are mostly invested in bonds,” Mr. Subran said of commercial insurers.

Raising interest rates to curb inflation also benefits insurers chafing under claims inflation, driven by elements such as higher building material costs, he said. The property/casualty industry will “welcome” the rate hikes to help curb claims inflation, he said.

The Allianz “base scenario” includes six rate hikes this year, the first of which has taken place, and three next year, Mr. Subran said.

Swiss Reinsurance Co. Ltd. in April raised its Fed Funds forecast to six rate hikes this year from four, for a total of 200 basis points, implying potential 50 basis-point hikes at some of the Fed’s meetings. In addition, Swiss Re expects the Bank of England to hike rates five times rather than four and for the European Central Bank “to likely exit from negative interest rates by the year end.”

“Inflation rising further from already high levels will likely see major central banks raising interest rates faster and more forcefully,” the reinsurer said in revising its forecast.

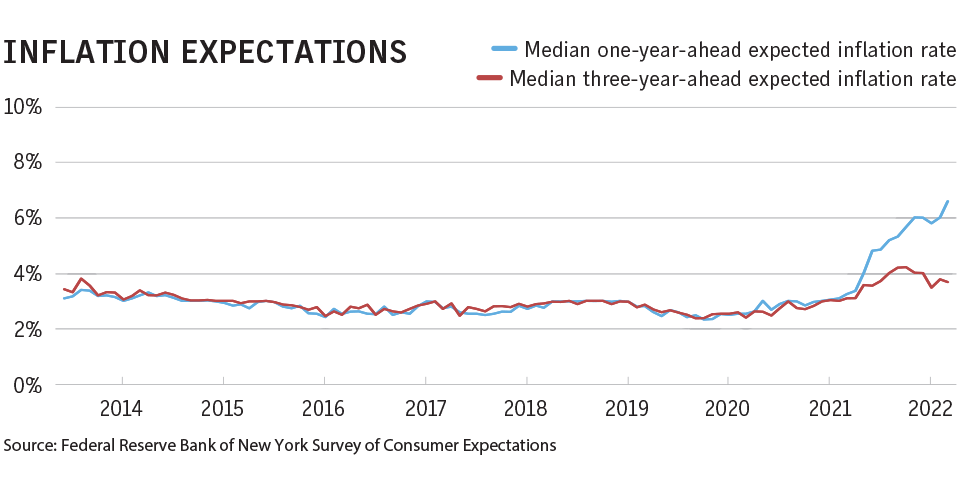

Michel Léonard, chief economist for the Insurance Information Institute in New York, said the Fed is looking to end the year at about 4.3% inflation, down from current levels nearer to 8%. “We have a very clear direction. We know inflation will come down and growth will come down. That’s very clear and useful,” he said.

Indicators such as the futures markets for shipping containers show slowing demand, Mr. Léonard said. Trading in these futures markets “gives us a sense of where it’s going to be and there is light at the end of the tunnel when looking at futures for container rates, and the worst is behind us.”

Although the III sees the U.S inflation rate reaching Fed targets, Mr. Léonard said it may take into the first or second quarter of next year rather than by year’s end. “Our view is Fed numbers are feasible, but quite fast and steep. The question is how fast this happens.”

Federal Reserve Bank of New York President John C. Williams, who also serves as the vice chairman and a permanent member of the Federal Open Market Committee, said in recent public comments that faced with rising inflation but otherwise strong economies, the Fed and other central banks have been moving away from the “extraordinarily accommodative” stances they took in early 2020. The Bank of England began raising rates in December, followed by the Bank of Canada in March.

Other Federal Reserve officials have advocated a range of policy alternatives differing slightly along the way. On March 18, two days after the Fed’s initial quarter-point hike, Federal Reserve Bank of St. Louis President Jim Bullard issued a statement explaining his dissenting vote in which he called for a half-point hike.

“In my view, raising the target range to 0.5% to 0.75% and implementing a plan for reducing the size of the Fed’s balance sheet would have been more appropriate actions,” the statement said.

Supply chain shortages, strong demand drive current inflation

While raising interest rates has long been used as the remedy for rising inflation, some experts warn that policymakers must tread carefully.

The causes of today’s inflation are not the same as those from the past, they say.

“The inflation we have now is different. It’s not driven by the same drivers,” like oil prices in the 1970s, said Michel Léonard, chief economist for the Insurance Information Institute in New York.

Today, U.S. inflation is driven by supply chain shortages and very strong demand in some sectors, such as pre-owned autos. “It’s an inflation driven by an economy that’s recovering and that’s doing well,” Mr. Léonard said. “Will increasing interest rates have the desired impact on the scale desired?”

For instance, “what’s raising interest rates going to do to supply chain delays? Not much,” he said.

“If we believe that tightening monetary policy could solve the supply chain crisis in China, this is, of course, wrong,” said Ludovic Subran, chief economist for Allianz SE in Munich. He also sees some strength in the U.S economy, partially because of the stimulus payments during the COVID-19 pandemic.

The Federal Reserve’s desire to “come out big” and control the political narrative of the situation, must also be carefully managed, Mr. Subran said. Taking too heavy a hand could risk recessionary conditions.

“The Fed as the lender of last resort for the U.S. and the world” has increased its prominence and makes crafting monetary policy more complicated, he said.