Rising material prices, catastrophe losses put focus on multifamily property claims

Reprints

Commercial residential properties, already facing a tough insurance market, are seeing double-digit rate increases and even higher for loss-hit risks in catastrophe-exposed locations.

Recent losses, such as the partial collapse of the Champlain Towers South condominium building in Surfside, Florida, in June 2021, have heightened market concerns about underinsured properties, experts say.

The winter storm and freeze that hit Texas and large swaths of the U.S. early last year also led to a substantial volume of claims for insurers in the multifamily sector.

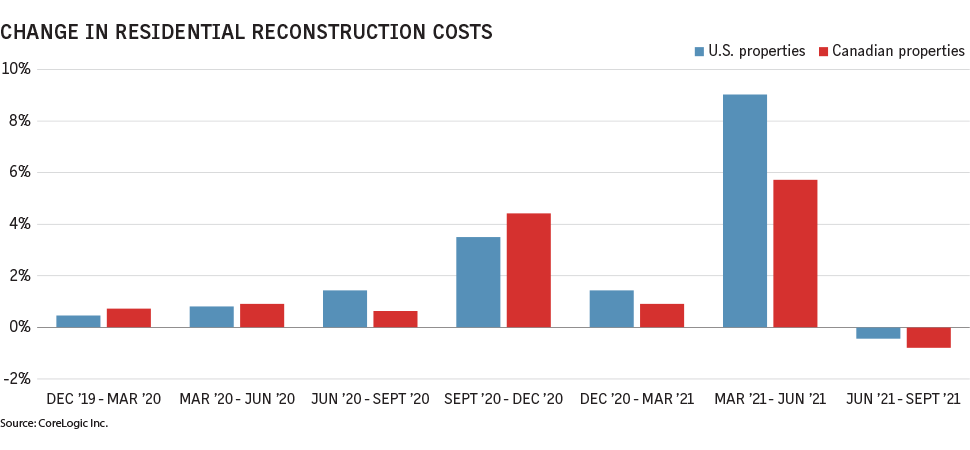

Inflation, which accelerated to 7.5% in January, is driving up costs for insurers, widening the gap between insured values and actual rebuilding costs.

“We are in an inflationary economy,” said Maggie McIntyre, area executive vice president with Arthur J. Gallagher & Co.’s global real estate and hospitality practice in Whippany, New Jersey.

“Insurers having sustained catastrophic losses are looking at those losses versus what insureds reported on schedules, and in some instances there’s a disconnect,” she said.

At renewal, policyholders should ensure that replacement cost values are reported accurately. “Most conversations start off with ‘let’s look at the values,’” Ms. McIntyre said.

Every policyholder should expect pressure to review property values going forward, said Rick Miller, Boston-based U.S. property practice leader at Aon PLC’s commercial risk solutions business.

Construction costs have increased significantly, and the pandemic has exacerbated the problem, with supply chain challenges and rising prices for building materials such as lumber, copper and roofing, Mr. Miller said.

The higher prices of materials are driving up replacement costs, said Vivalde Couto, executive vice president of underwriting at American European Insurance Group, a unit of American European Group Inc. in Cherry Hill, New Jersey. “The rates are up, but in addition to rates going up, we also have more of a need to increase the building limit so that the insured continues to have replacement cost coverage,” he said.

Every insurer is asking policyholders about how they are valuing their properties, said Marc Reisner, Boston-based multifamily practice leader at Marsh LLC. In addition to inflation, insurers are responding to loss experience and “how much they are paying out in claims that had been above what clients are estimating their replacement values to be,” Mr. Reisner said.

Impact of losses

Winter storm Uri, which struck hardest in Texas but also hit states from Florida to the Northeast, and the Surfside condo collapse both highlighted the importance of valuing properties appropriately, brokers say.

The Texas freeze resulted in a significant volume and severity of claims in a part of the country that historically was unused to plunging temperatures, said David Novak, San Francisco-based area president in the property practice at Risk Placement Services Inc., the excess and surplus lines broker and managing general agent unit of Gallagher.

“We’ve got accounts that had $20 million to $30 million in Texas freeze claims on their portfolio of habitational business that was neither accounted for, nor expected or placed for,” he said.

Insurers are pushing for more information on values, he said. “The tough part for insureds is not only are they seeing rate increases because the cost of capital has gone up, so their cat exposure has gone up year over year, but now they are also getting dinged with an increase in insurance to value,” he said.

In its 2022 Property Market Outlook released in February, RPS cited the Surfside condo collapse as a cautionary example of what can happen when a structure isn’t insured to its current valuation.

The condominium association had purchased a $31.4 million property policy for a building where 136 condo unit values ranged from approximately $400,000 to nearly $3 million, RPS said.

On Feb. 11, a tentative settlement was announced by attorneys that would split $83 million among those condo owners who lost property in the collapse that left 98 dead. Those who agree to the settlement would be released from possible liability claims under a Florida law that makes unit owners liable for acts by their condo association board.

Losses such as Surfside had a ripple effect across the marketplace, both in terms of rates and valuations, said Brendan O’Connor, vice president of operations at ReShield LLC, part of Baldwin Risk Partners LLC, in New York.

Insurers are more frequently conducting onsite inspections to take a hard look at what they’re insuring, Mr. O’Connor said. “Insurers want to make sure they are collecting appropriate premiums,” he said.

They are also thorough in the questions they ask property owners about their risk mitigation tactics and loss control.

CLICK IMAGE TO ENLARGE

In some cases, habitational risks are “terribly undervalued,” said Peter Fallon, national property practice leader at brokerage Risk Strategies Co. Inc. in Boston.

“I’ve seen some that are $50 per square foot, some that are $80 per square foot. Now, underwriters are saying unless you can get it to $100 per square foot then we may not quote, or, if we quote, we may eliminate a blanket (limit) … and therefore the limit would apply per location,” Mr. Fallon said.

Other restrictions insurers may impose include co-insurance provisions and occurrence limit of liability endorsements, “so you will pay bounty either in the absolute limit or as a percentage of it,” Marsh’s Mr. Reisner said.

Insurance-to-value concerns have always been an issue, said David Pagoumian, president of the Red Bank, New Jersey, office and property practice member at CRC Group, a unit of CRC Insurance Services Inc.

“The reinforcer for today is you’re not going to be able to convince an underwriter to accept unreasonable valuations unless you want restrictive coverage,” Mr. Pagoumian said.

Valuations become central topic of renewal discussions

Property insurance buyers, including owners of multifamily buildings, should work with brokers and insurers to get ahead of any concerns over valuations, experts say.

Brokers going into a renewal cycle should make sure they are having a conversation with their clients around their values, said Peter Fallon, national property practice leader at brokerage Risk Strategies Co. Inc. in Boston.

Understanding what the valuation is based on and asking if there is an appraisal is important, Mr. Fallon said.

“We can do a cost-per-square-foot calculation for buildings to come up with what we think the value should be and compare that to the statement of values, but it’s up to the client to tell us whether the machinery and equipment values are accurate because we can’t do a desk job on that,” he said.

Rick Miller, Boston-based U.S. property practice leader at Aon PLC’s commercial risk solutions business, said it should be easier for insurers to understand valuations on a multifamily habitational risk than for a complex manufacturing risk.

With a multifamily property, “you know what it is built from, so it’s fairly easy to understand what the property damage values should be,” Mr. Miller said. The time element component of real estate risks should also be straightforward since rental value exposures are based on the number of units and the amount of rent collected, he said.

For a manufacturing risk where complex, sophisticated machinery is in use, it could be more challenging, he said.

In some cases, insurers will ask clients to substantiate their statement of values, and sometimes they will do their own valuation to come to a value they are comfortable with and quote accordingly, said Maggie McIntyre, area executive vice president with Arthur J. Gallagher & Co.’s global real estate and hospitality practice in Whippany, New Jersey.

Valuations of older buildings, because of the way building materials were used and the data available, present a different challenge than newer buildings, but the focus on valuation is across the board, she said.

In the case of a significant loss, older buildings may need code upgrades, such as sprinkler and electrical systems that comply with local ordinances, said Vivalde Couto, executive vice president of underwriting at American European Insurance Group, a unit of American European Group Inc. in Cherry Hill, New Jersey.

The upgrades can increase rebuilding costs, Mr. Couto said.

Adding ordinance or law coverage to a commercial property policy is an important consideration for policyholders, and some commercial lenders require the coverage, brokers said. However, insurers may have limited capacity for the risk, they said.

Little relief on rates expected for buyers as insurers exit market

Insurance market conditions are expected to remain challenging for multifamily risks in the year ahead, especially for wood frame construction.

In addition to rising catastrophe losses, multifamily properties are susceptible to water damage and fire claims.

Premium rate increases will be in the 15% to 20% range for many, with hurricane-exposed properties seeing rate increases that are even higher, Risk Placement Services Inc. said in its 2022 Property Market Outlook released in February.

Many insurers are raising wind and hail percentage deductibles on properties in the Midwest, RPS said.

“This industry segment has gotten crushed over the last four to five years from both catastrophe losses and attritional losses,” and many insurers have exited the market, said David Novak, San Francisco-based area president in the property practice at RPS, the excess and surplus lines broker and managing general agent unit of Arthur J. Gallagher & Co.

“Five years ago, there were maybe seven to 10 markets; now there are just three to four markets writing the class,” Mr. Novak said. As a result, there is a supply and demand imbalance, which drives up prices, he said.

The overarching theme of renewals is underwriting discipline, said David Pagoumian, president of the Red Bank, New Jersey, office and property practice member at CRC Group, a unit of CRC Insurance Services Inc.

He cited the recent renewal of a high-rise tower in Manhattan. Part of the residential property houses a hotel, now unoccupied, and its expiring insurer declined to renew the risk. It took at least six insurers to produce a quota share on the account, and the premium tripled, Mr. Pagoumian said. Still, he described this as “an outlier.”

Many multifamily habitational properties tend to be lighter construction such as frame which is a “bad combination” when mixed with the human component associated with water damage and fires, said Rick Miller, Boston-based U.S. property practice leader at Aon PLC’s commercial risk solutions business.

Renewals are expected to continue to be “reasonably challenging” going forward for accounts that have experienced losses, but for accounts that have done a good job managing risk that have higher retentions, renewals are expected to go well, Mr. Miller said.