M&A cover costs rise with losses

Reprints

A resurgence in mergers and acquisitions activity coming out of the pandemic has fueled a record volume of deals and unprecedented demand for representations and warranties insurance, industry experts say.

As the coverage has become more widely used and the pace of deals has accelerated, more claims are being filed, and as insurer payouts grow, the price of a reps and warranties policy has increased.

Deals are also facing more scrutiny because insurers are being more selective in the risks they write in response to the overwhelming level of submissions, experts say.

Rates are hardening due to the claims environment and the “steep increase” in the number of transactions seeking insurance, said Allyson Coyne, Philadelphia-based managing director and chief broking and administrative officer of M&A and transaction solutions at Aon PLC.

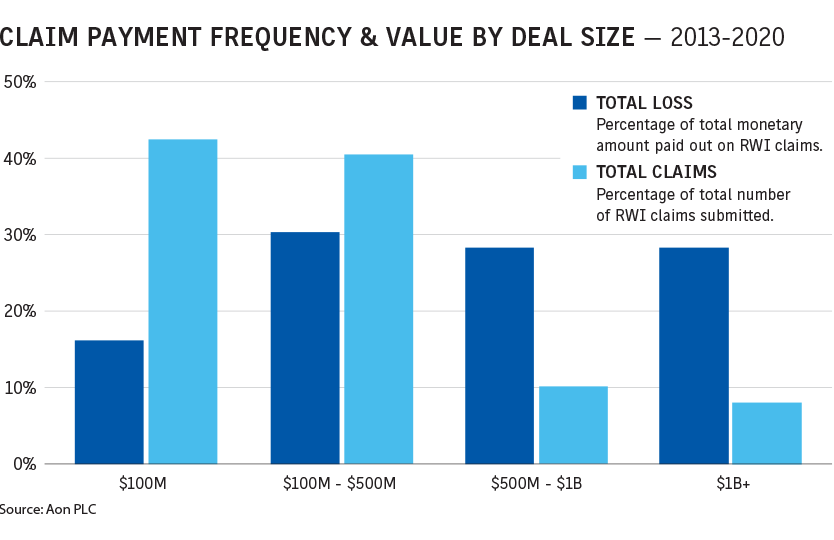

CLICK IMAGE TO ENLARGE

Rate increases started in 2020 and have trickled into 2021, with the average rate on line for primary reps and warranties deals increasing “about three-tenths of a percent over the average at the same time in 2020,” Ms. Coyne said.

Some deals may be more challenged than others. “Small deals, health care deals are very challenging to get placed when there’s so much volume in the market right now,” she said.

“A rising M&A tide is raising all insurance boats,” said Rowan Bamford, London-based president of Liberty Global Transaction Solutions, a unit of U.S. insurer Liberty Mutual Insurance Co.

Insurance is seen as an increasingly important deal tool. “We are insuring a higher percentage of the deals that are done, and on top of that more deals are being done,” Mr. Bamford said.

Rates in the Americas have increased up to 25% since the third quarter of 2020, driven in part by increased claims activity, Liberty Mutual said in a September report. The region sees a higher proportion of “high” and “medium” severity claims and more claims for the full tower limit, the report said.

Rates on larger transactions have seen a “significant uptick,” said Stavan Desai, New York-based senior vice president, M&A team leader at Mosaic Insurance Holdings Ltd.

The bigger a transaction is, the more insurance markets generally are involved to provide an adequate level of insurance coverage, and typically the primary market will charge an increased rate given it is taking the most amount of risk, Mr. Desai said.

“For a $3 billion deal where you’re maybe getting $300 million of insurance coverage, that primary market was offering a $25 million limit and maybe pricing that at a 5% rate on line a few years ago,” he said. “Now, we’re seeing rates at 6.5%, 7.5%. ... We had a tower that was priced at 8.6% fairly recently,” he said.

The market has been on a run, and insurers are trying to keep up with the demand for additional manpower and availability and putting more limits out into the market, said Larry Shapiro, San Francisco-based managing director and representations and warranties insurance team leader at Alliant Insurance Services Inc.

“Some took the opportunity to correct that rate to a level that they felt better reflects the risk exposures that are being covered,” while others have used the pricing as “a proxy to handle deal flow,” Mr. Shapiro said.

The latter trend has spilled over into more substantive aspects of coverage, he said. Insurers are managing capacity by taking the deals they feel they can execute on most efficiently or “they are quoting harder deals but on terms that have more substantive limitations than they may have in the past,” he said.

Insurers are more likely to modify the reps and warranties in agreements for purposes of coverage than they have in the past, said Michael Wakefield, executive vice president and transactional insurance practice leader at CAC Specialty, who is based remotely in Tennessee. “I’ve seen more markups of a purchase agreement for policy purposes,” he said.

Insurers are also inserting more restrictive limitations around data privacy and cybersecurity, and in some cases environmental and product liability issues, he said (see related story, below).

Now that reps and warranties insurance is a default source for coverage in a transaction, insurers have their pick of deals and they don’t have to be as accommodating any more, said Randi Mason, co-head of the corporate practice at law firm Morrison Cohen LLP in New York.

“Where I’m seeing the most change is insurers are kicking the tires on due diligence that buyers are doing much more deeply than before,” Ms. Mason said.

Cyber, data focus of insurer scrutiny of deals

Insurers are paying more attention to the scope of what is covered in a reps and warranties policy and inserting more restrictions, especially around cyber and data privacy exposures, experts say.

Data privacy and cybersecurity comprise an area where insurers might point to other insurance coverage as primary sources of recovery for the client, said Michael Wakefield, executive vice president and transactional insurance practice leader at CAC Specialty, who is based remotely in Tennessee.

“In the past, it was more likely not to have specific exclusions in respect to those matters. We see insurers draw harder lines on it now,” Mr. Wakefield said.

Increased insurer scrutiny on M&A deals is making negotiations more complex, said Randi Mason, co-head of the corporate practice at law firm Morrison Cohen LLP in New York.

In a recent deal, the insurer sent the middle-market buyer six pages of questions and proposed exclusions covering topics such as corporate, tax, insurance, benefits, intellectual property/cyber, real estate and financial matters, Ms. Mason said. “Ultimately, there were over 15 to 20 deal-specific exclusions in the policy, in addition to exclusions for known breaches,” she said.

Standard coverage exclusions — which include covenants breaches, forward-looking statements and purchase price adjustments — have remained “pretty consistent” even with the changes in the market, said Paige Brewin, underwriting leader, transactional liability, at QBE North America.

“A trend we’re seeing with the hardening market is that there’s more of a need to negotiate terms early on, even at the quoting stage, before the underwriter has been engaged,” Ms. Brewin said.