Severe weather prompts policy revisions

Posted On: Sep. 1, 2021 12:00 AM CST

Climate-driven events are prompting changes in commercial property insurance policy wordings and tighter terms and conditions as insurers try to manage the increasing frequency and severity of natural catastrophe losses, brokers say.

How policies define temperature change and how deductibles and limits are applied are some of the areas where policyholders are seeing an impact, they say.

Global insured natural catastrophe losses totaled $40 billion in the first half of 2021, driven by winter freeze, hailstorm, flood and wildfire losses, according to a report published last month by Swiss Re Institute, part of Swiss Re Ltd.

Winter storm Uri, which hit swaths of the United States in February, caused estimated insured losses of $15 billion, the highest ever recorded for this peril in the U.S., and accounted for about 38% of all estimated insured losses from natural catastrophes in the first half, Swiss Re said.

Weather-related events — not just one-off events — are becoming more frequent and severe, and there’s a push by insurers to continue to clarify and enforce language, said Martha Bane, Glendale, California-based managing director of the North America property practice at Arthur J. Gallagher & Co.

For hail/convective storm losses, in the past two to three years insurers have pushed actual cash value on building roofs, Ms. Bane said. “That means a much lower claim payout for the insured,” she said. Insurers have also introduced “very scientific ways” of detecting pre-existing damage, she said.

Deductibles in commercial property policies have changed significantly. It’s almost standard in hail-prone areas for policies now to have a percent deductible for the exposure “whereas in the past the standard all other perils deductible applied,” she said.

In the wake of winter storm Uri, which knocked out power for numerous people and companies in Texas, change in temperature language has also been added to policies to clarify what coverage insurers intend to provide, Ms. Bane said.

Change of temperature coverage, which covers loss of products or materials that are sensitive to changes in temperature is offered by some insurers.

Insurers are moving to refine and restrict coverage following the freeze event in February, said Brian Dove, USI Insurance Services LLC’s national real estate practice leader, based in Dallas.

“There are going to be some changes in policy language as it relates to that type of event, because the application of some of the carrier forms is not what clients expected, so there were some shortfalls there,” Mr. Dove said.

One of the questions is around the term “change in temperature,” he said. “We haven’t seen the final version of where we’ll land but there will be changes in the policy language as it relates to that type of event,” he said.

Deductibles for earthquake, flood, named storm and wind/hail have also changed, increasing retentions for policyholders, Mr. Dove said. And insurers have reduced capacity for wildfire risks, he said.

FM Global is not planning any broad, wholesale changes to its policies when it comes to weather-related risks or climate change, said Amy Brown, staff vice president, manager for natural hazard underwriting, at the Johnston, Rhode Island-based insurer.

“There is nothing specific in our policy that addresses climate change,” and no temperature wording for freeze, Ms. Brown said.

However, policies are tailored to the individual risk profile of policyholders, and as the nature of their risk profile changes, “we have updated the policy to keep pace with that,” she said.

Five years ago, FM Global talked to policyholders about moving toward percentage deductibles for hail. “That was to help manage that balance between cost of insurance and the coverage they are looking for,” she said.

Joseph Jonas, product manager, commercial lines, at the American Association of Insurance Services, an insurance statistics and advisory organization in Lisle, Illinois, said there is not necessarily a shift by insurers to standardize language as it relates to extreme weather events and climate change.

But recent events have led to a shift in how the industry approaches extreme weather events, whether that’s insurers developing new coverages, the way insurance departments look at new filings, catastrophe modeling or adjudication of claims, he said.

Superstorm Sandy in 2012 brought to light inadequacies in policy language and/or policy offerings, for example, Mr. Jonas said.

Insurers are requesting much more information from catastrophe modelers with respect to climate change, in part because external stakeholders, such as regulators and rating agencies, are seeking more information from insurers, said Karen Clark, president and CEO of Karen Clark & Co.

“Insurers want to make sure the cat models are accounting for climate change to the extent possible,” she said.

Wildfire is the modeled peril that has the highest percentage impact from climate change, followed by floods and hurricanes, and then severe convective storms, Ms. Clark said.

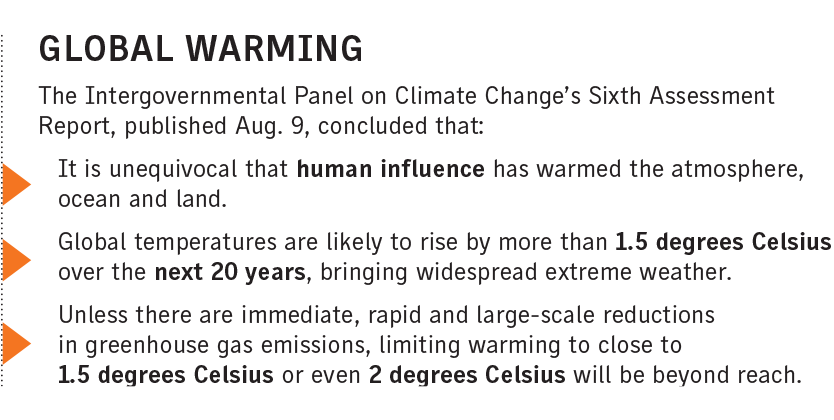

Scientific evidence suggests that climate change is a driver for many perils and the aggregate catastrophe data and first-half statistics confirm that, said Thomas Holzheu, chief economist for the Americas at Swiss Re Institute.

Mitigation strategies vital in managing climate-related losses

Mitigation has a critical role to play as insurers and policyholders look to better manage climate-driven losses, experts say.

Businesses can take steps at individual locations to mitigate their exposures to perils, said Brian Dove, USI Insurance Services LLC’s national real estate practice leader, based in Dallas. “It doesn’t guarantee they won’t be impacted by the event, but it definitely helps to mitigate the impact,” he said.

For more traditional primary perils such as flood, wind and earthquake, there’s extensive scientific data that “helps us understand the nature of the event,” what factors might make a client high risk, and “a wealth of ways to mitigate that,” said Amy Brown, staff vice president, manager for natural hazard underwriting, at FM Global, the Johnston, Rhode Island-based insurer.

“When we look at some of the emerging perils, like hail and wildfire, we’re in the beginning of that journey,” she said.

Catastrophe models can be used to determine the value of mitigation strategies, said Karen Clark, president and CEO of Karen Clark & Co. in Boston. “When commercial property owners do things to mitigate the risk, the models can quantify how much the rates can change due to that,” she said.

Insurance regulators also want to be sure mitigation steps taken by property owners and communities, such as pruning and clearing brush, are incorporated into the models and reflected in the rates charged, she said.