SPACs face challenges buying D&O cover: Can captives provide right solution?

Posted On: May. 4, 2021 12:00 AM CST

Captive insurers, long a home for hard-to-place risks and seeing greater use in the hardening commercial insurance market, are being eyed as a potential solution for the directors and officers liability problems facing special purpose acquisition companies.

A rapid rise in the volume of SPAC deals has led to a surge in demand for D&O insurance. Recent regulatory scrutiny of SPACs has compounded insurer wariness of these risks. As a result, D&O coverage costs, which were already climbing, have accelerated, leaving the so-called blank check companies exploring alternatives.

But trying to cover SPAC initial public offering D&O risks through captives could be problematic, experts say.

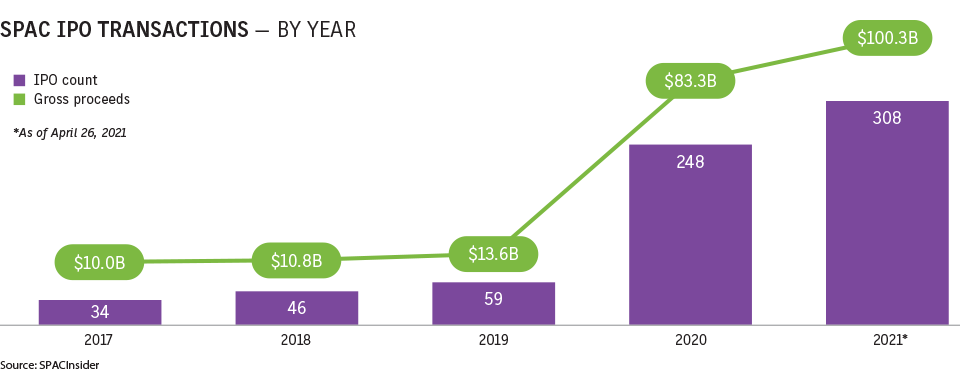

CLICK IMAGE TO ENLARGE

Captives have been used in D&O programs outside of the SPAC realm, but there are “potential headwinds” for SPACs in using them, said Kristin Kraeger, national SPAC and IPO leader at Aon PLC in Boston.

SPACs have a finite existence (see box), whereas captives are “longer-term plays and not really a solution you can pivot to midterm in your negotiations,” Ms. Kraeger said.

Captives are more frequently being discussed as potential vehicles to solve the riddle of maintaining broad coverage, accessing sufficient limits and controlling costs in a hard or hardening market, said Machua Millett, Boston-based SPAC leader at Marsh LLC.

However, the major hurdle for SPACs considering captives is timing. “The typical lifecycle for the SPAC and deSPAC process is only about two years at most, and sometimes as short as six months from the SPAC IPO to the close of the reverse merger. Captives take some time to arrange and set up,” Mr. Millett said.

There’s a “fundamental mismatch” between the timeline of a captive and the timeline of a SPAC, said Priya Cherian Huskins, San Francisco-based partner and senior vice president at broker Woodruff Sawyer & Co.

CLICK IMAGE TO ENLARGE

“A SPAC typically will decide to form and need its insurance within a very short period of time whereas a captive is designed to be economically efficient for a company that has operating profits and will be in business for many years,” she said.

Funding is another factor that makes a SPAC ill-suited for a captive, Ms. Huskins said. “A SPAC by its nature has a limited amount of working capital and then goes into the capital markets and raises a lot of money, but all of that money is held in trust. It’s not available for other activities,” she said.

Captive conundrum

The Delaware Insurance Department is beginning to receive inquiries about forming captive insurers for SPAC D&O risks, said Steve Kinion, the state’s captive insurance director.

“It becomes a question of whether there’s enough capacity in the D&O market right now to provide coverage for all these SPACs. If there isn’t, then at some point they will need to find coverage somewhere, because like all other companies SPACS want highly qualified directors and officers,” he said.

D&O coverage is critical for SPACs to attract and retain qualified directors and officers because the pace at which they target acquisitions and complete deals exposes them to shareholder scrutiny and potential lawsuits.

In Delaware, single-parent captives, captive cells and series captive insurers provide D&O coverage, Mr. Kinion said.

While captives typically provide years of coverage, captives have been formed to insure joint ventures between two companies where the captive’s existence is less than five years, he said.

Many large companies, including operating companies being acquired by a SPAC, may already have a captive, so “the use of that single-parent captive or establishment of a new one would be the most common” approach, said Jeff Kurz, managing director, captive insurance sales and consulting, North America, at Artex Risk Solutions Inc., the captive management unit of Arthur J. Gallagher & Co., in Columbus, Ohio.

However, if a company is looking to cover just its D&O retained risk, then a protected cell captive may be a more cost-effective and less capital-intensive option, he said.

Given a SPAC’s limited purpose and existence, a protected cell captive or a group captive is likely a more viable option than a single-parent captive structure, said Jeffrey S. Raskin, San Francisco-based partner at Morgan Lewis & Bockius LLP.

Cell captives, where companies essentially rent the use of a cell within a larger captive, could be a better fit for the accelerated lifecycle of a SPAC because they are “already an existing entity that is used for a fee,” he said.

A group captive, in which entities with similar risks come together and jointly own a captive, might also work better than a single-parent captive because it’s quicker and easier to access, Mr. Raskin said.

Regardless of which captive funding option is selected, using a proper actuarial study, implementing claims procedures, and following insurance accounting practices are critical to demonstrate that the captive should be treated as an insurance company, Morgan Lewis said in a March brief on SPACs and captives.

The Side A problem

In the hard commercial insurance market companies in general, in addition to SPACs, are exploring alternatives for Side A D&O coverage, including captives.

While some Side B and Side C D&O exposures are covered by captives, Side A coverage is more problematic. Side A coverage provides indemnification for directors, officers and employees for claims when a company cannot provide indemnification. Sides B and C cover corporate exposures.

Business corporate laws may prohibit or place into question whether a captive insurer can provide Side A coverage, Mr. Kinion said.

“The conflict arises because a captive is owned by the company, the insured. Should the captive be providing coverage for a claim when the corporation itself — the company that owns the captive — cannot indemnify the officer or director? That’s the issue,” he said.

It’s possible that the use of a protected cell company could be regarded as more distanced from the company itself and therefore a better fit to fund a nonindemnifiable loss, several experts said.

Other options

In addition to captives, various alternatives, such as buying Side A-only coverage, a 12-month versus a 24-month policy term and different ways to structure premium payments, are being considered by SPACs, said Ms. Kraeger of Aon.

Side A-only policies tend to be about 20-25% cheaper than an ABC policy, Marsh’s Mr. Millett said.

Some SPACs are comfortable purchasing Side A-only coverage, said Jonathan Selby, general manager at Foundershield LLC, a brokerage in New York.

Others, such as those wanting higher limits, perhaps up to $10 million or even higher, are buying $5 million of ABC coverage, and “instead of building on top of that with full ABC, they will purchase Side A for another $5 million excess of their underlying ABC coverage,” Mr. Selby said. “There are some cost savings to be had by going that route.”

In the high-cost environment, some buyers have chosen to purchase Side A coverage only, said Kevin LaCroix, executive vice president in Beachwood, Ohio, for RT ProExec, a division of R-T Specialty LLC.

“How that will respond in the event of a claim is a question they need to work with their legal and insurance advisers on,” he said.

The working capital of a SPAC is limited, and SPAC directors and officers don’t have access to the trust money to pay their legal fees should an enforcement action begin, Woodruff Sawyer’s Ms. Huskins said.

That makes the prospect of sitting on the board of a SPAC with little insurance unappealing. “My advice to people who are thinking about insurance for a SPAC is to … understand what an appropriate budget in the current market is, which is dynamic,” Ms. Huskins said.