Buoyant insurance M&A market rolls on amid abundant capital, hardening rates

Reprints

Mergers and acquisitions activity in the insurance sector was strong in 2020 despite COVID-19 and is expected to remain robust in 2021 as rising commercial insurance rates bolster earnings, making insurers attractive targets, and “deployable capital” remains abundant, analysts and others say.

Insurance technology investments have also grown, providing another avenue to enter the sector. In addition, special purpose acquisition companies, the use of which has boomed in many sectors over the past year, are being used in the insurance sector as a means of potentially taking companies public.

Another indication of this year’s strong M&A market is Chubb Ltd.’s offer in late March to buy rival Hartford Financial Services Inc.

“The mergers and acquisitions market in general, not just insurance, has been off the charts from last June through today, and we aren’t seeing anything right now that says that will slow down anytime soon,” said Mark Purowitz, senior partner in the mergers and acquisitions practice of Deloitte Consulting LLP in New York.

Some in the insurance industry were “surprised at how much deal activity there ended up being last year,” despite the interruption to markets in the spring due to the coronavirus pandemic, said Vikram Sidhu, New York-based partner at law firm Clyde & Co.

Deal advisors expected COVID-19 to chill activity, but 2020 proved to be a busy M&A year for the sector globally, he said.

Similarly, deal activity in the broker sector paused only briefly, said John Marra, a deals partner with PricewaterhouseCoopers LLP in New York.

“The distribution space continues to be very attractive,” he said. Broker M&A “saw a bit of a pause in the second quarter last year as those businesses were focusing on themselves and how to adapt to working from home” and other manifestations of the pandemic.

Some deals that were put on hold due to pandemic-related issues will likely be completed in the first half of this year, Mr. Purowitz said.

The total of 407 mergers and acquisitions completed worldwide in the insurance sector in 2020 was down slightly from 419 the previous year, according to a late February report from Clyde & Co. The number of deals completed in the second half of 2020 was slightly higher than the first half, with 206 deals compared with 201.

Although “deal activity in the insurance sector slowed in the spring of 2020,” it came “roaring back in the second half of the year,” PwC said in a late January deals report. “We expect strong M&A activity to continue as we head into 2021,” buoyed by “the hardening of specialty (property/casualty) markets and significant levels of deployable capital.”

As the insurance industry sees increased rates, buyers in search of returns in a low interest rate environment may be more attracted to the sector, said J. Paul Newsome Jr., Chicago-based managing director at investment brokerage Piper Sandler Cos.

The low interest rate environment also contributes to the availability of capital, which, combined with the search for returns, helps drive M&A activity, he said.

On the other hand, rising rates and premiums could blunt M&A activity as insurers focus on organic growth as opposed to growth via acquisition, said Meyer Shields, Baltimore-based managing director at Keefe, Bruyette & Woods Inc.

“There are enough opportunities for growth that companies are not looking for more complicated growth available through acquisition,” which carries integration and reserve risks, he said.

Technology investing also continues to grow in the insurance sector.

Investors are “very solidly coming in” to the insurtech space, said Mr. Sidhu of Clyde & Co. The sector has seen significant investment over the past five to seven years, he said.

Major investment activity in the insurtech sector last year included Aon PLC’s purchase of Coverwallet Inc. for an undisclosed sum and Duck Creek Technologies Inc.’s successful initial public offering, which raised $405 million and valued the company at about $5.2 billion. In addition, “multiple investments” in insurer Hippo Enterprises Inc. propelled its valuation to more than $1 billion, according to the report by Clyde & Co.

KBW’s Mr. Shields said that while insurtech deals have largely been smaller thus far, “we’re starting to see some very prominent insurtech companies with, in many cases, very impressive valuations.”

One insurtech, Integrated Specialty Coverages LLC, a Carlsbad, California-based program administrator, had a majority stake acquired by KKR & Co. Inc. in March. KKR bought the stake from Sightway Capital, which will continue to hold a minority interest in the company.

KKR, which made its investment through its Americas XII Fund, also holds investments in USI Insurance Services Inc., Alliant Insurance Services Inc. and Sedgwick Claims Management Services Inc.

Founded in 2017 by CEO Matt Grossberg, Integrated Specialty writes approximately $300 million of specialty premium annually.

KKR brings “a depth and wealth of knowledge in the insurance space, and they have a lot of relationships, which will be beneficial from an acquisition perspective,” Mr. Grossberg said.

In addition to insurtech M&As, several established insurtech companies raised significant funds in the past several weeks, including San Francisco-based cyber managing general agent Coalition Inc., which raised an additional $175 million in capital, and Boston-based cyber managing general underwriter Corvus Insurance Holdings Inc., which raised $100 million.

Growth in SPACs

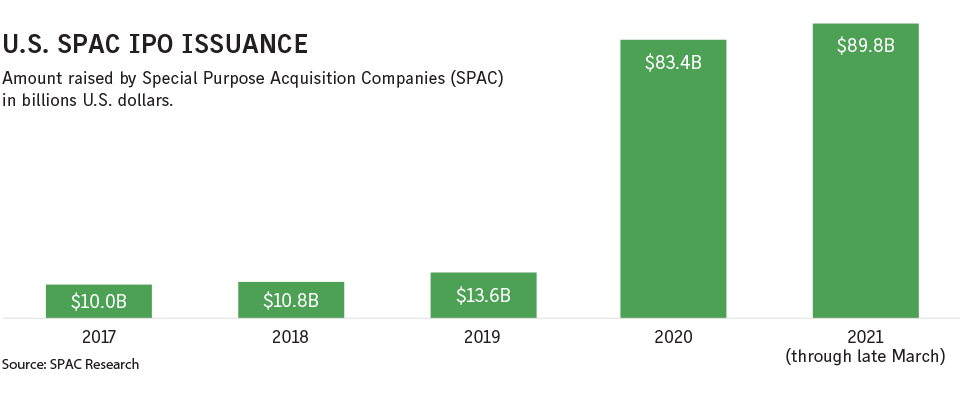

Special purpose acquisition companies, shell companies formed to raise capital without the need for a traditional IPO, have been growing wildly in popularity.

By late March 2021, there has been $89.8 billion raised across 276 SPAC deals, compared with $83.4 billion in 248 deals in all of 2020, according to data from SPAC Research, an industry tracker. In 2019, there was just $13.9 billion raised in 59 deals, showing how quickly the market has grown.

Personal lines insurer Hippo Enterprises, based in Palo Alto, California, is going public through a merger with Reinvent Technology Partners Z, a SPAC that launched last year, in a deal that values Hippo at $5 billion.

The growing popularity of SPACs should provide another avenue for insurtech investing, according to Martha Notaras, managing partner at Brewer Lane Management LLC, a venture capital firm in Los Angeles.

“The mergers and acquisitions market continues to heat up,” said Mr. Grossberg of Integrated Specialty.

“It’s incredibly active right now, especially given many participants still don’t get to meet face to face. Acquirers don’t get to meet in person with most of the candidates they’re buying. There’s a lot of willing and excited capital out there looking to enter the space.”

Read Next

-

States introduce changes to promote legacy deals for insurance sector

Mergers and acquisitions among ongoing insurance sector companies are triggering more interest in runoff transactions to seal off old liabilities, and the trend has been boosted by legislation in various states seeking to simplify the process.