COVID-19 one year later

Posted On: Mar. 4, 2021 12:00 AM CST

In March 2020, lockdowns were imposed in much of the United States and in many countries around the world in response to the rapid spread of the new virus SARS-CoV-2, or the coronavirus. One year later, the virus is still raging, and COVID-19 has caused more than 500,000 deaths in the U.S., but the rollout of vaccines is building confidence that the pandemic may at least be more manageable.

As in other sectors, the outbreak caused huge amounts of uncertainty and confusion in the risk management and insurance field. Much remains unclear, but various decisions by courts, regulators and lawmakers have added some degree of clarity on COVID-19 issues. In this special report, we look back on the turmoil risk managers have faced and what’s likely to happen in the years ahead

Lost income claim disputes evolve further

By Judy Greenwald

Shortly after businesses suspended operations during government-mandated lockdowns that began last March the first suit seeking business interruption coverage for forced closures was filed.

A few months later, courts began issuing rulings in the cases and in most instances favored insurers, but policyholders have also scored several victories.

Policyholders are likely to start winning more COVID-19-related business interruption cases, but a clear picture of the litigation landscape will not fully emerge before appeals courts start to rule in the cases, many experts say.

About 80% of court rulings to date have been in insurers’ favor, with many of the pro-policyholder rulings issued by state courts.

Policyholder attorneys say the early tilt in favor of insurers may in part be because many of the initial cases, which were often on behalf of small businesses such as restaurants, were filed by attorneys who do not specialize in insurance law.

But as more cases are filed by larger companies that are represented by specialized insurance attorneys, the win-loss ratio is likely to shift, although rulings will also depend on the court and jurisdiction.

Two factors that may determine the outcome of the cases are whether a court considers COVID-19 to inflict property damage, which tends to weigh in favor of coverage, and if the policy includes a virus exclusion, which could weigh against it.

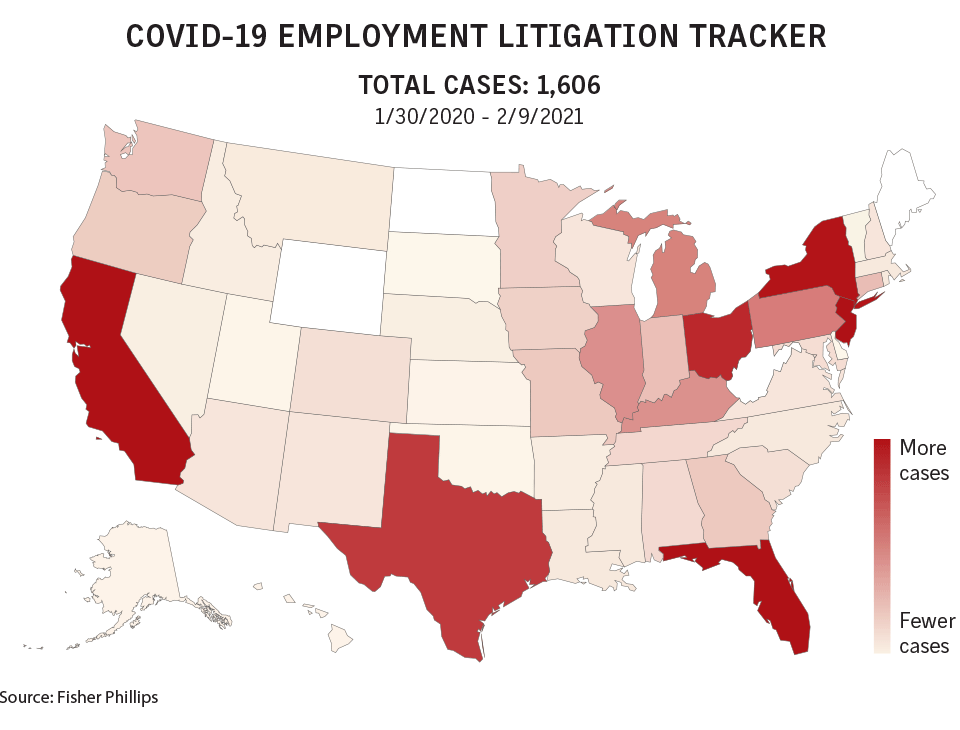

Meanwhile, despite the current emphasis on business interruption, some experts believe other COVID-19-related issues, such as employment practices liability and cyber liability, will become a greater focus of pandemic-related litigation (see related story below).

“The tide has already turned” toward policyholders, said policyholder attorney Michael S. Levine, a partner with Hunton Andrews Kurth LLP in Washington, discussing insurer victories.

“There are a lot of cases that were brought either prematurely or based on policies that don’t provide coverage or are based on pleadings that don’t adequately allege the salient facts, and those cases are being dismissed, but that was expected.”

Insurers may start to encounter additional obstacles, said Daniel A. Rabinowitz, an insurer attorney with Kramer Levin Naftalis & Frankel LLP in New York.

Policyholders have had success in arguing virus exclusions do not apply, he said, although each case must be evaluated individually.

However, Jeffrey M. Wank, an insurer attorney with Kelley Kronenberg LLP in Fort Lauderdale, Florida, said the courts have, for the most part, ruled correctly.

“Most courts have found, based on science and based on what we know of the virus, that it does not cause actual physical damage” and therefore does not trigger coverage, he said.

The litigation picture will come more fully into focus once higher courts, including federal appeals courts and state supreme courts and perhaps ultimately the U.S. Supreme Court, weigh in, and these rulings may begin to be issued this year, experts say.

Appellate court rulings “will help the parties on both sides to better understand the legalities of the policy language” and “help streamline the process and minimize the litigation because it will allow the parties to resolve the claims,” Mr. Levine said.

The issues of whether there has been physical damage and whether a policy has a virus exclusion will remain key, experts say.

Micah E. Skidmore, a partner with Haynes & Boone LLP in Dallas, said, “The trend seems to be that courts are persuaded by the argument that if you can document the presence of the virus on your property,” if you had employees, patrons or others who you can say were infected and came onto the premises, “that seems to be among the more compelling arguments” for determining there has been a physical loss, although “it’s hard to generalize.”

Tyrone R. Childress, insurance recovery practice leader with Jones Day LLP in Los Angeles, said, “The battlefield is a little more level” between policyholders and insurers when there is not a virus exclusion.

Michael John Miguel, a principal with McKool Smith in Los Angeles, said it’s too early to tell whether COVID-19 business interruption litigation will be like legal fights over insurance coverage for Y2K remediation costs, which ended within a few years of the millennium turning, or more like disputes over coverage for asbestos liability, which have been raging for decades.

Some observers believe that, although it cannot be cited as a precedent in U.S. courts, a United Kingdom ruling in favor of many policyholders on the business interruption issue may influence U.S. decisions.

The U.K.’s highest court ruled in a test case that some policies provided coverage under various disease or loss of access clauses.

“I think courts are going to look at the U.K. decision and say, ‘That makes a lot of sense,’” said R. Hugh Lumpkin, a partner with Reed Smith LLP in Miami.

Attorneys say future rulings will depend on factors including the judge and jurisdiction involved.

Observers say there has been a mixed reaction by insurers regarding changes to their policy language to more clearly avoid litigation stemming either from COVID-19 or future pandemics.

Jonathan B. Sokol, a policyholder attorney with Greenberg, Glusker, Fields Claman & Machtinger LLP in Los Angeles, said, “I would assume the ones that haven’t are certainly going to be when these policies come up for renewal.”

Litigation set to expand

While much of the focus of COVID-19-related litigation to date has been on business interruption claims, lawsuits are also being filed on other pandemic-related issues, including bodily injury, employment practices liability and other specialty risks, observers say.

“While there’s been a huge amount of focus, obviously, given the number of lawsuits filed” related to business interruption, there are broader COVID-19 issues beginning to emerge, said Tyrone R. Childress, insurance recovery practice leader with Jones Day LLP in Los Angeles.

Bodily injury cases have already been filed by cruise lines passengers, among others, said R. Hugh Lumpkin, a partner with Reed Smith LLP in Miami.

Employers may also face suits filed by employees who are required to work and become sick, he said.

In addition, directors and officers liability suits have been filed against companies, such as suits alleging companies made unfulfilled promises about their ability to somehow profit from the pandemic.

Daniel A. Rabinowitz, an insurer attorney with Kramer Levin Naftalis & Frankel LLP in New York, said that although the cases will not be a “slam dunk,” there is likely to be less litigation over policy language as there has been in business interruption cases, which hinge on interpretation of physical loss and damage.

Robin Cohen, chair of Cohen Ziffer Frenchman & McKenna LLP in New York, said that while other types of claims will evolve, “these business interruption claims are very, very large.”

As a result, “while there’s going to be other claims that are going to come out of this, I wouldn’t underestimate the importance, or the significance, of the business interruption claims.”

State efforts to mandate cover fall short

By Claire Wilkinson

Legislative efforts to force insurers to either retroactively cover business interruption claims due to COVID-19 or to provide prospective coverage for future pandemics are unlikely to gain traction this year, legal experts say.

So far in 2021, several states, including New York, Pennsylvania, Rhode Island and Washington, have introduced or reintroduced bills that would require insurers to provide some sort of retroactive business interruption coverage for COVID-19.

In December 2020, a bill was filed in Texas that would take effect Sept. 1, 2021, and apply to insurance policies written or renewed on or after Jan. 1, 2022. SB 249 would require business interruption insurance to “cover loss caused by a pandemic, including loss caused by the order of a civil authority made to prevent the spread of a pandemic, without regard to whether the pandemic caused a direct physical loss to the policyholder’s property.”

Jeffrey L. Kingsley, New York-based partner at Goldberg Segalla LLP, said he was not surprised to see efforts in certain jurisdictions last year “to try to retroactively eliminate an exclusion or declare that somehow this virus was a physical loss to cover.”

Between March and May of 2020, numerous state legislatures introduced bills, some of which would have forced insurers to retroactively cover business interruption claims due to COVID-19.

The legislative moves came as businesses looked to their property insurance policies for business interruption coverage to recover lost income associated with closures following government-mandated shutdowns early in the pandemic.

With the lockdowns now easing in some jurisdictions and the lack of traction for the better part of 2020, “I don’t see an uptick or a push for retroactive business interruption carveouts this year,” Mr. Kingsley said.

The pressure to provide some sort of compensation has eased a little, because of the financial relief that has been provided by the federal government, he said.

“It would be a hard sell, unless there is some type of change in the direction of the pandemic, to see the legislators really take it up and push it forward,” Mr. Kingsley said.

Steven Badger, Dallas-based partner at Zelle LLP, said there’s no indication that legislative efforts to force retroactive coverage are moving forward in any state.

“Everyone has realized that’s a non-starter,” because it’s both unconstitutional and fundamentally unfair to change contracts that were negotiated between insurers and their policyholders prior to COVID-19, Mr. Badger said.

Efforts to legislate prospectively to force coverage in the future are “equally as untenable,” because they will threaten the financial viability of insurers, “or more likely in states where any such laws are enacted the insurance industry will just stop writing insurance because it cannot under any circumstance assume a risk that every one of its insureds will suffer,” Mr. Badger said.

Feds weigh pandemic risk backstop

By Claire Wilkinson

Revised legislation to create a federal pandemic backstop is in the works as businesses look to recover amid easing COVID-19 restrictions.

While the Pandemic Risk Insurance Act introduced in May 2020 by Rep. Carolyn Maloney, D-New York, was modeled on the Terrorism Risk Insurance Act that was enacted after the 9/11 terrorist attacks, a reconfigured bill may look quite different, experts say.

In addition to Rep. Maloney’s bill, various plans were put forward last year, including a taxpayer-funded pandemic backstop plan proposed by major insurance industry groups.

Policyholder groups also formed a coalition advocating for a public-private backstop for pandemic business interruption insurance, while individual insurer plans were put forward by Chubb Ltd. and Zurich North America.

The proposals followed a letter sent to Congress in March 2020 by John Doyle, president of Marsh LLC, urging a public-private pandemic risk-sharing program.

The political dynamic has shifted in Washington from a year ago, which may have some bearing on this issue, said Robert Hartwig, clinical associate professor and director of the Risk and Uncertainty Management Center at the University of South Carolina in Columbia.

“Increasingly the industry is recognizing that the vast majority of response associated with pandemic events really has to be housed and organized by the government,” Mr. Hartwig said.

Aid packages that passed Congress in 2020, along with the $1.9 trillion in relief proposed by the Biden administration, bolster the idea that the appropriate way to handle the economic consequences of pandemics is through a “robust federal government response,” Mr. Hartwig said.

Insurers have also generally stated that they don’t want a financial risk-sharing role along the lines of what they have with TRIA, he said.

“We are helping to facilitate Congress hearing from various participants as they work on a revised PRIA that will hopefully incorporate comments from insurers and policyholders,” said Erick Gustafson, chief public affairs officer at Marsh & McLennan Cos. Inc.

“We think it’s going to be a more thoughtful piece of legislation and reflective of input from both policyholders and insurers,” Mr. Gustafson said.

Globally, the risk management and insurance communities recognize the importance of developing a plan that will help organizations more effectively manage future interruptions due to pandemics, said Whitney Craig, director of government relations at the Risk and Insurance Management Society Inc. in New York.

“A public-private partnership remains a RIMS priority as it will instill confidence in business leaders that their assets are protected, while also providing insurers with a financial backstop should we encounter another pandemic catastrophe,” Ms. Craig said in an emailed statement.

In addition to Rep. Maloney, Rep. Emanuel Cleaver, D-Missouri, newly appointed chair of the House Financial Services Subcommittee on Housing, Community Development and Insurance has said pandemic risks are a focus, according to reports.

RIMS is ready to collaborate and “hopes to see a new bill introduced in the coming months,” Ms. Craig said.

OSHA changes on the horizon

By Louise Esola

The COVID-19 pandemic and a new presidential administration have brought greater focus on workplace safety when it comes to infectious disease.

The U.S. Occupational Safety and Health Administration began working on an infectious disease standard for health care workers in 2010, but the effort stalled in recent years, prompting several unions to sue the agency on Oct. 29, 2020. The Department of Labor said in a Feb. 16 response to the lawsuit that OSHA would prioritize the development of the standard.

Meanwhile, employers have been bracing for OSHA to possibly create an emergency temporary standard for COVID-19 workplace safety. President Joe Biden issued an executive order on Jan. 21 calling on regulators to determine whether such a standard is necessary and, if so, to issue it by March 15.

The administration on Jan. 29 also introduced COVID-19 “guidelines” that mirrored what had been in place during much of the pandemic. The guidelines in general restated U.S. Centers for Disease Control and Prevention guidance, calling for face coverings, social distancing and contact-tracing.

OSHA also called on employers to implement COVID-19 prevention programs, separate and send home sick workers, improve safety communication with workers, install barriers, provide personal protective equipment, and routinely clean and disinfect workplaces.

Eric Conn, Washington-based chair of the OSHA practice at Conn Maciel Carey LLP, said his firm, along with labor organizations and other stakeholders, has been working with OSHA on developing an emergency standard for COVID-19 safety and that it is “imminent.”

“It’s not a traditional rulemaking,” he said of OSHA’s development of the emergency standard that does not give stakeholders an opportunity to see a draft and to comment.

“We are just doing everything we can to make sure that employers who have been managing around this crisis for a year now can share with OSHA what works, what doesn’t work, what would be a waste of time and money and what wouldn’t,” he said.

By late February, three states had already introduced safety standards — California, Michigan and Virginia. Oregon in late 2020 announced it was implementing a rule-making process for such a standard.

Legal experts say OSHA could include some elements of the states’ standards, could re-state the new guidance issued in January as its temporary standard, or continue the work that has been done to create an infectious disease standard.

“They may dust that off and go with (an infectious disease standard) since they have been working on it,” said Pat Tyson, partner and head of the OSHA practice in the Atlanta office of Constangy, Brooks, Smith and Prophete LLP, following January’s announcement that OSHA would be considering an emergency COVID-19 standard.

Another significant development since the beginning of the pandemic was OSHA’s notice that a workplace COVID-19 infection was a recordable illness, under its rules for reporting workplace injuries.

Meanwhile, according to a Reuters analysis, OSHA, which had issued more than $4 million in workplace citations to more than 300 employers since the start of the pandemic, had only collected $897,000 in fines from 108 companies, and that more than half of employers cited for COVID-19 safety problems by federal OSHA authorities had appealed. Most of the citations were issued for violations of the general duty clause and the respiratory protections standard, according to OSHA data.

Mr. Conn said he expects the contesting of citations to continue, even with a COVID-19 emergency standard in place.

There is “a lot of contesting because a lot of them are questionable,” he said. “I am defending a lot of employers right now because it is such a novel area.”

COVID-19 presumption laws emerge

By Angela Childers

The evolution of presumption measures continued in 2020 with the pandemic leading to executive orders and laws making it easier for certain classes of workers to obtain workers compensation for COVID-19.

Workers comp presumption laws — which place the onus on employers to rebut employees’ claims that their injuries or illnesses arose out of the course and scope of their employment — have been on the books for nearly two decades. These include presumptions for firefighters for certain cancers and for first responders for mental illnesses caused by traumatic work-related events.

But the expansion of such laws to include a highly communicable disease like COVID-19 is an emerging issue that may have lasting effects on the workers comp industry, experts say.

“When you’re looking at the fiscal impact of these different bills … what this is going to do to premiums and what it could potentially do to (the workers comp) marketplace could be considerable,” said Bert Randall, president of Baltimore law firm Franklin & Prokopik PC.

“If we start expanding presumptions to private sector jobs, are we going to see some carriers move away from certain lines? Is it going to shrink the market, or is it going to cause premiums to rise considerably?”

By August 2020, 11 states had issued executive orders or emergency rules creating presumption of compensability for certain classes of workers who claimed they acquired COVID-19 on the job, and eight states passed legislation establishing presumptions of compensability. Most of the laws and orders covered first responders and health care workers, and some included essential workers such as retail and transit workers and essential governmental employees.

Some of the laws and orders have expired, leading to a wave of bills to extend or create a legislative presumption.

According to the National Council on Compensation Insurance, in the first two months of this year several states enacted new presumption laws, while two states rejected such measures. Approximately 20 other states have introduced presumption legislation so far this year.

“There will be a period of time before we’ll know precisely what the financial impact (of COVID-19 presumptions) will be to the comp system,” said John Hanson, Atlanta-based vice president at Alliant Insurance Services Inc. Much of that uncertainty is due to the wide variations in the classes of employees covered and the burden of proof in the various presumption laws, he said.

For instance, some presumptions are written very narrowly. At the other end of the spectrum, proposed legislation in Oregon doesn’t require a positive COVID-19 test for the presumption to apply and allows workers in any industry with at least a 10% positivity rate to file a coronavirus comp claim, Mr. Hanson said.

California Gov. Gavin Newsom created a presumption via executive order last March, which was scaled back in legislation enacted in September that created a COVID-19 rebuttable presumption for first responders and health care workers. Although the number of coronavirus comp claims in the state is far less than the early doomsday prediction — with about one in six claims in the state related to COVID-19, according to the California Workers Compensation Institute — it’s too early to tell how the industry might be impacted by continued presumption expansions, said Amy Puffer, San Francisco-based claims consulting project manager for brokerage Woodruff Sawyer & Co.

“I know there’s concern that these compensability presumptions for contagious disease such as COVID might be widely adopted or permanently enacted and expanded to include other common diseases,” she said.

Workers comp claims pile up

By Louise Esola

Workers compensation claims for COVID-19 in the first year of the pandemic proved less expensive than anticipated, yet gathering claims data hasn’t been as easy as expected, experts say.

The biggest shock for the workers comp industry was that an infectious disease such as coronavirus would be compensable, according to experts trying to gauge the current and long-term effects.

“A year ago the majority of us in the claims arena would say, more likely than not, COVID claims would not be deemed compensable … with very little information on how an employee may pursue a claim that they got (the virus) at work,” said Carol Ungaretti, Chicago-based managing consultant with Aon Global Risk Consulting.

Then came the wave of presumption executive orders and laws — as of February more than 20 states either had a COVID-19 presumption in place or were in the process of establishing one — and, along with that, came the claim activity. The presumption makes COVID-19 illness compensable for workers, who are presumed to have been infected at work. Experts say there was concern early on that the claims would prove expensive and difficult to manage given how novel the virus is.

Recent data, however, points to a milder effect on the workers comp industry, experts say.

“At the beginning of the pandemic, the hypothetical scenarios and projections related to direct cost impact were quite grim,” Kim Haugaard, senior vice president of policyholder services at Austin-based Texas Mutual Insurance Co., wrote in an email. “The current impact has not been as bad as we anticipated that it could have been,” he said, noting that COVID-19 claims made up just 2% of claim activity for the insurer in 2020.

Trying to obtain data on how much the claims are costing or how widespread claim activity is has been complicated, said Mark Walls, Chicago-based vice president of communication and strategic analysis for Safety National Casualty Corp., during a recent webinar.

“One of the big challenges in analyzing workers compensation data trends is there is no single source for workers compensation information,” he said, adding that information from ratings agencies, various states, research organizations and self-insured entities is siloed.

The Boca Raton, Florida-based National Council on Compensation Insurance — which gathers data from 36 states — reported that most claims have not been severe. The top 5% of COVID-19 medical claims in the first half of 2020 drove about 70% of coronavirus-related payments, according to an NCCI analysis.

NCCI reported in January that 20% of COVID-19 claims included an inpatient hospital stay; of those, 19% required intensive care services. The cost of claims with a hospital stay averaged $38,500.

Overall, in analyzing COVID-19 claims activity in 27 states, the Cambridge, Massachusetts-based Workers’ Compensation Research Institute in January reported “great variation in the percentage of COVID-19 claims among all workers compensation paid claims,” ranging from 1% to 42% in the second quarter of 2020.

“A number of factors may have contributed to the variation, including severity of the COVID-19 outbreak, presumption laws, and compensability rules,” the WCRI analysis stated.

Angela Childers contributed to this report.