View from Washington: NFIP reform inches closer

Posted On: Aug. 1, 2019 12:00 AM CST

It might have gotten lost in the spectacle of Bob Mueller’s congressional testimony, but a legislative fix for the troubled National Flood Insurance Program may finally be gaining some traction.

A bipartisan group of senators introduced a bill to revamp and reauthorize the NFIP in July, which followed unanimous approval of a program overhaul bill by the U.S. House of Representatives Financial Services Committee in June.

The bills are not that far apart. They both feature a five-year extension, which risk managers have been pushing for so they wouldn’t have to contend with looming expirations and retroactive reauthorizations of a program critical to their insurance placements.

Both bills pay particular attention and devote resources to flood mapping and mitigation initiatives, which experts say is critical to getting an accurate view of evolving flood risks and determining where best to deploy limited government resources.

But like any proposal emerging from Congress these days, the bills have not escaped criticism. The National Association of Professional Insurance Agents was “heartened to see bipartisan, bicameral support for important reforms,” but the Senate bill includes a provision that PIA National deemed “unacceptable”: a 25% cut to the Write-Your-Own reimbursement rate. “As a result, most, if not all, WYO insurance carriers could be pushed out of the program,” the organization stated.

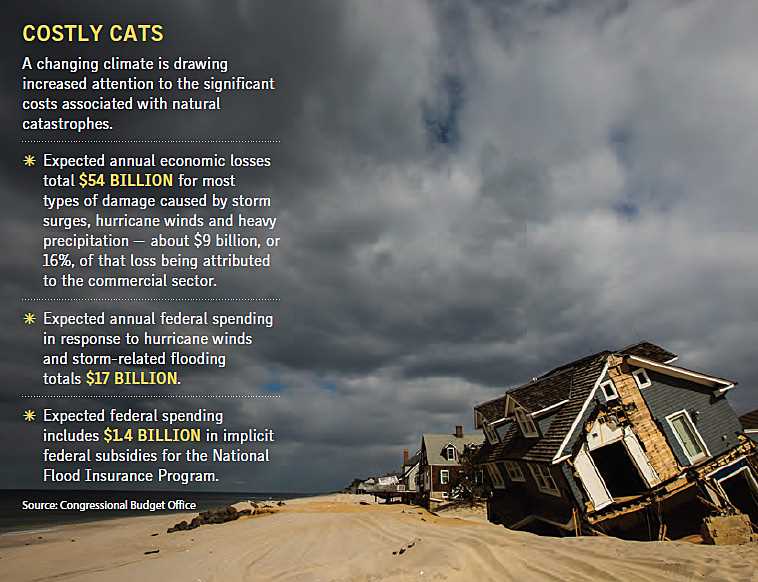

And naturally, the bills don’t deal with the financial elephant in the room: what to do about the program’s existing $20 billion-plus debt. Premiums are failing to keep up with program payouts. The Congressional Budget Office has estimated a $1.4 billion gap between the NFIP’s expected annual payments and its expected income from premiums — a shortfall that the CBO assumed would be financed by borrowing from the federal Treasury. Of course, the agency would assume that. Why would it assume anything else? The NFIP has continually needed to borrow to cover shortfalls caused by major catastrophic events. In October 2017, President Donald Trump signed a bill forgiving $16 billion in debt following the devastation caused by hurricanes Harvey, Irma and Maria. But whether or not to forgive the rest of the debt continues to be a source of disagreement for federal legislators.

The Federal Emergency Management Agency’s Risk Rating 2.0 initiative aims to address the disconnect by charging actuarially appropriate rates, but legislators are skittish about the initiative, having gotten earfuls from their constituents the last time they tried to set rates that actually reflected rising flood risks —ergo, the 9% cap on annual rate increases featured in the Senate

proposal, which would draw “guardrails” around the initiative. The Senate bill would temporarily freeze interest payments on the NFIP debt — freeing up about $400 million per year — but Congress does a disservice to FEMA and to its constituents by refusing to deal with the overarching debt problem.

However, it seems clear that a political calculation has been made that the only way to push some reforms forward is to ignore the elephant. If so, perhaps risk managers can be cautiously optimistic that a long-overdue overhaul of the program may finally be in sight.