Assailant coverage evolves as shootings rise

Reprints

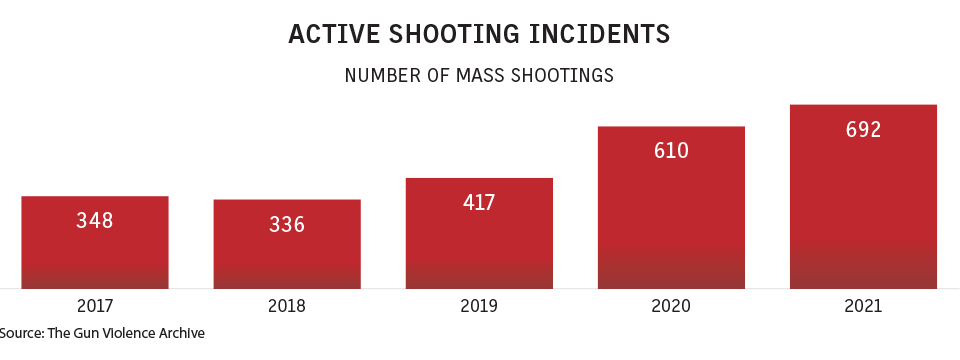

Interest in active assailant insurance coverage has risen among an expanding range of organizations in the wake of several recent mass shootings.

Most demand comes from businesses and organizations in the United States, which has seen high-profile shootings in New York, Texas, Illinois and elsewhere over the past several months. U.S. policyholders account for 80% or more of the coverage bought, experts say.

The insurance products, which were often called active shooter policies when they were launched about seven years ago, have been expanded and wider definitions applied as attackers employed different methods including knife and vehicle attacks.

CLICK IMAGE TO ENLARGE

There is “absolutely” more interest in this coverage, said Morgan Shrubb, New York-based head of terrorism for Axa XL, a unit of Axa SA. Her team now offers active assailant coverage on all of its quotes for terrorism insurance and the take-up rate has doubled this year, she said.

Beazley PLC deployed a team of four people in the U.S. earlier this year to market its active assailant insurance product and inform potential policyholders and brokers, said Chris Parker, head of terrorism and deadly weapon protection for the insurer in London.

“It’s never been busier,” Mr. Parker said. With mass shooting numbers increasing in the U.S. every year, “there’s more interest in the product,” with both inquiries and binding up, he said.

Policy language varies, but exposures covered by the insurance can include property damage — in some cases including rebuilding costs of schools or other buildings demolished after an event — business interruption, legal liability, loss of attraction or access and various response-related costs. There is no standard coverage form used by the market (see related story, below).

Purchased limits in the range of $1 million to $2 million were available when the Beazley coverage was introduced in 2016, but the average limit has risen to between $3 million and $5 million, Mr. Parker said. The largest limit available — incorporating nearly every underwriter in the market — is $100 million, which Beazley writes for two policyholders, he said.

Aspen Insurance Holdings Ltd. offers a maximum limit of $25 million, and the average limit purchased is $7.8 million, said Tim Strong, London-based head of crisis management at the insurer.

Mr. Strong said that inquiries and submissions usually rise by about 15% to 20% after an event, “but given the steady frequency of events in the U.S., submissions counts have been pretty constant,” he said.

Interest in Hiscox Ltd.’s active shooter and malicious attack coverage has grown along with the increase in attacks, said Atlanta-based Elise Barton, head of war, terrorism & malicious acts at Hiscox USA.

The types of organizations looking at active assailant covers are also widening. When the coverage was first offered, many of the buyers were schools, municipalities and other public entities, sources say. More recently, interest has grown in the corporate sector, said Jo Holliday, managing director and global head of crisis management for Willis Towers Watson PLC in London.

“In the past six months in particular, there’s been a real increase and divergence in the types of clients which are asking about and binding the coverage,” she said.

Beazley’s Mr. Parker said there is no category of industry where an organization has not bound coverage.

Historically, municipalities and schools had been the buyers of coverage from Axa XL, but the coverage is increasingly being bought by private sector companies, Ms. Shrubb said. Those buying active assailant insurance include apartment building owners, condominium associations, hotels, retailers and entertainment companies, she said.

The broad interest reflects how many locations are potential targets, including religious organizations and others, said Hiscox’s Ms. Barton.

The risk management community is also showing growing concern and awareness of the issue.

“As risk managers, I think it’s important for us to bring these topics up to our executives,” said Kristen Peed, corporate director of risk management at Cleveland-based CBIZ Inc. and a board member of the Risk & Insurance Management Society Inc.

“We need to have proper training for our employees to know how to react if faced with this,” she said. “We can’t ignore what’s going on because the events are happening it feels like on a more regular basis, so we are forced to look at and address the risks.”

RIMS has an active shooter report and is increasingly incorporating programming on active assailant issues into its events and educational efforts, according to a spokesman for the organization.

As with other property market coverages, the cost of active assailant coverage has increased, said Jennifer Rubin, New York-based head of terrorism for Liberty Specialty Markets, a unit of Liberty Mutual Insurance Co., which offers the cover as a sublimit of war and terrorism policies.

The market for active assailant coverage is smaller and less mature, making it less available and thus subject to higher rates, she said.

Lack of standardized forms, exclusions a challenge for buyers

The active assailant insurance market is still in its early stages, and there remains a lack of standardization in policy language and forms among insurers, experts say.

“Carriers’ offerings are all differentiated; there is no standardized form,” said Morgan Shrubb, New York-based head of terrorism for Axa XL, a unit of Axa SA.

Insurers have different definitions of coverage and triggers, and policy terms and language are frequently updated as the market evolves, Ms. Shrubb said. “It’s still such a new product in the marketplace, that markets are still adjusting and evolving their wording,” she said.

Organizations should be careful when choosing insurance products because of the differences in policy language — including exclusions — among the various forms in the market, said Kristen Peed, corporate director of risk management at Cleveland-based CBIZ Inc.

“Risk managers should really be aware of those differences and exclusionary language and make sure to purchase the right type of coverage for their business,” she said.

Building a larger, more established market to allow brokers and policyholders to better and more quickly understand their choices will likely require greater standardization of language and terms, said Tim Strong, head of crisis management in London for Aspen Insurance Holdings Ltd.

“To take the market forward will require more syndication,” he said.