Editorial: Disasters teach enduring lessons

Reprints

There’s nothing like experience to change perspectives. Individual and collective run-ins with catastrophes, in particular, can change how people and society respond to the potential for future threats.

It sometimes requires multiple close encounters, though, for the message to get through. While living in London — a city not known for its exposure to intense windstorms — I managed to sleep through the hurricane-force winds of 87J, also known as the great storm of 1987. The next day, after walking through the debris to work at a financial magazine, I was more focused on the tumult in the stock market than on the aftermath of what had been a deadly storm.

Eleven years later, staying south of Miami while Hurricane Georges hit southern Florida, the sheer power of a major storm was much more apparent. There wasn’t much to do other than stay away from windows as torrential rain flooded streets and pieces of palm trees flew around outside.

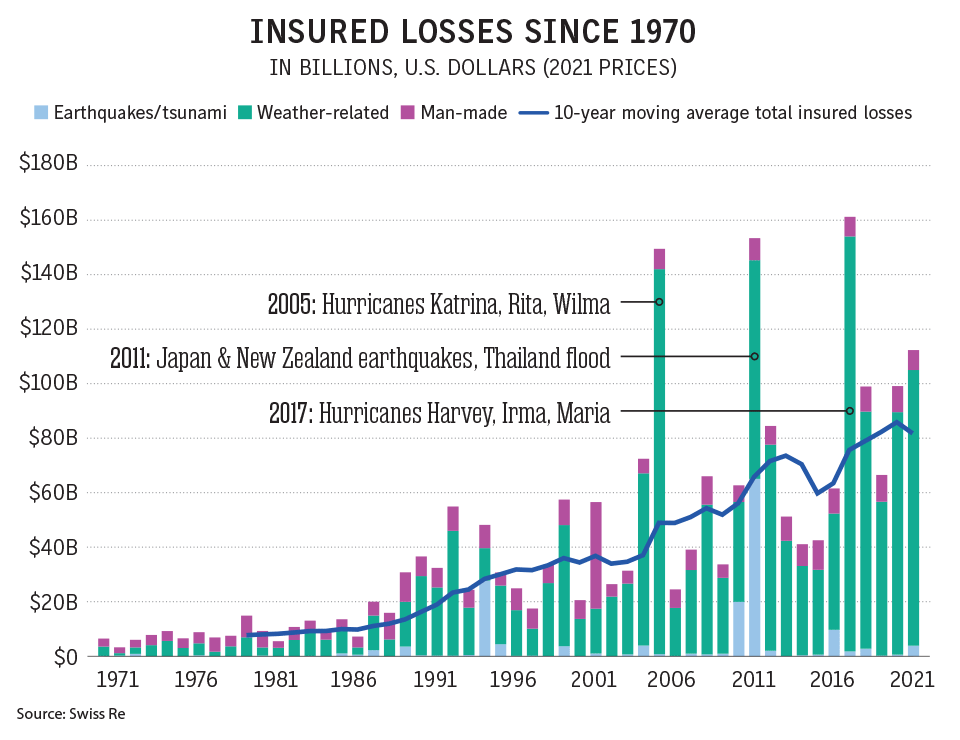

A few years earlier, Hurricane Andrew had a huge effect on many people’s understanding of storm risks and how they could be insured. As we report in our cover story, 30 years after Andrew, insurers and reinsurers are still operating in an environment that was shaped by the storm.

Improved building codes, the wide acceptance of computer models in the underwriting process, the expansion of reinsurance capital and the beginnings of an understanding of how climate change is transforming property risk management can all be traced back to Andrew.

And the experience of other storms since, in particular Hurricane Katrina in 2005 and Superstorm Sandy in 2012, has led to even more changes in how the industry manages natural catastrophe risks and how insurance policies are worded to cover or exclude the variety of different losses that are associated with severe windstorms.

But there is still more to be learned. As we report on page 4, safety experts have significant concerns over the adequacy of organizations’ emergency action plans, and those concerns have only been heightened by recent disasters involving tornadoes.

Less predictable and less effectively modeled than hurricanes, twisters require quick and flexible responses, but that does not mean that the various scenarios can’t be simulated in table-top exercises at organizations of all sizes.

The experience of increased disasters over the past three decades has led to permanent changes in risk management practices but response plans need to continually evolve as we head into a period of potentially even more uncertainty.

Insurers and reinsurers started talking about the effects of climate change on their business long ago, and many in the industry must be frustrated that the evidence they see in their loss figures is still ignored or explained away by some who would rather just wish that the problem would disappear. Experience needs to triumph over hope when it comes to natural catastrophes.