Editorial: Public entity risks reach new levels

Reprints

Public entity risk managers are having as hard a time as any insurance buyers as they prepare for renewals. A combination of marketwide trends and sector-specific challenges has created insurance and risk management conundrums that would test even the most seasoned risk professionals.

As we report beginning on page 32, in the past couple of years, the most high-profile problem municipalities have had to face is police liability coverage. Highlighted by the chilling recording of the murder of George Floyd in 2020, police misconduct is being graphically documented with far more frequency than just a few years ago. The inevitable increase in lawsuits and claims against police departments led to severe restrictions in capacity as insurers and reinsurers cut limits or exited the market.

Other liability concerns are also testing the ability of buyers and brokers to find adequate coverage for municipalities and school districts. Increased friction between parents and teachers that resulted from virtual classes during the pandemic, fights over social issues such as the treatment of transgender students, and the emergence of historic sexual abuse claims are making already wary insurers even more concerned about the limits they offer and prices they charge.

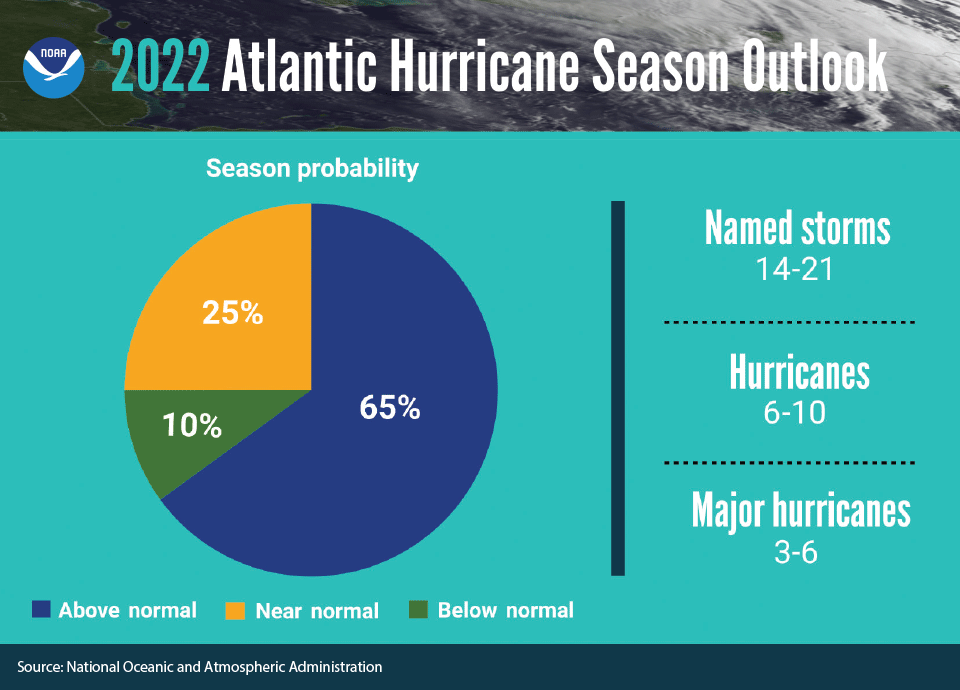

On the property side, things are not much better. As people continue to move away from parts of the Northeast and Midwest to areas of the country that are more vulnerable to windstorms, such as Texas and Florida, inevitably the public entities and school districts in those states grow larger and occupy more buildings. The increase in the instances of costly hurricane losses over the past three decades has been felt acutely in the public entity sector, and, looking ahead, the situation is unlikely to improve anytime soon (see chart).

While there are some signs that the property/casualty market may be stabilizing, given the economic environment, there’s no reason to think that there is not more uncertainty to face in the years ahead.

To address the issues, risk managers at public entities and their brokers are having to be inventive in the way they approach their insurance programs and the resources they turn to. Like buyers in the private and publicly owned sector, they can to some extent look to self-insurance facilities. While captives are not as attractive to public entities as to private companies because they do not see the same tax benefits, municipal risk pools and other structures are gaining in popularity in the hard market.

If there is any upside to the troublesome market it would be that risk managers are likely to receive more attention as they seek to implement policies that help avoid losses in the first place. Changes in police protocols, policies to intervene in contentious school disputes, and improvements in property resilience should all be considered more seriously as ways to improve safety and save taxpayers money over the long term.