Terrorism coverage expands as risks evolve in decades following shock of 9/11 attacks

Reprints

The Sept. 11, 2001, terrorist attacks in the United States caused huge losses and disruptions in property insurance markets.

While insurance claims from the attacks led to years of litigation, with insurers ultimately paying about $4.55 billion under various policies for the World Trade Center and about $30 billion in total losses, insurance coverage for terrorism risks going forward evaporated.

Prior to the attacks, terrorism coverage was usually included in most property coverages, but after 9/11 insurers inserted exclusions barring terror cover and the U.S. government had to create the so-called TRIA backstop to stabilize the market (see story, below).

In the years that followed, insurers became more comfortable with the exposure and capacity for stand-alone terrorism coverage grew. But the perceived threats have changed.

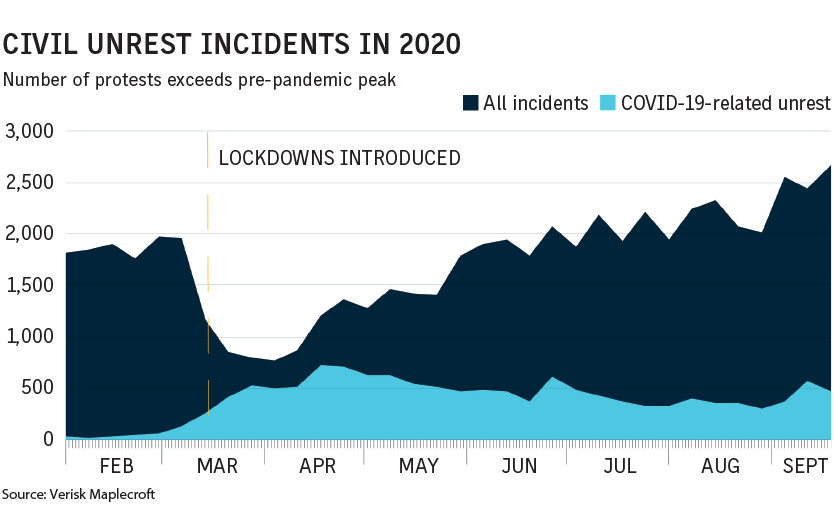

More recently, the coverage has expanded to encompass active assailant risks. In addition, coverage for civil unrest is seeing renewed interest in the wake of the social tumult in the U.S. during 2020.

Pricing for such coverage has seen the greatest upward pressure, while stand-alone coverage for acts of terrorism has experienced only modest increases.

Demand is definitely increasing, said John Minor, Chicago-based director of crisis management for Aon Risk Solutions, part of Aon PLC. “The number of new clients binding stand-alone terrorism programs increased by nearly 50% last year, and this trend continues into 2021.”

Much of the demand is for political violence coverage in response to an increase in protests and civil unrest occurring in many parts of the world, he said.

Sources agreed that the situation in Afghanistan has yet to affect the market for stand-alone terrorism insurance as the focus remains on domestic exposures and the civil unrest losses of 2020.

In the U.S, civil unrest and protest activity has risen in profile recently.

“The extremists on both sides, whether far left or far right, they are the new terrorists. There is heightened awareness of their activity,” said Wendy Peters, executive vice president of financial solutions-terrorism and political violence for Willis Towers Watson PLC in New York.

Insurers view the U.S as a bit more of a higher risk than five or 10 years ago, said Tarique Nageer, terrorism placement and advisory practice leader for Marsh USA Inc. in New York. “The threat going forward, from an insurer’s perspective, has changed. Domestic threats are high on the insurer’s radar screen. Now the threat is from within, and it’s a different kind of threat.”

Social unrest in 2020 “definitely drove a lot of inquiries into the stand-alone terrorism market from clients asking to help them understand where the line is, what would be picked up in an all risk policy versus a stand-alone terrorism policy,” said Jennifer Rubin, New York-based head of terrorism for Liberty Specialty Markets, a unit of Liberty Mutual Insurance Co.

Strike, riot and civil commotion coverage can cover damages of the type that might occur in the wake of a social protest or a mass looting event, such as those that occurred in New York and other U.S cities in mid-2020.

The stand-alone terrorism market is seeing more and more requests for strike, riot and civil commotion coverage, Mr. Nageer said.

Such risks had historically been covered under property all risk policies but as a result of the events of 2020, “some insurers are electing to exclude SRCC from all risk property forms, which drove clients elsewhere for cover,” he said. “For the first time in the U.S., people began to realize this is a risk and they need to look carefully at how they are buying it.”

The market for strike, riot and civil commotion coverage is the only one in the stand-alone terrorism sector to see capacity reductions, and it also saw the largest price increases, said Morgan Shrubb, New York-based head of terrorism for Axa XL, a unit of Axa SA.

The various incidents of unrest in the U.S. in 2020 “played a role for certain clients, specifically in the retail and hospitality industries, facing some price increases and challenges, depending on the type of insurance they bought.”

Pricing for stand-alone terrorism policies, as distinct from active assailant and strike, riot and civil commotion, rose in the single digit range for most policyholders, experts say.

Ms. Shrubb noted that she is seeing increased submissions from entities that had stopped or cut back limits for stand-alone terrorism coverage as exposures plummeted during the pandemic lockdown — such as hotels, event venues and malls — and are now coming back to the market as exposures return to pre-pandemic norms.

In addition, some policyholders are interested in the crisis management and other services offered through the stand-alone terrorism active assailant markets. “They want the coverage extensions which the active assailant market offers,” such as security and public relations consulting and crisis management response services, Ms. Shrubb said.

“Some markets are offering a more robust consulting service from their third-party risk partners, allocating a portion of the premium to cover the costs of a wider array of consulting services,” Mr. Minor said.

Terror risk program acts as backstop, but insurers’ share of exposure rises

Prior to Sept. 11, 2001, terrorism existed as a “silent” peril in all risk property coverages, under which terrorism was not specifically excluded.

“Policies didn’t identify it as a peril, so if you had an all risk policy it was covered because it wasn’t excluded,” said Wendy Peters, executive vice president of financial solutions-terrorism and political violence for Willis Towers Watson PLC in New York.

The specialty terrorism insurance market in the United States was practically “nonexistent” prior to the attacks, said Tarique Nageer, terrorism placement and advisory practice leader for Marsh USA Inc. in New York.

Before 9/11, terrorism insurance coverage was largely written in the London market and addressed risks in regions such as Northern Ireland and Colombia, where terrorists were more active.

That changed after the attacks in the United States when the government had to step in to support the private market. The Terrorism Risk Insurance Act, which was signed into law in 2002, created a backstop for commercial insurers to cover terrorism risks.

Under the original law, the government backstop was triggered after the insurance industry lost $10 billion. That amount rose for 2003 and 2004 and as the program was extended or reauthorized in 2005, 2007, 2015 and 2019.

Under the current iteration of the program — the Terrorism Risk Insurance Program Reauthorization Act of 2019 — for 2020 the program trigger was $200 million in losses, which has been increasing in $20 million annual increments since 2015. The insurance industry retention has been rising in $2 billion increments, from $29.5 billion in 2015 to $37.5 billion in 2019 and rises to the average of insurers’ deductibles over the previous three years. The program’s cap on liability is $100 billion.

Related Stories

Most Read in Risk Management

Sign up for Daily Briefing, the free email newsletter from Business Insurance.

Advertise

Resources